Australia’s superannuation concessions need to be adjusted to make them more equitable and sustainable.

According to the Australian Treasury, superannuation concessions cost the federal budget around $60 billion in foregone revenue in 2024-25 and are expected to grow rapidly.

Concessions on contributions cost the federal budget $30,950 billion in FY25, rising to $36,750 billion in FY28.

Concessions on superannuation earnings cost $24,200 billion in FY25, rising to $28,250 billion in FY28.

Reform should, therefore, target these two areas.

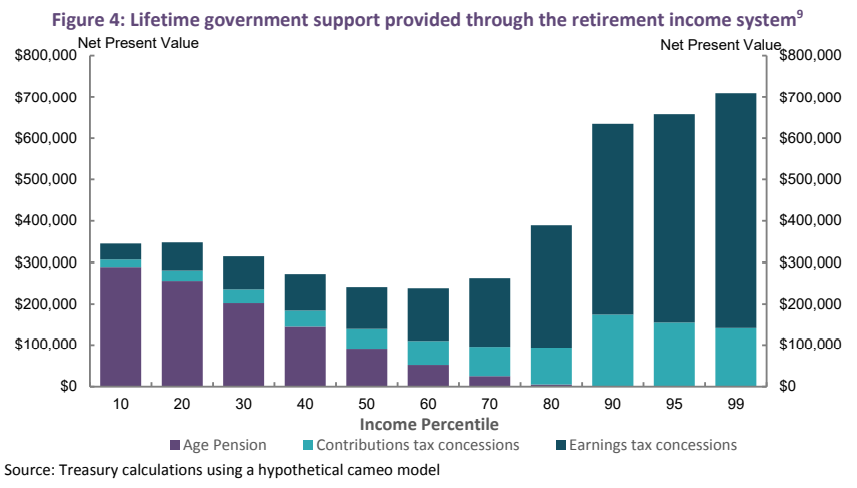

These two superannuation concessions overwhelmingly flow to higher-income earners:

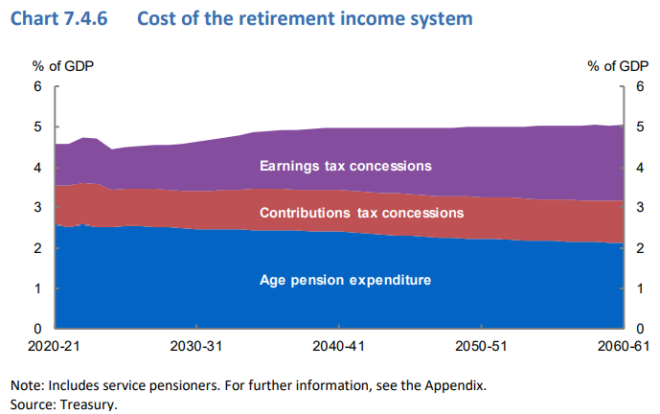

Superannuation concessions are also projected by the Australian Treasury to cost more than the aged pension:

The Albanese government has announced that it would increase the earnings tax on super balances of $3 million or more from the current 15% to 30% without indexation. It would also apply the 30% tax rate to unrealised ‘paper profits’.

The taxing of unrealised gains is opposed by the Coalition and most teal independents, business leaders, the superannuation industry, and eminent economists such as former Treasury Secretary Ken Henry (lead author of the 2010 Henry Tax Review) and former Reserve Bank of Australia (RBA) governor Phil Lowe.

Former ACTU secretary Bill Kelty, who was one of the architects of Australia’s compulsory superannuation system, is the latest prominent figure to criticise the proposed reforms, particularly the plan to tax the unrealised capital gains of super funds.

“I don’t mind taxing people but not unrealised earnings”, Kelty told The Australian.

“I think taxing unrealised capital gains is bad policy. It distorts the effective tax. Changes your income flows, and if it was on superannuation generally, there would be a revolution about it. It would destroy super”.

Bad policy is bad policy – for rich or poor”, he said.

I agree wholeheartedly with Kelty that there are better choices than taxing unrealised ‘paper earnings’, which complicates the system and is especially burdensome for illiquid, unlisted assets.

To reduce superannuation concession on contributions, the government should simply replace the 15% flat tax with a 15% deduction from one’s marginal tax rate.

This simple adjustment would make superannuation concessions on contributions progressive by matching one’s marginal tax rate minus 15%.

If a superannuant’s income was $220,000, they would be taxed at their marginal tax rate (47%) less 15%, resulting in a 32% superannuation contributions tax.

If a superannuant earning $30,000 contributed, they would be taxed at their marginal tax rate (18%) minus 15%, resulting in a superannuation contributions tax of only 3%.

The government should also reduce the threshold for large superannuation accounts to $2 million, link it to wage growth, and raise the tax rate on actual realised earnings from 15% to 30%. Doing so would be administratively simple because the second 15% of tax would be calculated in the same way as the first.

These two simple adjustments would improve the equity and sustainability of the superannuation system while also raising billions of dollars in revenue for the federal budget.

They would also eliminate the complexities associated with taxing unrealised gains.