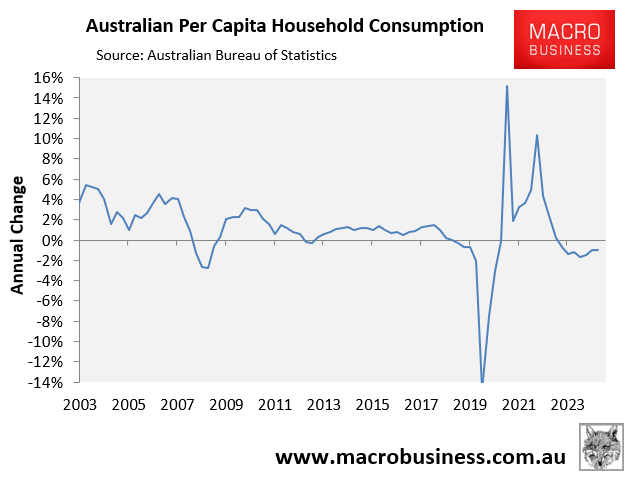

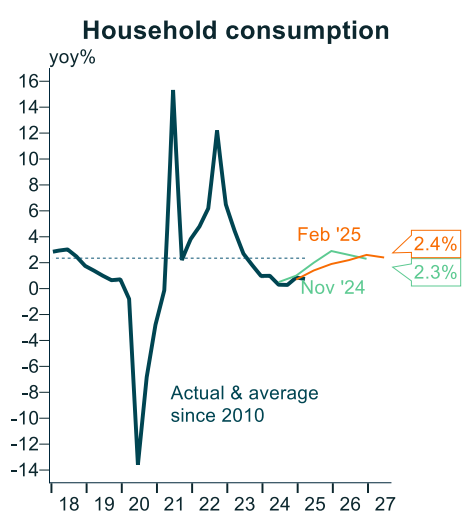

Last week’s Q1 national accounts release from the Australian Bureau of Statistics (ABS), revealed that real per capita home consumption has been negative for seven consecutive quarters on an annual basis, down 2.4% from its peak.

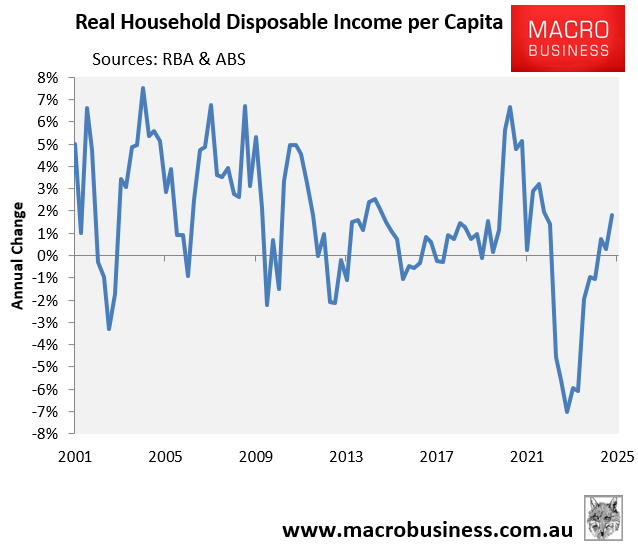

The fall in household spending occurred despite a 1.8% increase in real per capita household incomes in the year to Q1 2025:

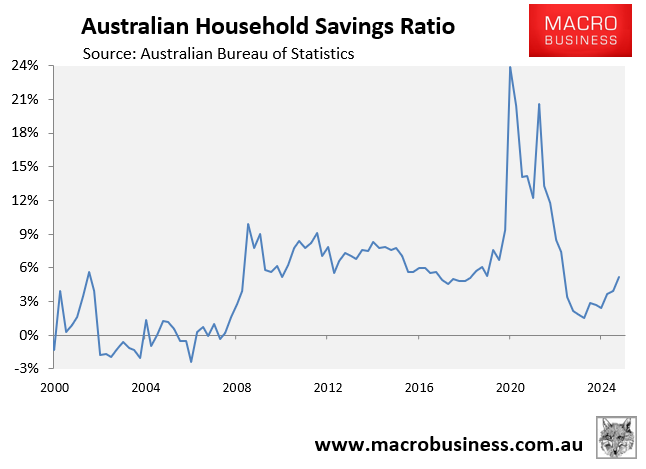

The gap between income and spending increased the household savings rate to 5.2% in Q1 2025, up from 2.7% the year before and the highest percentage since Q3 2022:

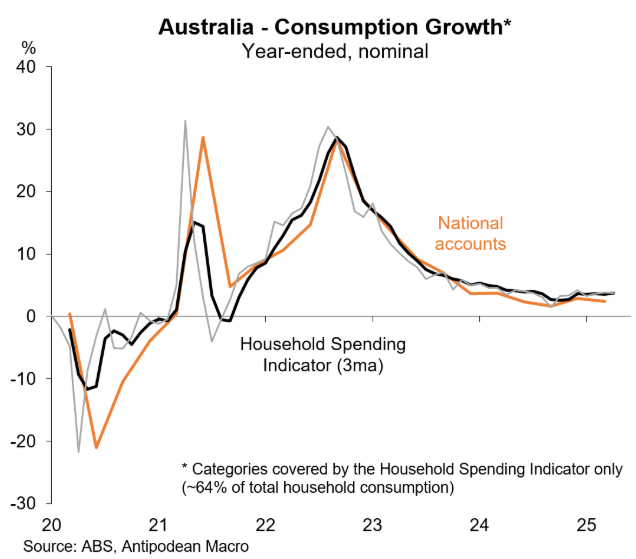

The ABS also released its Monthly Household Spending Indicator (MHSI) last week, which increased by only 0.1% over the month and 3.7% annually, continuing the trend of weaker consumer spending data in 2025.

The chart presented below by Justin Fabo from Antipodean Macro confirms that there has been no shift higher in spending momentum:

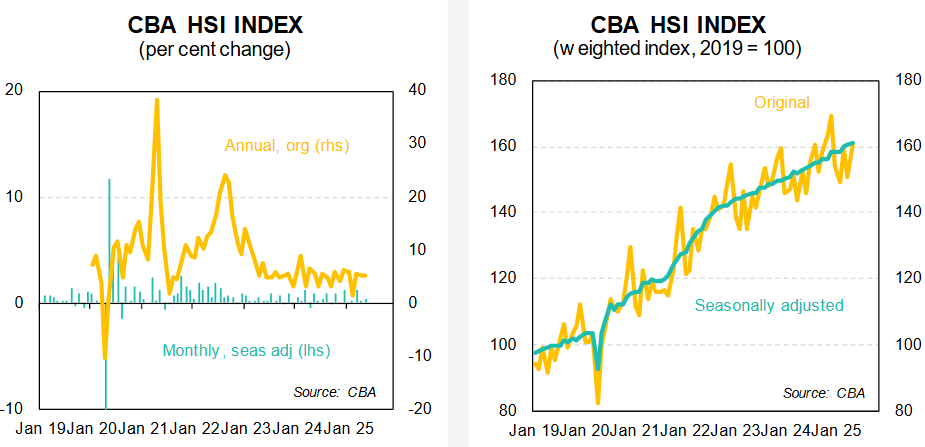

CBA has released its Household Spending Insights (HSI) for May, which reported a 0.5% increase in spending, which followed April’s flat result. This took the annual rise to 5.2% in nominal terms.

“The consumer spending rebound is unfolding at a slower rate than we expected, which could be the result of scarring from a loss of real household income post-COVID, and the impact of global uncertainty caused by trade tensions”, said Belinda Allen, Senior Economist at CBA.

“We are seeing some green shoots however, as our insights suggest households are using money saved from energy rebates and lower petrol prices to enjoy themselves by dining out and spending on experiences”.

In annual three-month smoothed terms, household spending per capita grew by only 3.2%, compared with CPI inflation of 2.4%.

Therefore, the increase in disposable income from the Stage 3 tax cuts and falling interest rates has so far not translated into spending, with households choosing to save instead.

Further interest rate cuts will free up more disposable income and should stimulate spending. But it is unlikely to meet the RBA’s expectations:

Source: Alex Joiner (IFM Investors)