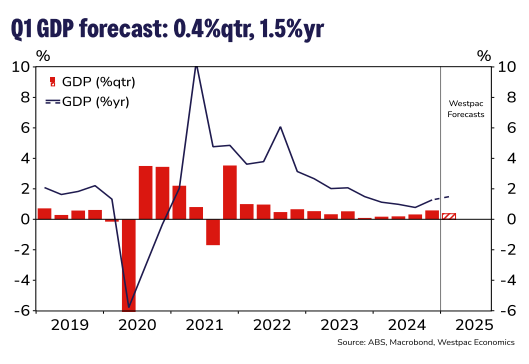

Westpac is reading the economy right as examines Q1 GDP.

Domestic demand is expected to have slowed, lifting only 0.3%qtr in Q1. As growth in new public demand moderates, private demand remains patchy and at this stage, unable to pick up the slack left by the public sector.

The impacts of the natural disasters which occurred in the quarter were partially offset by a bring forward of external demand. This suggests the Accounts will provide a reasonable gauge on the underlying growth impulse.

As lower interest rates add to the support already coming from cost-ofliving measures, tax cuts and moderating inflation, private demand is expected to gradually improve. However, as the run of recent data shows, there are significant downside risks which the evolving global backdrop is only amplifying.

The RBA has run the economy into the ground just in time for the external shock of the Trump administration to stall it completely.

Last week’s retail sales, CAPEX data, and building approvals all signaled an economy at stall speed.

The ructions of the Trump administration were not entirely predictable. He had foreshadowed trade and other shocks but not to the extent that was exacerbated by very poor policy implementation.

So we can perhaps forgive the RBA for factoring that in.

Yet it has been obvious for many months that the RBA had won the battle against inflation, and refusing to acknowledge this simple fact, they were always running the risk that something unexpected could land upon an economy that was unprepared to absorb it.

The RBA remains the world’s most stupid central bank for one simple reason.

It refuses to mention the word “immigration”. And given Australia is running a unique immigration-led, labour market expansion economic model, this omission goes from being stupid to corrupt.

Put another way, in contemporary parlance, I am a “racist” but at least I can forecast monetary policy.

The RBA need to cut by 50bps in June.