Following a wave of softer-than-expected data and the dovish May RBA decision, CBA has revised its expectations for interest rate cuts forward.

“We now expect the RBA to cut the cash rate by 25bp to 3.60% at its 7-8 July meeting”, CBA senior economist Belinda Allen wrote. “And a follow up 25bp rate cut in August”.

“Today’s monthly CPI print capped off a flow of data that should provide comfort to the RBA that a swifter return of the cash rate to neutral is both manageable and needed”, Allen wrote.

CBA points to three particular pieces of economic data that have prompted it to bring forward its rate cut forecasts.

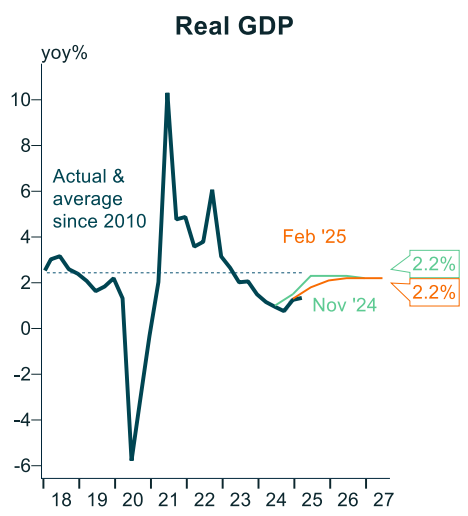

First, GDP printed below expectations at just 0.2% for Q1 and 1.3% annually, below RBA estimate of 0.4% quarterly growth.

Chart by Alex Joiner (IFM Investors)“A fall in public demand for the first time since Q3 22 should provide a reminder of the tricky handover from public to private sector growth needed this year to support the recovery”, Allen noted.

“The consumer was also subdued and the flow of data on the consumer in Q2 25 to date also suggests a still tepid recovery”.

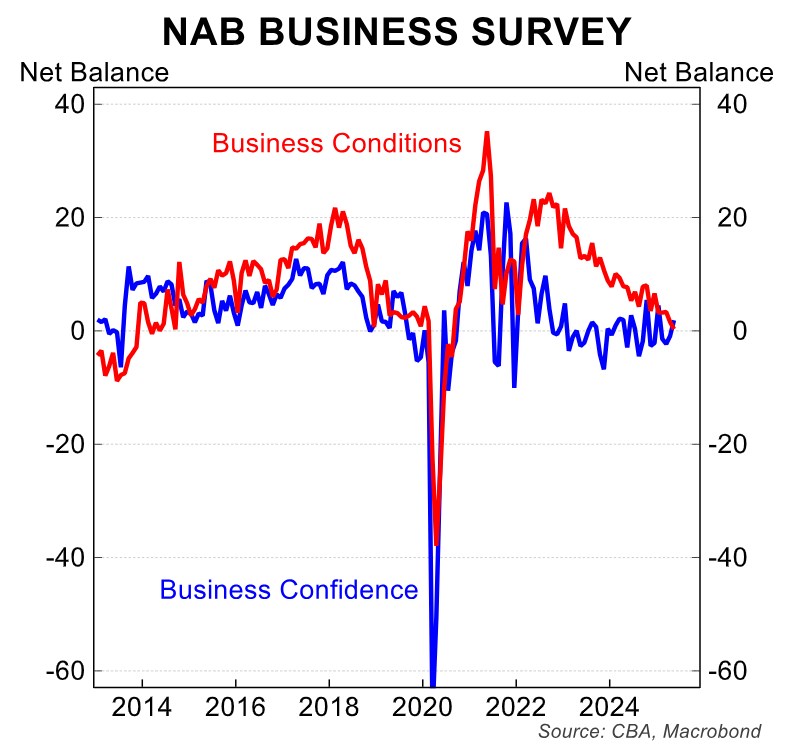

Second, business and consumer sentiment are weak.

“The closely watched NAB business survey took a turn down in May, with business conditions sitting below the long-term average”, Allen noted. “The employment subcomponent also reached a cycle low”.

“The pricing components in both the NAB survey and PMIs also confirm that disinflation momentum in the Australian economy is continuing”.

Third, the May labour market data saw the unemployment rate steady at 4.1% for the fifth consecutive month.

“Still limited signs of unsustainable wages growth continues to suggest the non-accelerating rate of inflation (NAIRU) is around current levels”, Allen noted.

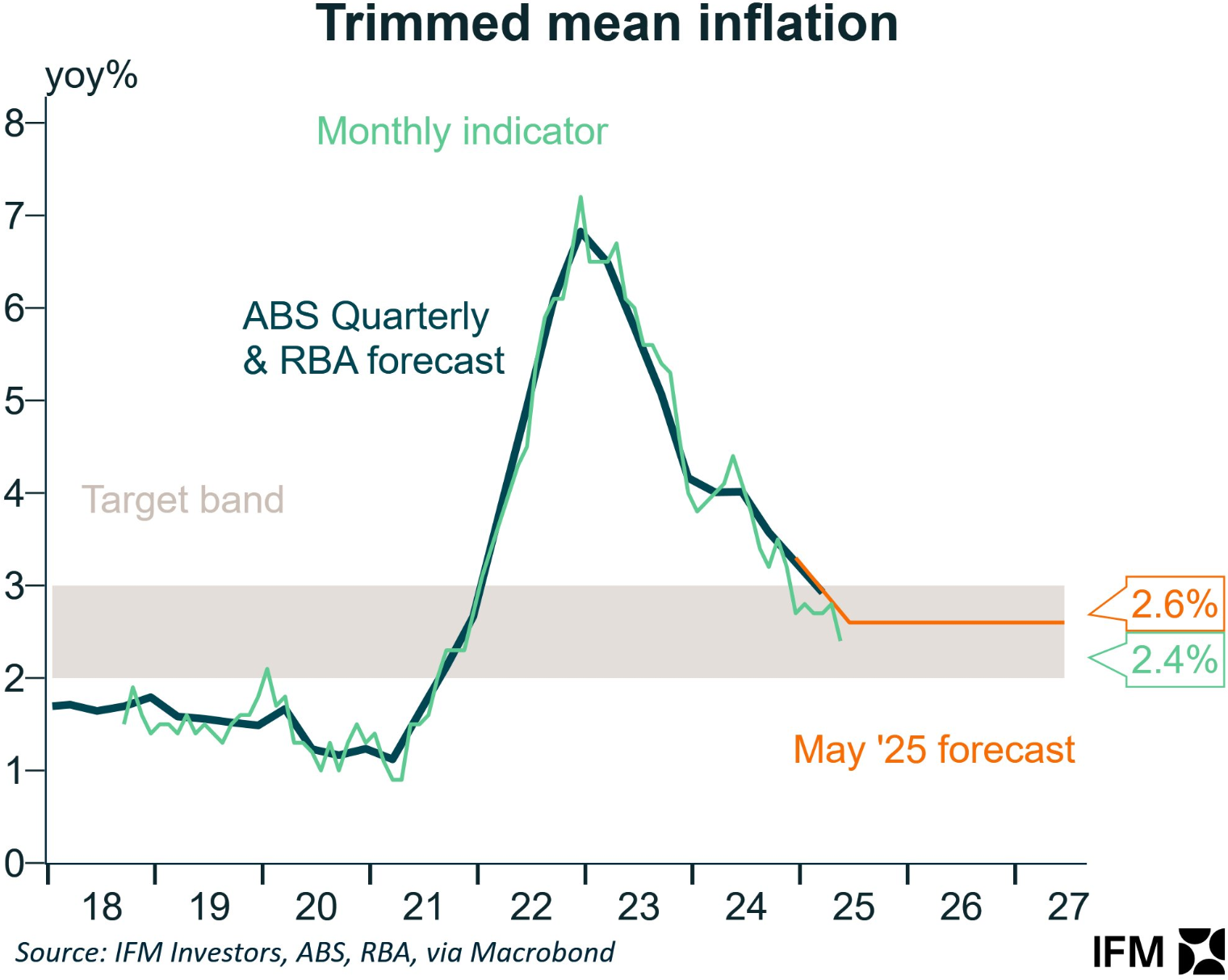

Finally, the May CPI Indicator, released today, printed at 2.1% annually, below the CBA’s and the consensus estimate of 2.3%/yr.

“We expect there is enough evidence for the RBA that the disinflation pulse in the economy should continue and inflation should sit around the mid-point of the target band”, Allen noted.

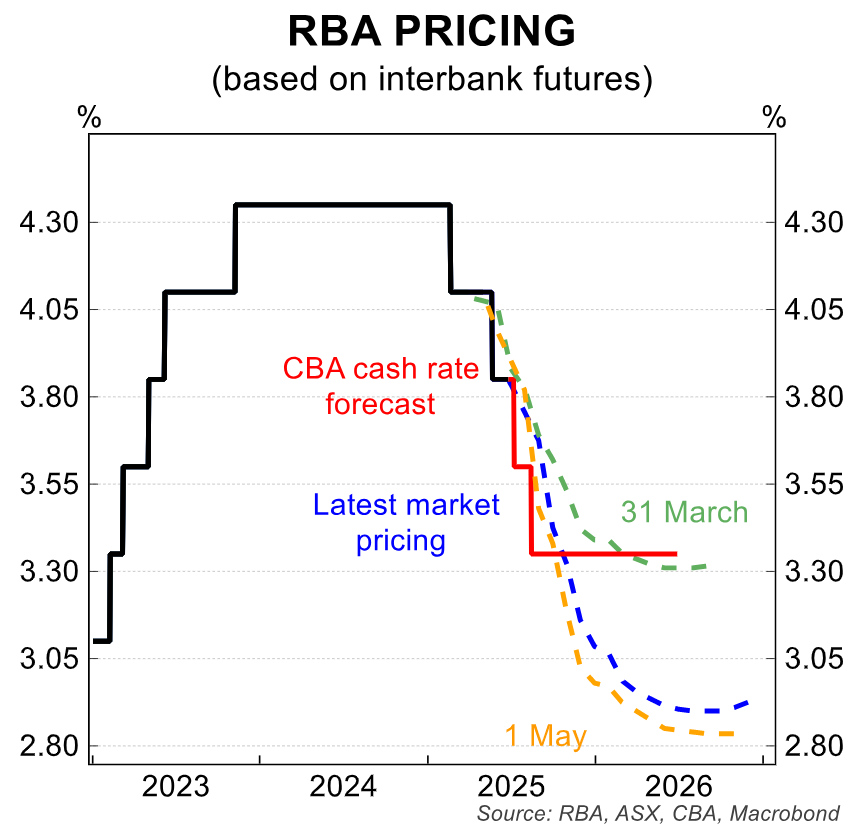

As a result, Allen believed “the path is clear for the RBA to move the cash rate swiftly back to a more neutral rate of ~3.35%”.

“The risk sits with a further rate cut later in 2025 or early 2026, depending on the transition of growth from the public to private sector and the possibility that this could see inflation undershoot the midpoint”.

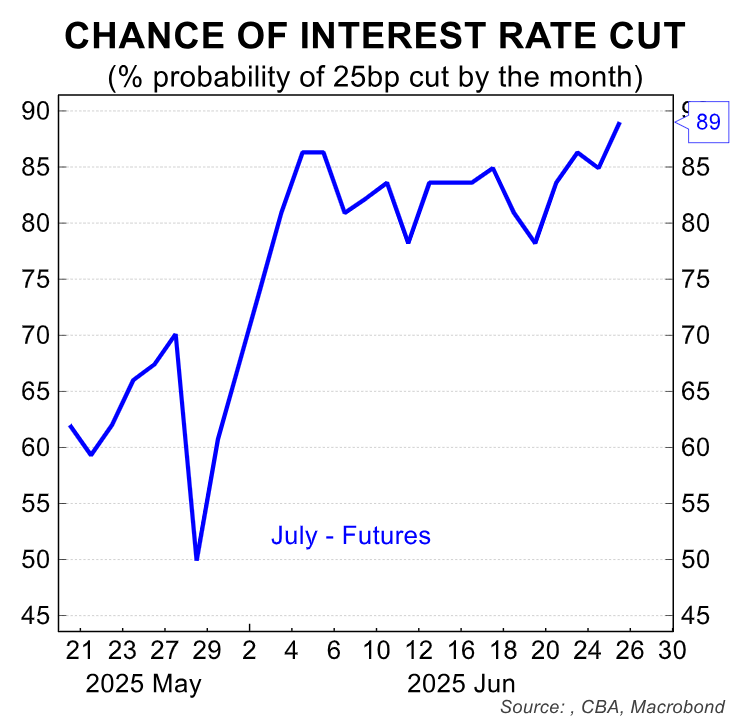

Financial markets have ascribed a circa 90% probability of a July rate cut.

The market then expects a further two 25 bp rate cuts this year, taking the cash rate to 3.10%, followed by one last 25 bp cut in 2026 to a terminal low of 2.85%.

As shown above, the market’s rate cut pricing is more dovish than CBA’s.

I share the market’s perspective, recognising that the unpredictable global geopolitical landscape poses a significant downside risk.