Livewire with the note.

CBA operates in a domestic banking market with limited credit growth in Australia, selling an identical product to that offered by four other competitors (now including Macquarie), all of which have the same cost of production (capital).

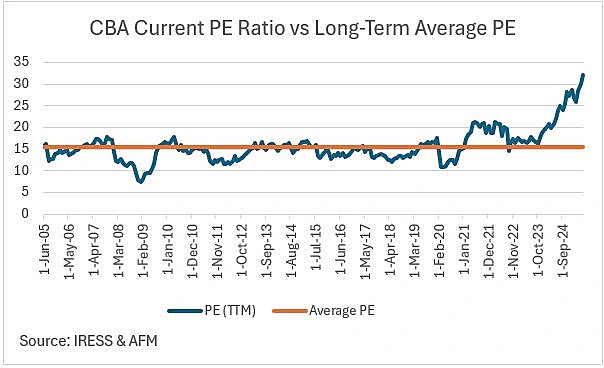

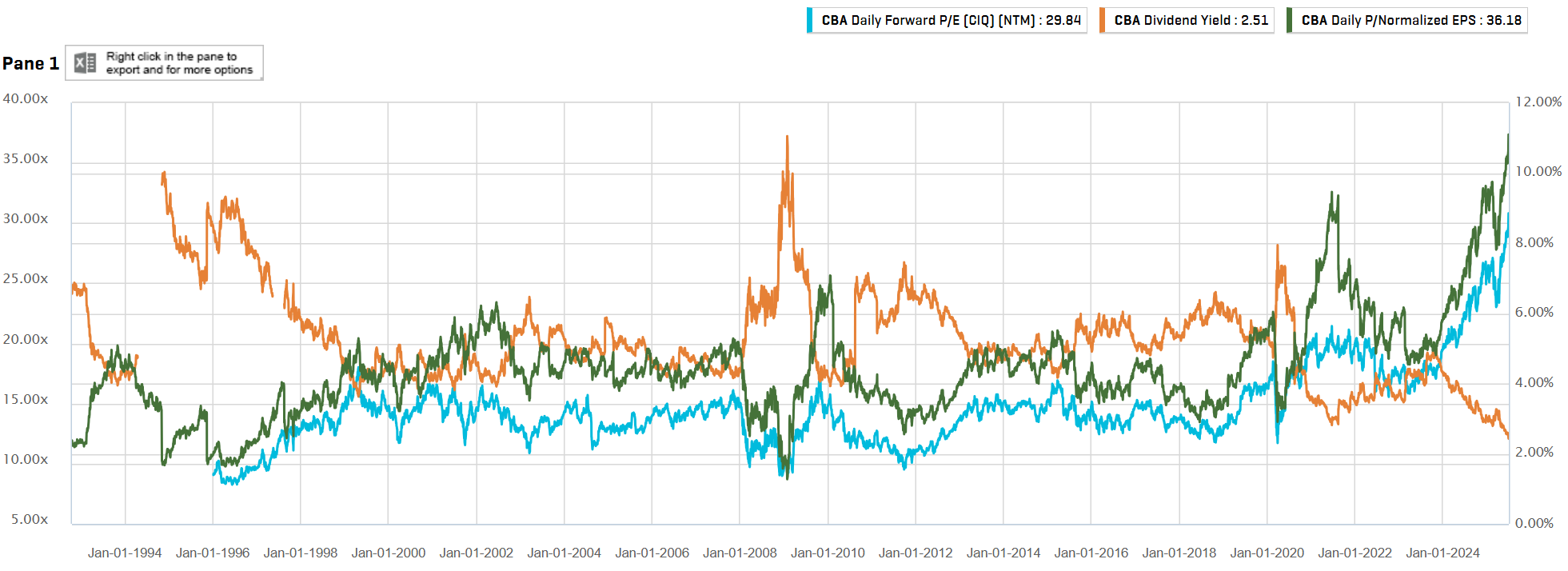

This current rally has seen CBA move into the world’s top ten most valuable banks and become the first developed market bank in history to trade at a multiple greater than 30 times earnings.

One of the key drivers behind CBA’s meteoric rise has little to do with its earnings or strategy. Instead, it’s the sheer weight of money flowing into passive investment vehicles.

As the largest constituent of the ASX 200, CBA receives the lion’s share of every dollar that flows into index-tracking funds, such as Vanguard’s VAS or Betashares’ A200.

This creates a self-reinforcing loop: rising prices attract more inflows, which in turn push prices higher. It’s a virtuous cycle—until it isn’t.

Hmm, that’s part of the story. There is more to it.

- The global Value trade is red hot, which means buying banks. If you have an Australian mandate, then what else is it to be?

- Boomer retirement is playing some role, as they double down on their winnings.

- In Australia, the game of funds management is won by picking one of two sectors to outperform: mining verus banks. The former is in a bear market for the ages, forcing everyone into the latter.

The numbers are ridiculous.

The valuation is absurd, higher than most tech stocks. The dividend loses money in real terms. There is some EPS growth, but that is obviously cyclical with a shift to higher interest rates pumping mortgage backbook profits.

That’s the key to when this busts. Most forecasters see interest rates structurally higher post-COVID. I do not.

I do not expect the lows of the previous cycle owing to big spending Labor everywhere. But even Labor will have to cut as the bottom falls out of the terms of trade over 2026/27.

As 200mt of new iron ore supply—most notably from the Pilbara killer, Simandou—meets Chinese demand falling at 30-40mt per annum over 2026/27, interest rates will go much lower than most expect.

Moreover, money will begin to shift back into mining as underlying commodity prices crater.

Some may argue that CBA will be fine as volume growth picks up. But there is far less leverage to profits in this than there is in rapidly declining net interest margins.

The last four occasions that CBA bubbles burst—2000, 2008, 2010 and 2020—these were the prevailing conditions that did it.