Following one of the largest increases in the industrialised world during the Covid-19 pandemic, New Zealand’s housing prices fell sharply.

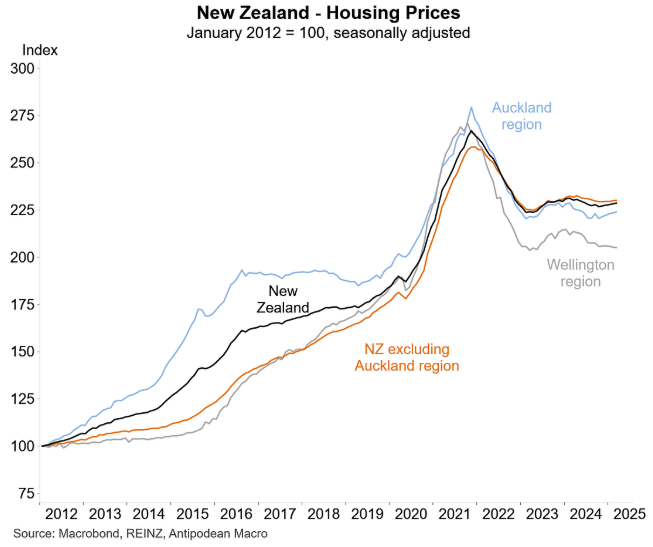

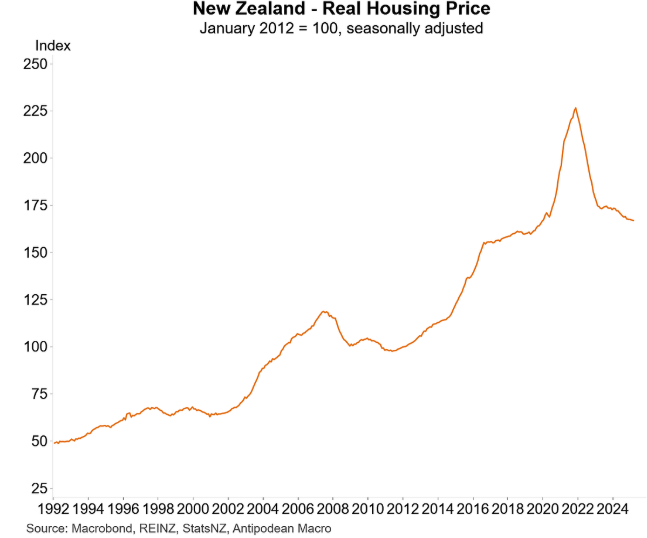

According to the REINZ home price index, presented below by Justin Fabo from Antipodean Macro, New Zealand’s real inflation-adjusted home prices have reverted to pre-pandemic levels.

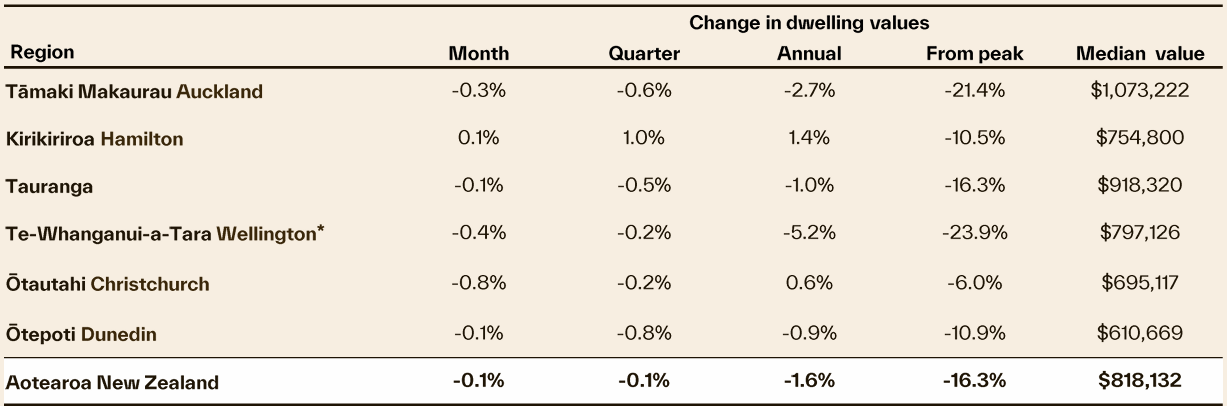

Separate data provided this month by Cotality reported that New Zealand home values continue to decline, falling by 0.1% in May to be 1.6% down year on year and 16.3% below the peak:

Source: Cotality (May 2025)

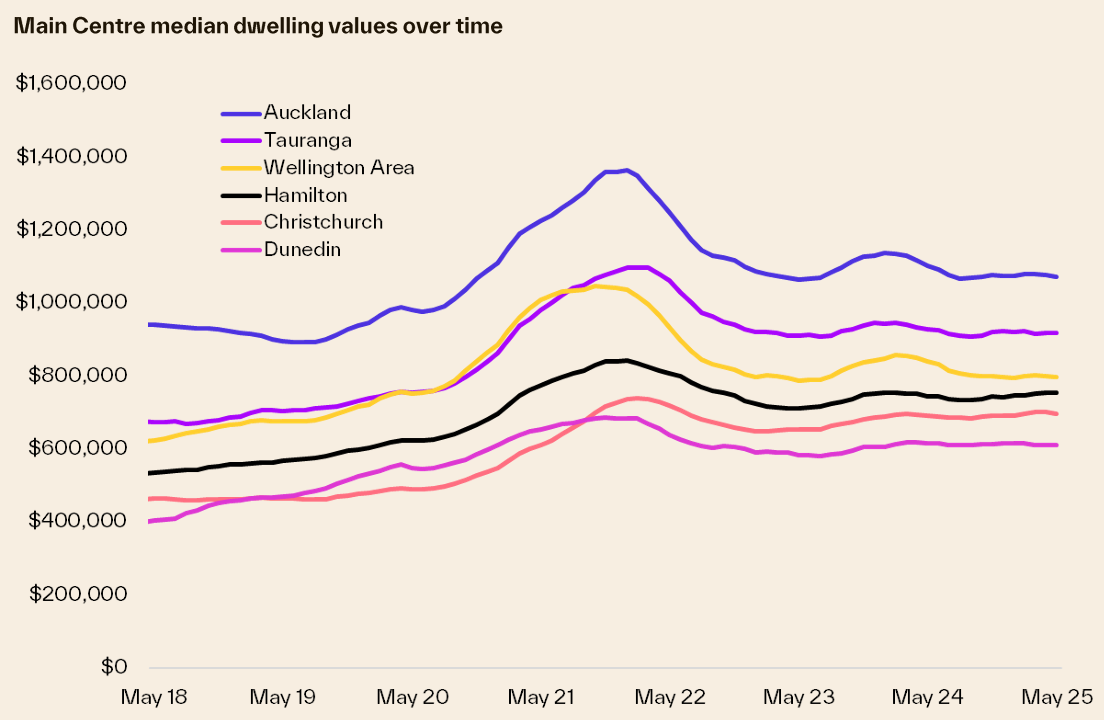

The following table from Cotality illustrates the declines from peak throughout the major centres of New Zealand:

Source: Cotality (May 2025)

Auckland (-21.4%) and Wellington (-23.9%) have led the decline in New Zealand home prices.

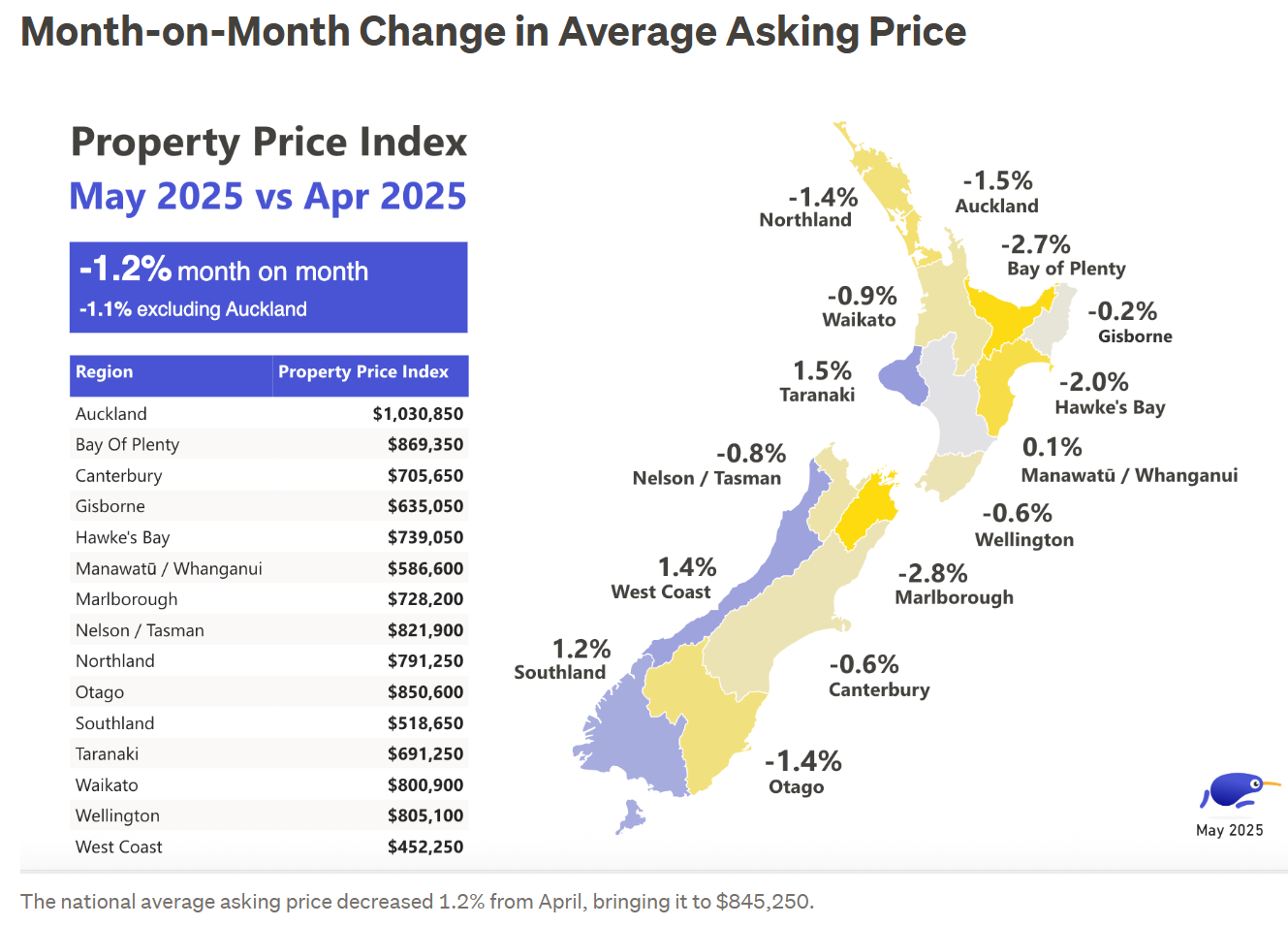

TradeMe’s property price index shows similar results, recording a 1.2% decline in national average asking prices in May, which follows April’s 0.8% decline.

Each main centre recorded declines in their average asking prices in May, with Auckland, Wellington, and Canterbury recording their lowest prices since September 2024.

“Buyers tend to take a little more time in the winter months and the current market is already showing signs of this slow down with median days onsite sitting at 70 in May, up from 62 in April”, noted TradeMe Customer Director, Gavin Lloyd.

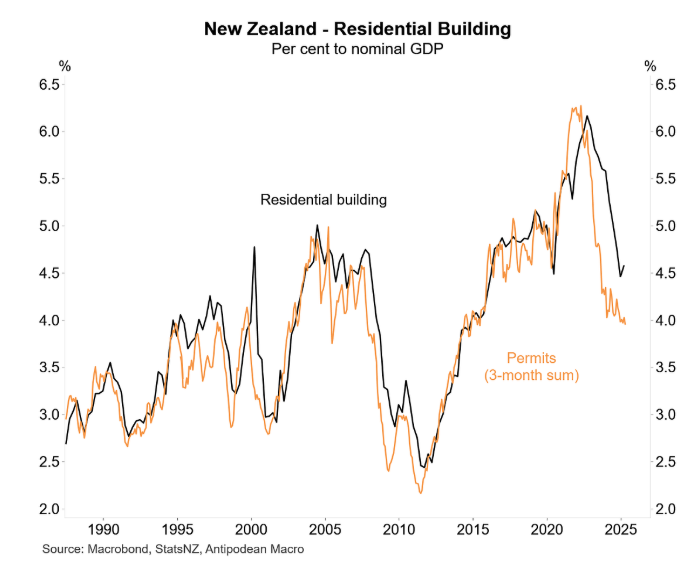

The construction side of the housing market has also tanked, as illustrated below by Justin Fabo:

Major bank ASB said that “we’d be remiss if we didn’t state that construction activity has been surprisingly frail”, which appears to be an understatement given the Reserve Bank of New Zealand’s 2.25% monetary easing.

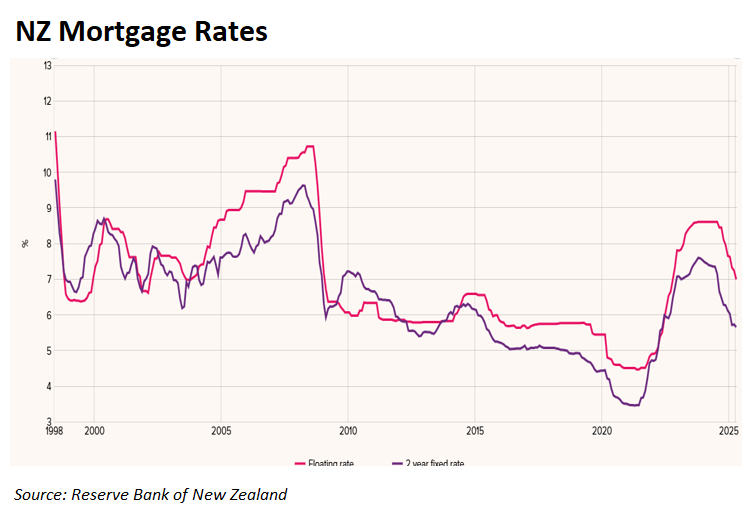

Falling mortgage rates have greatly increased affordability, which should have boosted demand, prices, and construction activity.

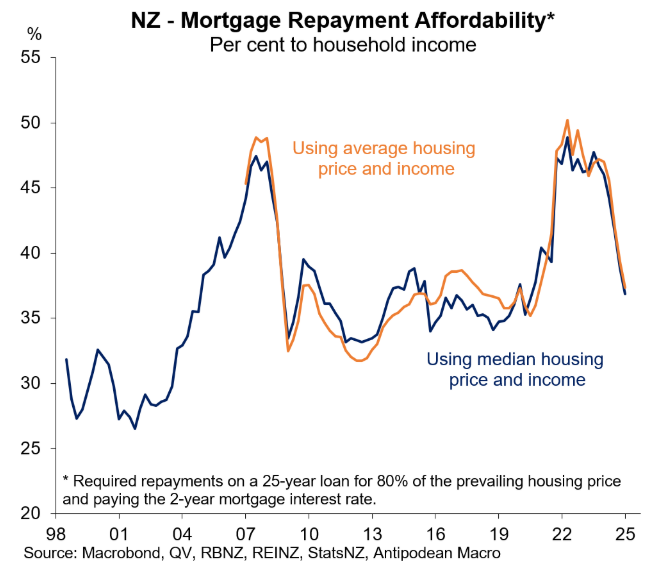

Mortgage payments as a percentage of household income have decreased from around 50% to little more than 35%.

Kelvin Davidson, Chief Property Economist at Cotality NZ, stated that, while “lower mortgage rates are clearly going to be bolstering households’ confidence as well as their wallets”, there remain “restraints on buyers’ willingness to push ahead with property deals or to pay higher prices”.

This means that “anybody who was anticipating a sharp or widespread increase in property values as we got further into 2025 continues to be disappointed”.

As a result, property buyers in New Zealand are in a strong position, with vendors lowering prices and borrowing rates reducing.

At least housing in New Zealand is becoming much more affordable, unlike in Australia.