New Zealand shames Australia on housing affordability

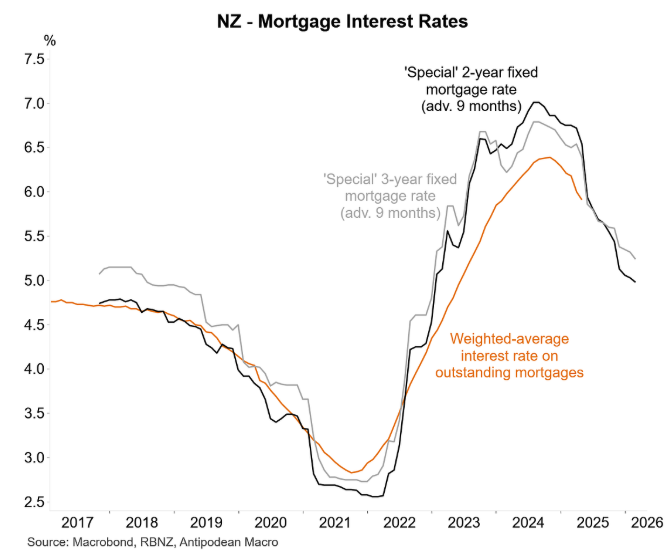

Justin Fabo from Antipodean Macro posted the following chart, which shows the collapse in mortgage rates in New Zealand.

“The weighted-average interest rate on outstanding mortgages in New Zealand declined another 9bps to 5.91% in April, taking the cumulative fall to nearly 50bps since the peak”, noted Fabo. “More is coming”.

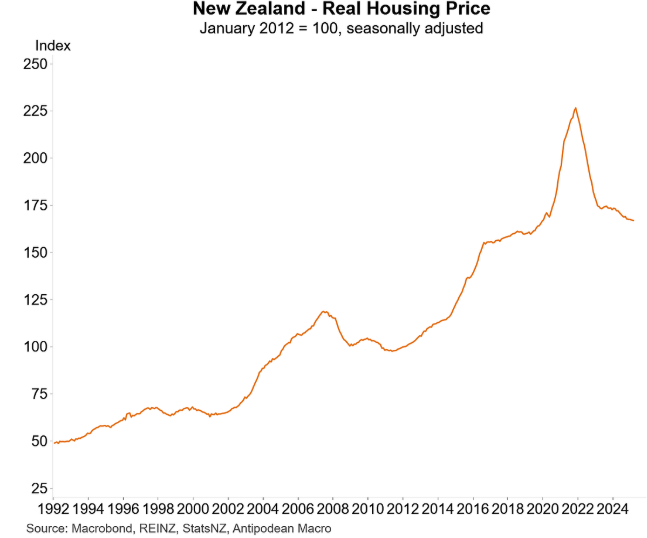

Falling mortgage rates have been accompanied by a sharp decline in house prices, which have fallen to pre-pandemic levels in real inflation-adjusted terms:

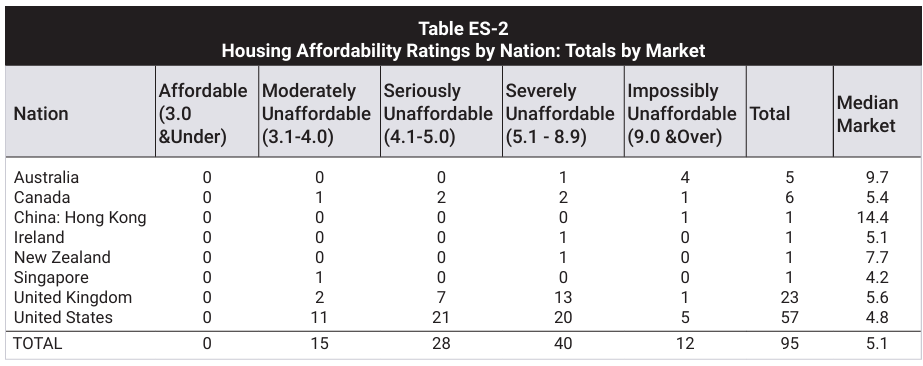

Indeed, the latest Demographia housing affordability survey, released last month, showed that New Zealand’s median multiple (i.e., median house price divided by median household income) had fallen to 7.7 in 2024, down from 11.2 in 2021.

Source: 2025 Demographia Housing Affordability Survey

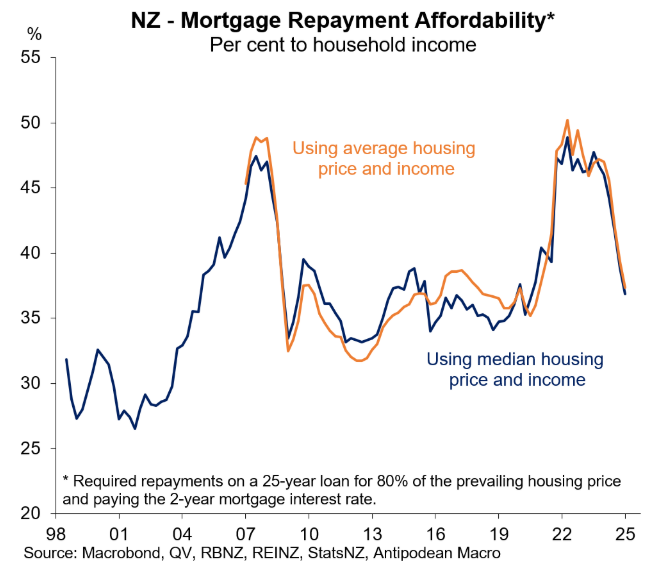

As a result, the percentage of median income required to service a median new mortgage in New Zealand has decreased from around 50% to 35%, with further reductions expected as average mortgage rates decline.

The affordability situation in New Zealand contrasts with Australia, whose median multiple increased from 8.0 in 2021 to 9.7 in 2024, according to Demographia.

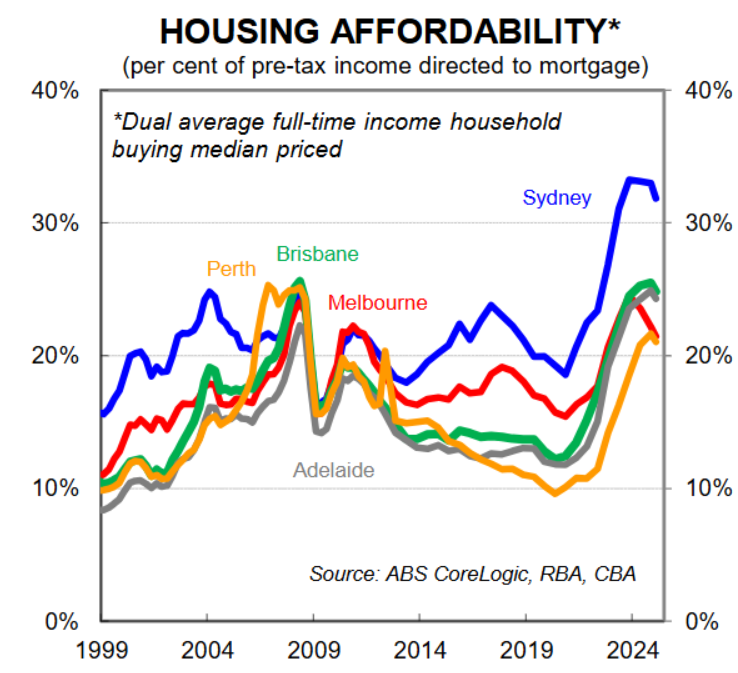

Australia’s mortgage affordability is also tracking near its worst level in history.

While mortgage affordability will improve as interest rates decline, Australian home prices are also likely to rise above their current record levels, which will make affordability structurally worse.

The Albanese government’s 5% deposit scheme for first home buyers, which is scheduled to come into effect on 1 January 2026, will add further to demand and drive prices higher.

Ultimately, achieving more affordable housing requires that home prices fall. New Zealand’s politicians seem to understand this concept.

Australia’s politicians do not share this view, which explains why they continually introduce stimulatory policies to boost mortgage demand and prices.