New Zealand’s economy is a basket case. Consider the following data points, many of which come from Justin Fabo from Antipodean Macro.

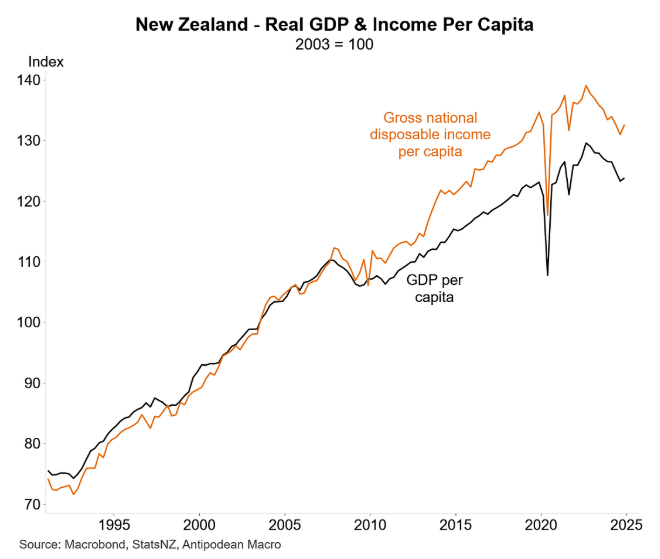

The following chart of national accounts data to Q4 2024 shows that New Zealand has experienced a sharp decline in GDP and national income.

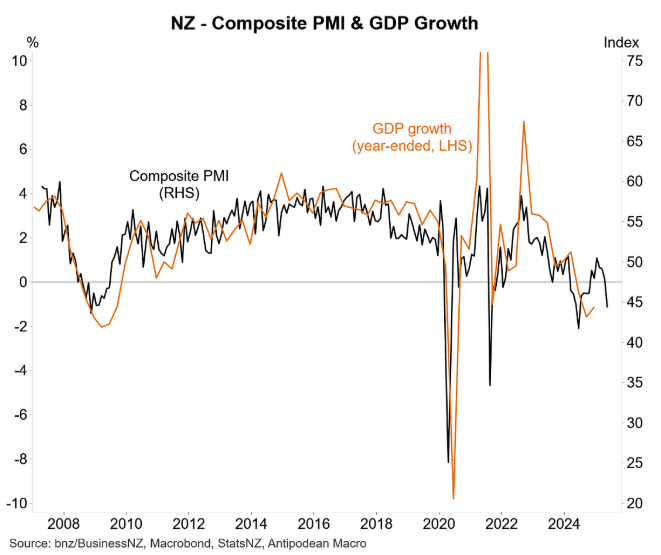

More recent data suggests that the economy remains moribund.

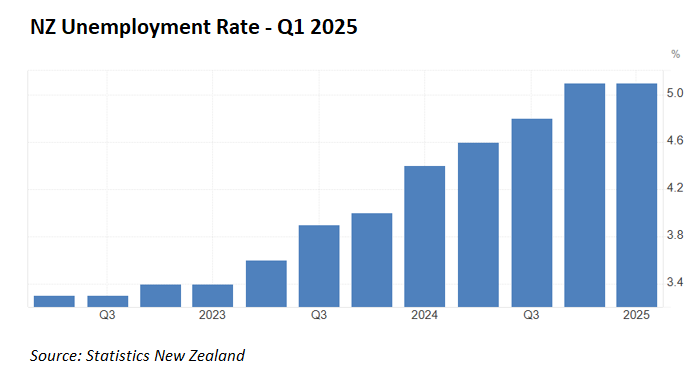

New Zealand’s unemployment rate has increased to 5.1% as of Q1 2025:

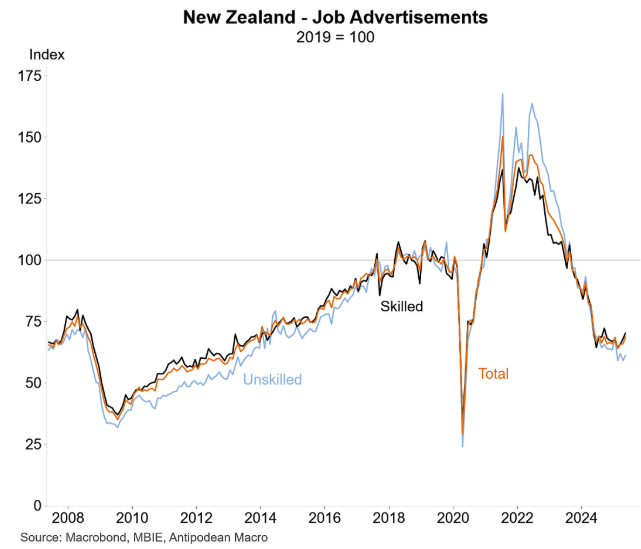

The latest MBIE survey showed that job advertisements in New Zealand have fallen well below pre-pandemic levels; although they have at least stabilised.

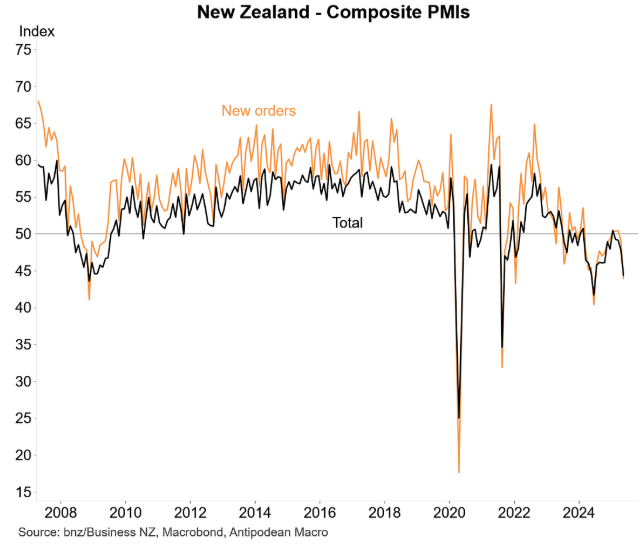

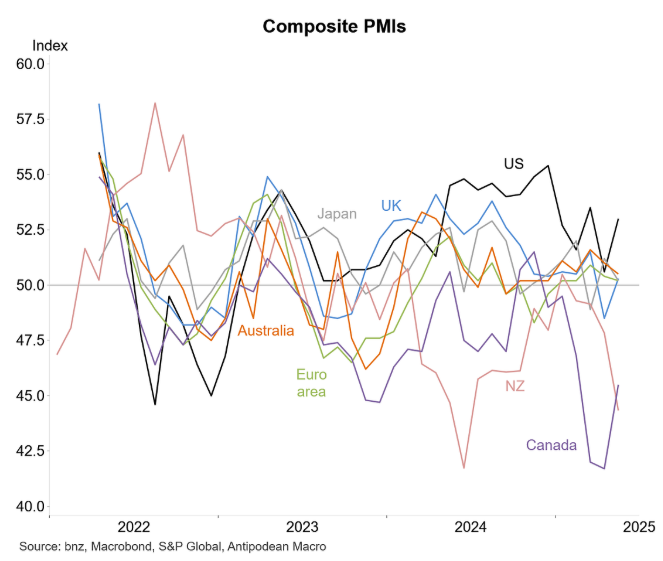

New Zealand’s composite PMI tanked in June, with new orders also plunging:

The decline in New Zealand’s composite PMI is among the worst in the developed world:

The decline in New Zealand’s composite PMI suggests that GDP growth will decline in Q2 after rebounding in Q1.

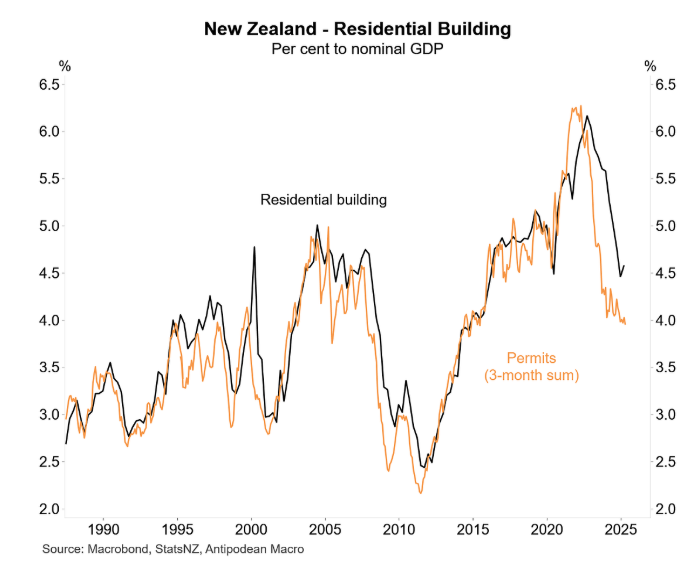

Residential building activity has also tanked.

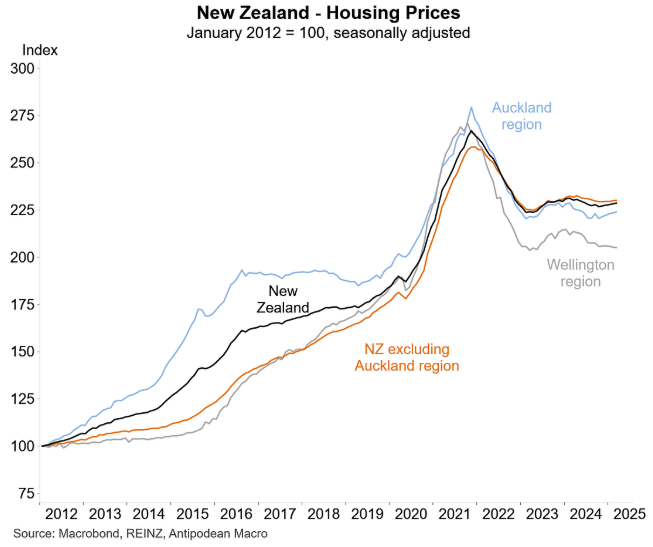

As have residential housing prices.

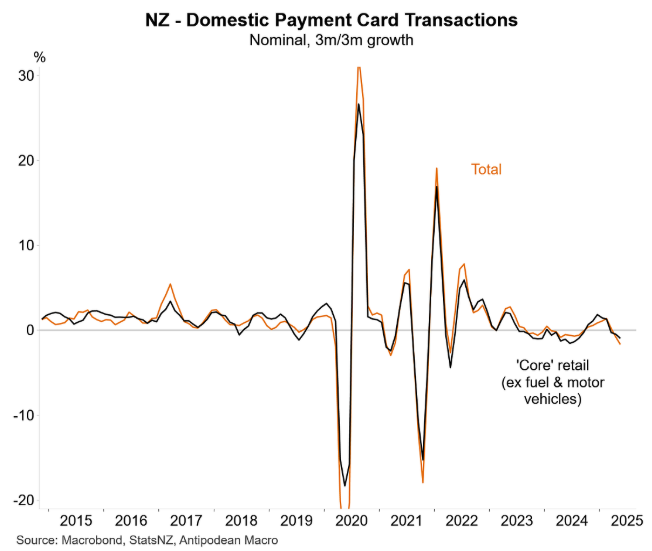

The latest data on core and total retail spending also remains anaemic, suggesting that consumers have tightened their purse strings in response to the weak economy.

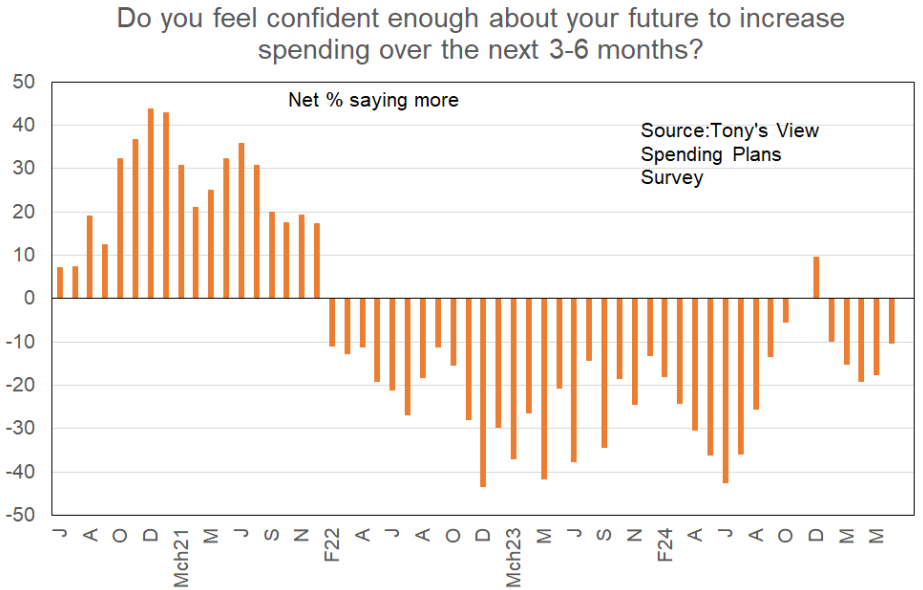

The outlook for consumer spending also looks soft, with independent economist Tony Alexander’s latest survey of monthly spending plans showing that the net proportion of consumers planning to spend more remained negative (-10%) in May:

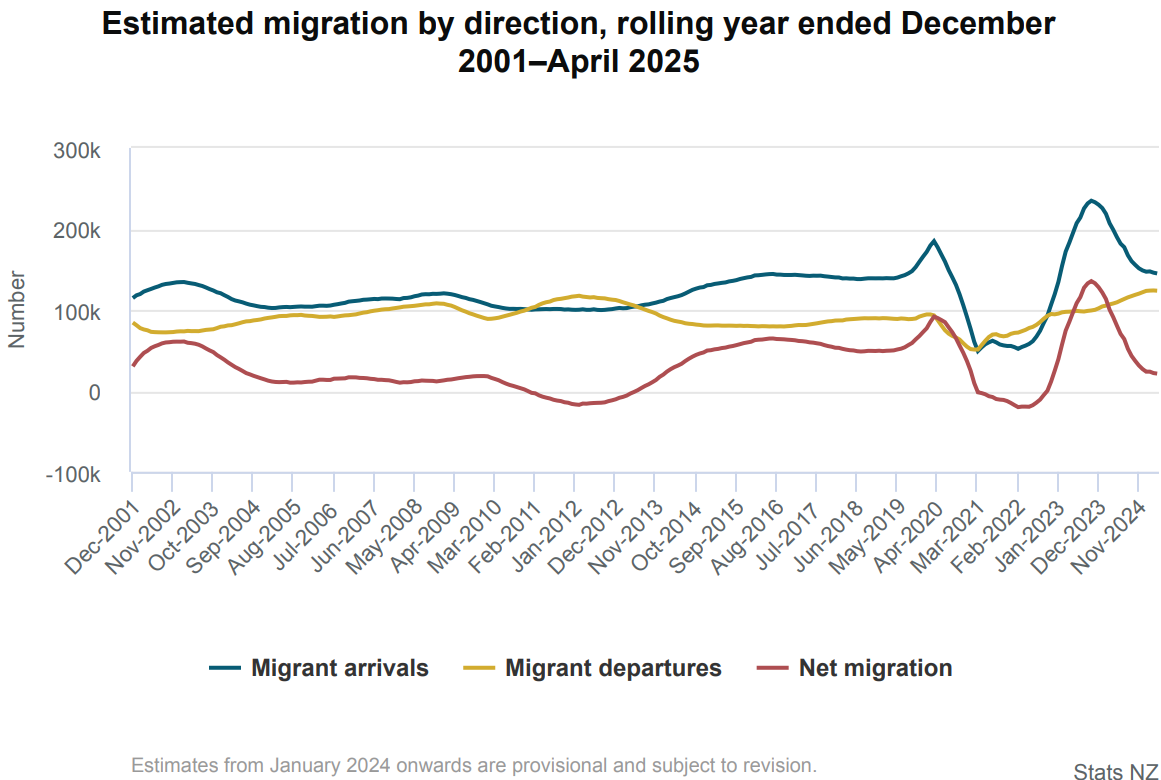

Finally, net overseas migration into New Zealand has fallen to its lowest level in 2½ years:

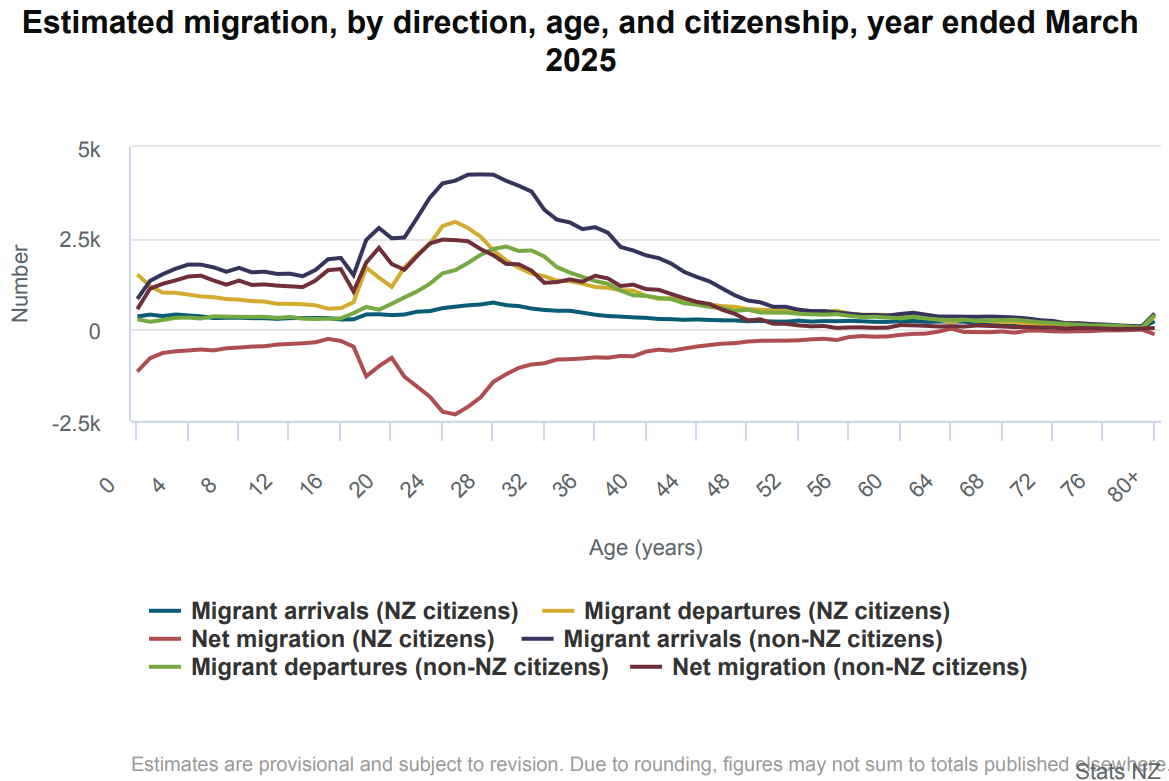

In particular, New Zealand is suffering a brain drain of prime-age Kiwis, with 18- to 30-year-olds comprising 27,200 (39%) of the 70,000 migrant departures of citizens in the March 2025 year.

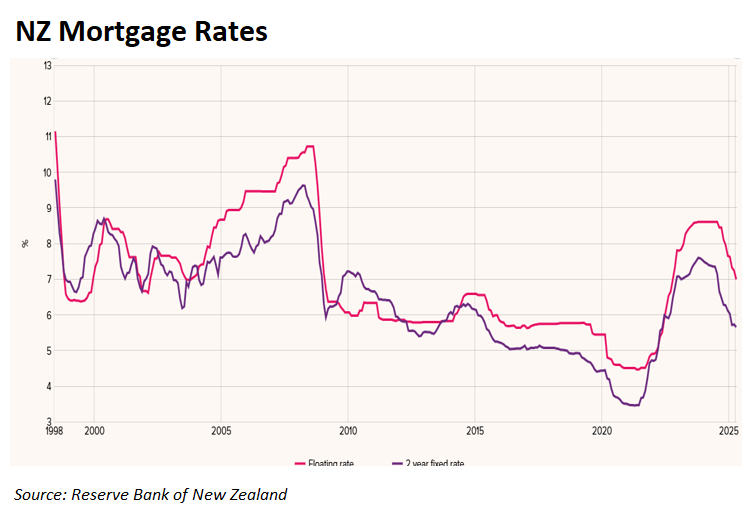

The above data explains why the Reserve Bank of New Zealand has slashed the official cash rate by 2.25%.

The Reserve Bank will need to lower rates further to stimulate the economy.