The start of the new trading week is coinciding with the end of the month and for some, the financial year, which is leading to a lot of window dressing across risk markets in Asia. However Wall Street is riding the wave higher after the Canadians gave in to the public demands of the Trump regime with a concession on their digital tax as part of trade negotiations but that is not stopping the selloff in the USD against, well everything.

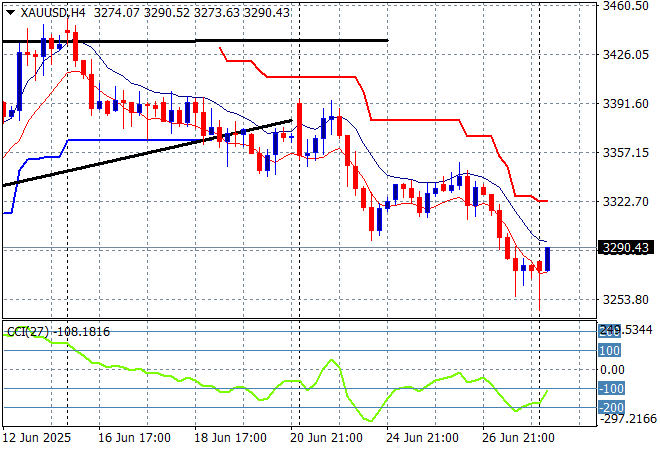

Oil markets continue to steady after their recent correction with Brent crude trading just above the $66USD per barrel level while gold is trying to make a comeback but is still above the $33000USD per ounce level:

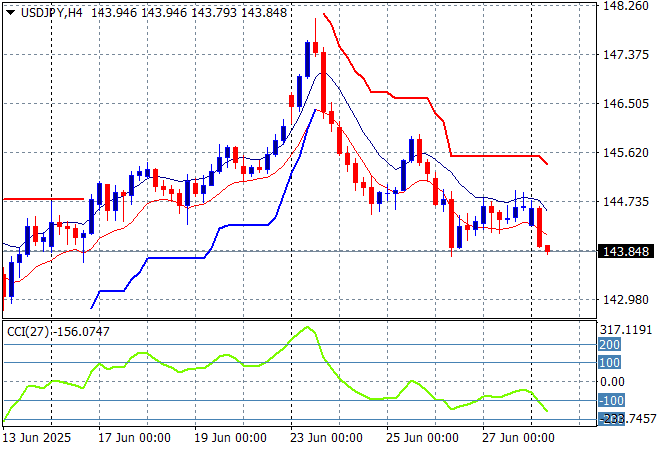

Mainland Chinese share markets are up slightly with the Shanghai Composite remaining above the 3400 point level while the Hang Seng Index is pulling back around 0.4% or so but still maintaining a strong position above the 24000 point level. Meanwhile Japanese stock markets are doing very well with the Nikkei 225 lifting more than 0.7% higher to extend further above the 40000 point barrier with the USDPY pair retreating well below the 144 level:

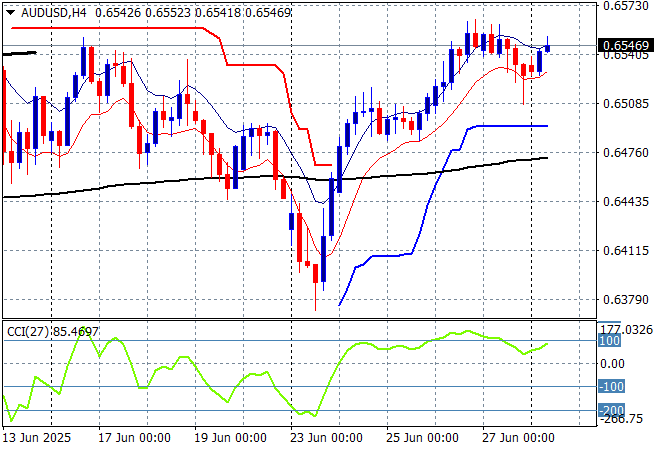

Australian stocks are finally finding some positivity with the ASX200 closing 0.5% higher at 8557 points while the Australian dollar was able to slightly extend above the 65 handle after the weekend gap on the weaker USD:

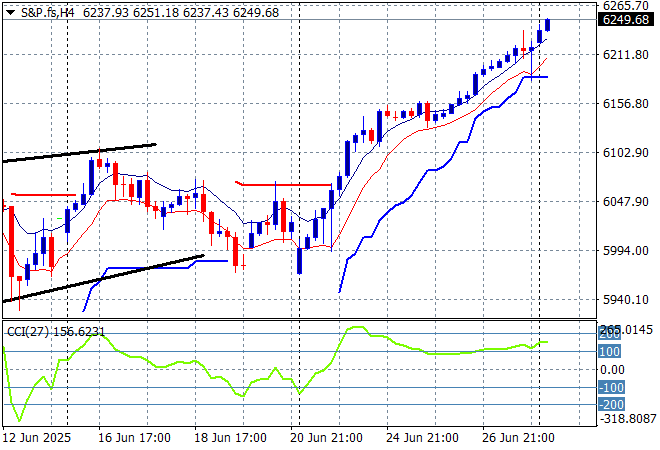

S&P and Eurostoxx futures are up strongly going into the London session with the S&P500 daily chart showing the market clearly overextended but still turning any news into outsized returns after breaking right through the 6200 point level:

The economic calendar starts the trading week with some more European inflation figures and end of month/quarter/year shenanigans.