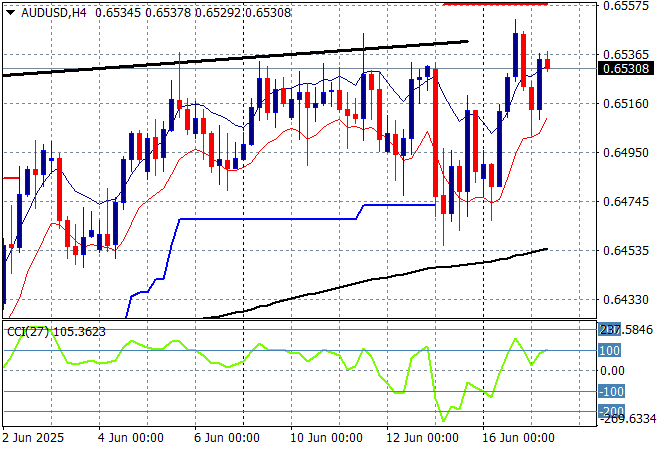

The Israel-Iran war continues to dominate risk markets as Trump runs away from the G7 meeting tweeting out incoherent threats and deals while further strikes against oil tankers and other targets show the conflict spreading. The USD remains somewhat weak although Yen took a small back seat on today’s BOJ meeting with a taper plan on future bond purchases announced. The Australian dollar remains slightly above the 65 cent level despite the risk off mood.

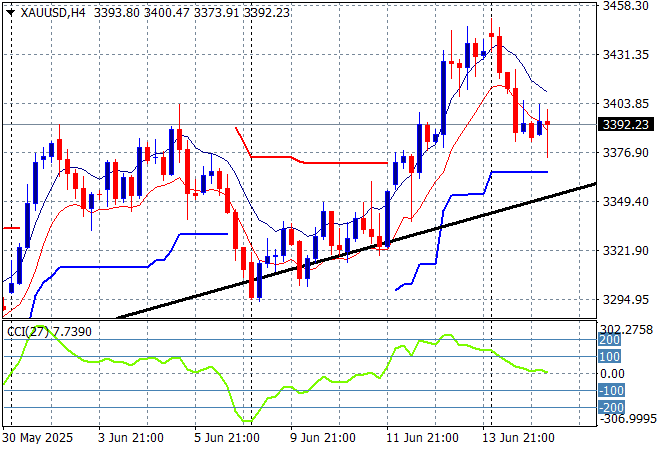

Oil markets are lifting higher on the Iranian strikes and the oil tankers on fire in the Gulf with Brent crude lifting back above the $75USD per barrel level while gold is also holding on at its recent losses where it slipped back below the $3400USD per ounce level:

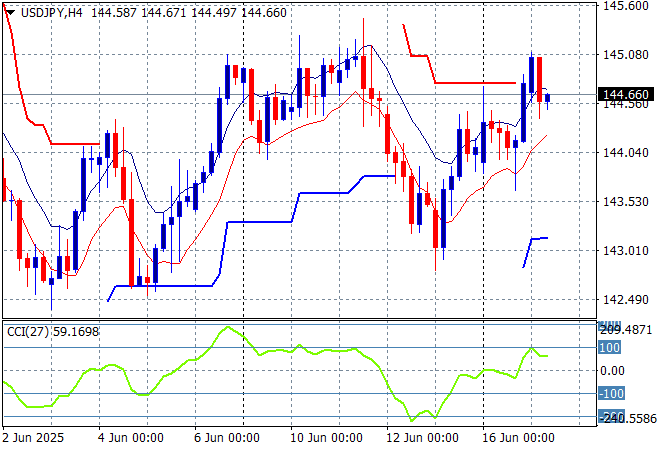

Mainland Chinese share markets are somewhat steady going into the afternoon session as the Shanghai Composite remains slightly below the 3400 point level while the Hang Seng Index has slipped 0.6% or so to get back below its own recent resistance level at 24000 points. Japanese stock markets are pushing higher on the BOJ non decision with the Nikkei 225 moving up more than 0.5% to 38504 points while trading in the USDPY pair has seen a very small retracement as it fails to beat the previous weekly high, holding above the mid 144 level:

Australian stocks have slipped slightly with the ASX200 closing 0.1% lower at 8541 points while the Australian dollar has continued its strong start to the week to remain well above the 65 handle despite the war tensions:

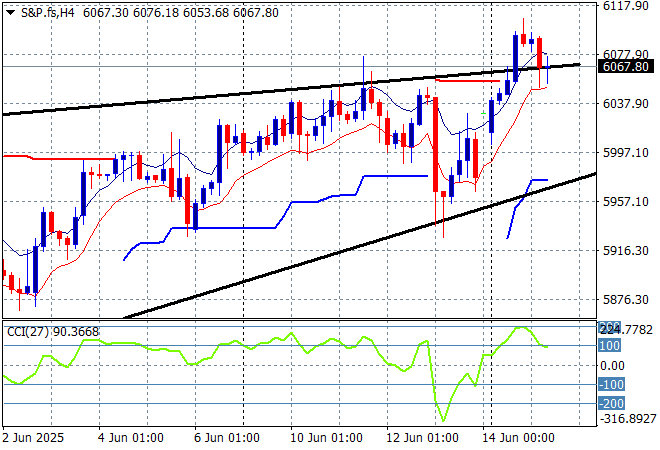

S&P and Eurostoxx futures remain surprisingly robust with the S&P500 four hourly chart previously showing a desire to remain above the recent highs at the 6000 point level but this could be a short term momentum reversal :

The economic calendar continues with the closely watched German ZEW survey then US retail sales.