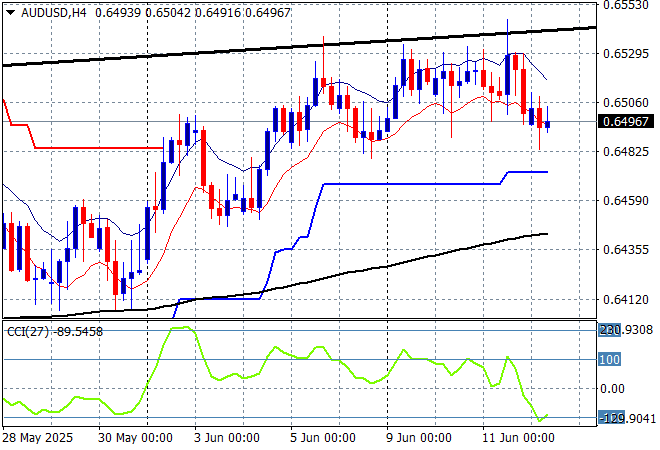

Middle East tensions are dominating risk taking here in Asia with most share markets finishing in the red, not helped by what looks like a “non-deal” deal from the ongoing US/China talks, regardless of what the Trump regime claim has come to pass. The USD continues to fall against the majors despite a very tame May inflation print overnight with the Australian dollar slipping below the 65 cent level again as calls for the RBA to cut again grow louder.

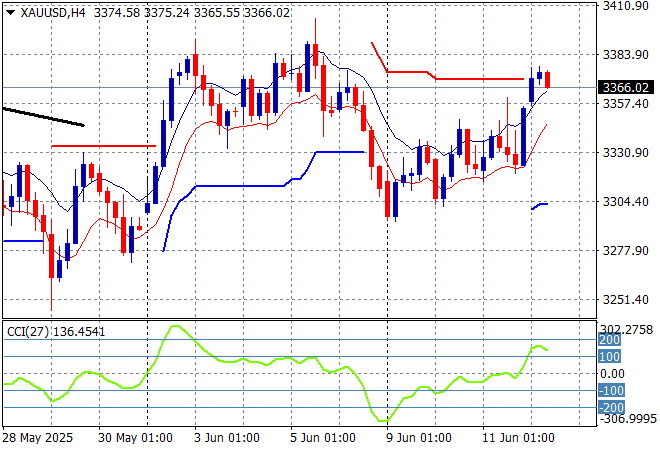

Oil markets are consolidating into recent strength with Brent crude slipping slightly below the $70USD per barrel level while gold has held on to most of its overnight gains to just below the $3370USD per ounce level:

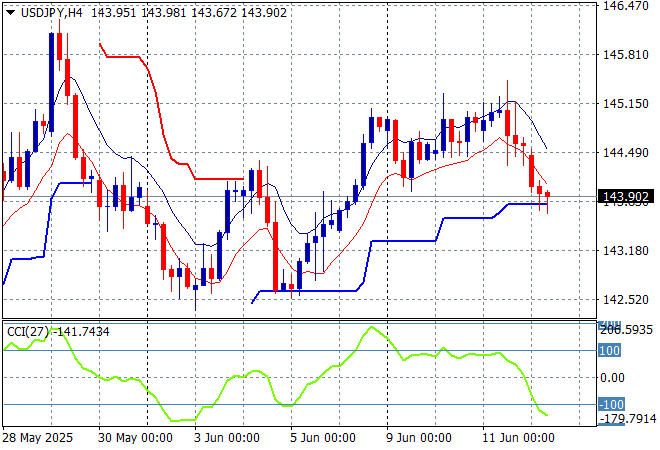

Mainland Chinese share markets are getting of their recent holding pattern as the Shanghai Composite holds above the 3400 point level while the Hang Seng Index has taken back its previous gains to be down nearly 1% in afternoon trade at 24137 points. Japanese stock markets are failing to continue their bounce back with the Nikkei 225 moving 0.6% lower to 38181 points while trading in the USDPY pair has seen a further decline with a drop below the 144 level:

Australian stocks were the best relative performers with the ASX200 closing some 0.3% lower at 8565 points while the Australian dollar has just pushed below the 65 handle:

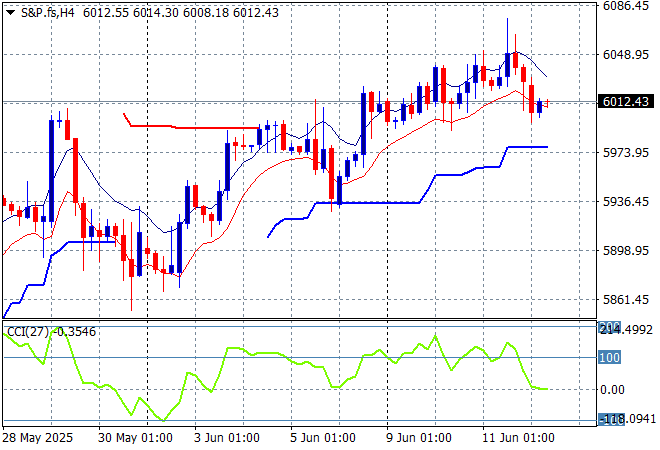

S&P and Eurostoxx futures are down 0.8% or so with the S&P500 four hourly chart still showing a desire to push above the recent highs at the 6000 point level but short term momentum has moved completely out of overbought mode:

The economic calendar will be dominated by US weekly initial jobless claims then the latest PPI figures.