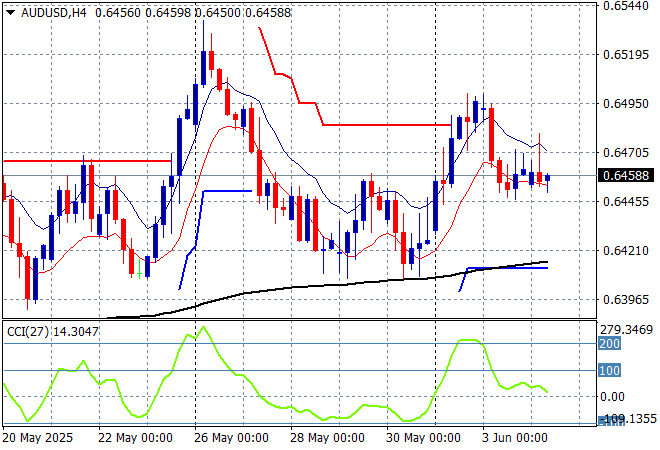

Its still all about the art of the deal as the Trump regime struggles to find anyone wanting to come to the table with more tit for tat accusations between China still not yet upsetting risk markets. Currencies are in a holding pattern, digesting a lot of macro events and geopolitics with tonight’s Canadian central bank meeting in focus alongside a possibly Iranian nuclear deal. Meanwhile the Australian dollar absorbed the latest poor GDP print locally without much effort, still holding at the mid 64 cent level.

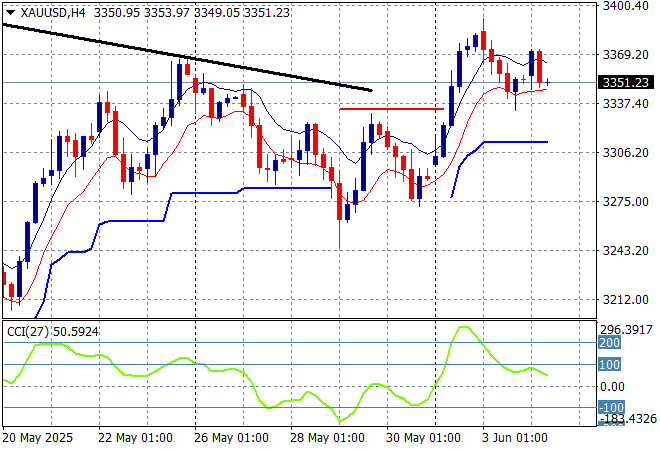

Oil markets are still consolidating into short term strength despite the announced OPEC production increases with Brent crude holding above the $65USD per barrel level while gold has recovered from its minor contraction after getting ahead of itself in the Friday session, holding just below the $3360USD per ounce level:

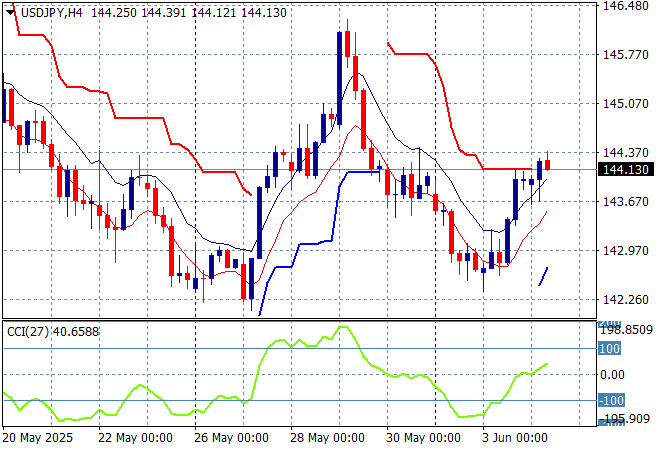

Mainland Chinese share markets continue to have solid gains with the Shanghai Composite lifting 0.4% while the Hang Seng Index has put only nearly 0.6% to build above the 23000 point level. Japanese stock markets were the strongest in the region on the weaker Yen with the Nikkei 225 moving nearly 1% higher to 37806 points while trading in the USDPY pair has seen a further lift above the 144 level but not yet in a strong position:

Australian stocks were able to put on some very strong gains despite the slowing GDP print with the ASX200 closing 0.9% higher at 8541 points while the Australian dollar was somewhat steady throughout the session, still holding above the mid 64 cent level:

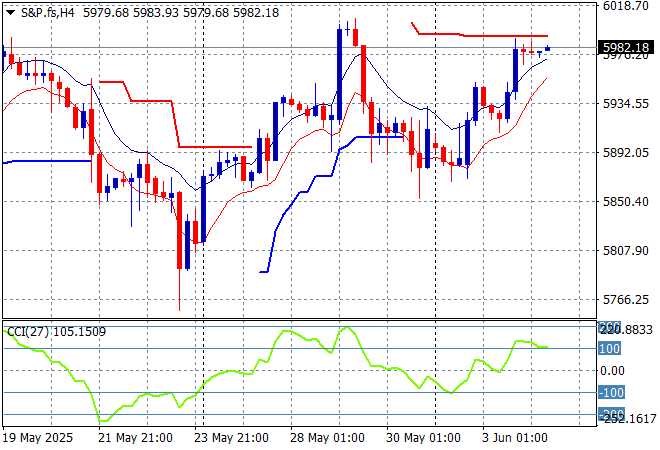

S&P and Eurostoxx futures are down slightly with the S&P500 four hourly chart showing a desire to return to the recent highs near the 6000 point level as short term momentum gets into overbought mode but price action indicating exhaustion setting in:

The economic calendar includes the latest Canada central bank meeting and the US ISM services print.