A lot of macro events and geopolitics hit risk markets today but was mostly absorbed outside of currencies as the USD hit a six week low on a combination of the burgeoning world wide trade war started by the Trump regime and the growing slowdown in the domestic US economy. The latest Chinese manufacturing figures haven’t hurt the local markets as they return from a long weekend, while the Australian dollar took a small hit on the release of the latest RBA minutes where larger cuts look to be off the table for now.

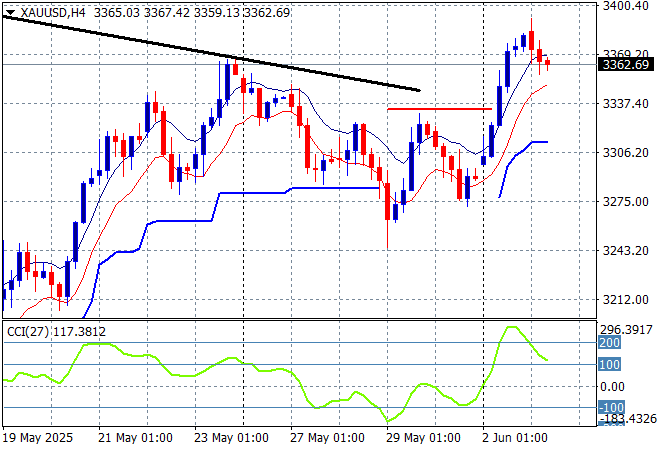

Oil markets are consolidating into short term strength despite the announced OPEC production increases with Brent crude holding above the $64USD per barrel level while gold is having a minor contraction after getting ahead of itself in the Friday session, retreating back to the $3360USD per ounce level:

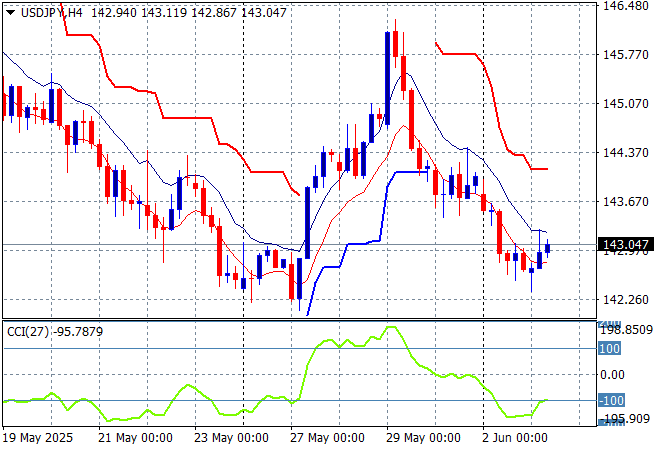

Mainland Chinese share markets returned from their long weekend with the Shanghai Composite lifting 0.4% while the Hang Seng Index has jumped some 1.3% to get back above the 23000 point level. Japanese stock markets were on the backfoot due to BOJ talk with the Nikkei 225 barely up 0.2% to 37510 points while trading in the USDPY pair has seen a slight lift back above the 143 level but still in a very weak position:

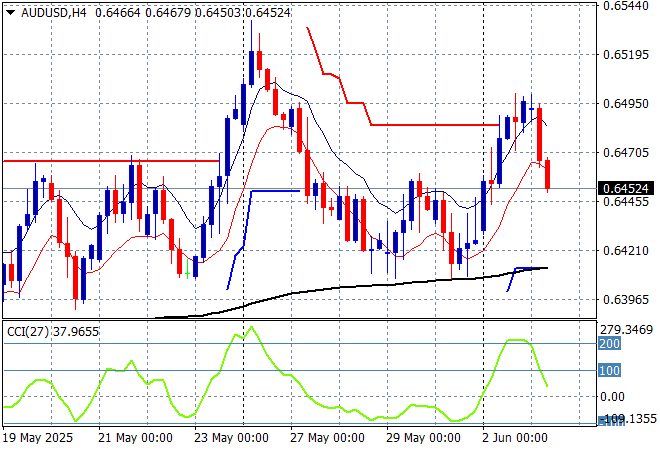

Australian stocks were able to put on some steady gains against the RBA minutes backdrop with the ASX200 closing 0.6% higher at 8466 points while the Australian dollar has been swatted from its near breach of the 65 handle back down to the mid 64 cent level:

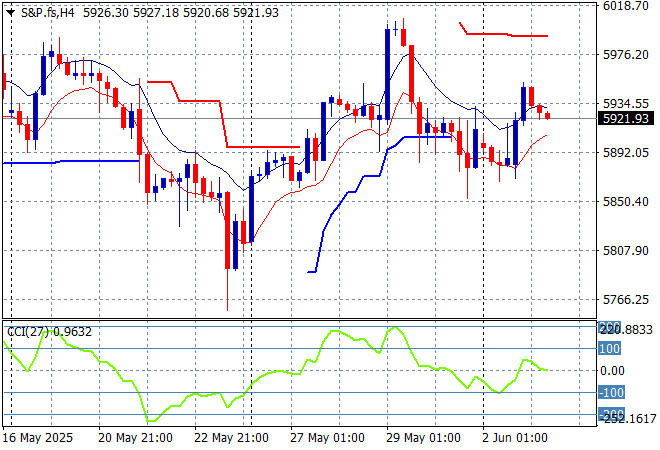

S&P and Eurostoxx futures are up a little as the latter plays some catchup from the firm rebound on Wall Street overnight, however the S&P500 four hourly chart still shows an in ability to return to the recent highs near the 6000 point level as short term momentum and price action point to a bearish head and shoulders setup:

The economic calendar starts with European core inflation figures then switches to the latest US factory orders.