DXY and EUR both look like they are consolidating for more.

AUD at bottom of rising channel.

Brent will crash Monday after OPEC lifted output again. The child president is making everyone except the US “drill, baby, drill”.

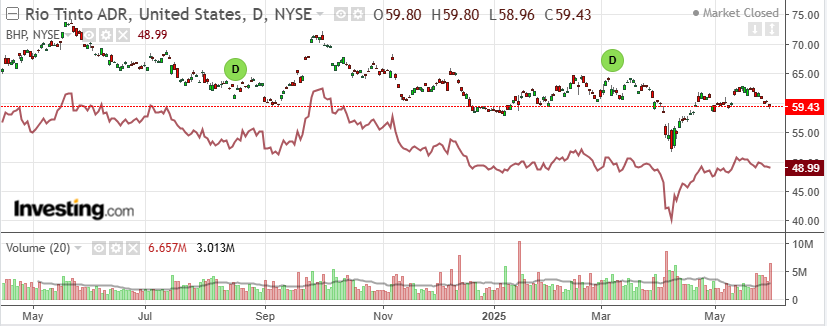

Metals no bueno.

Miners yuk.

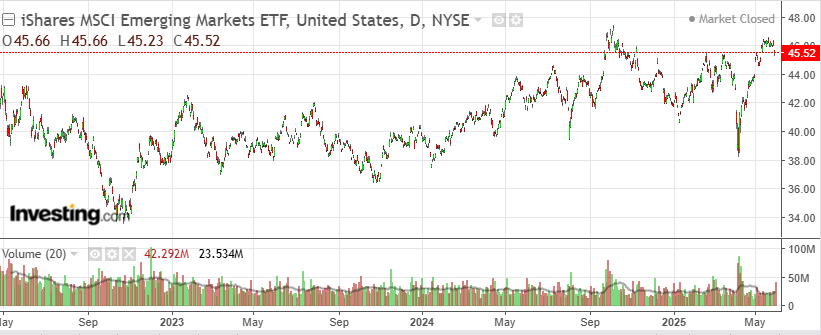

EM meh.

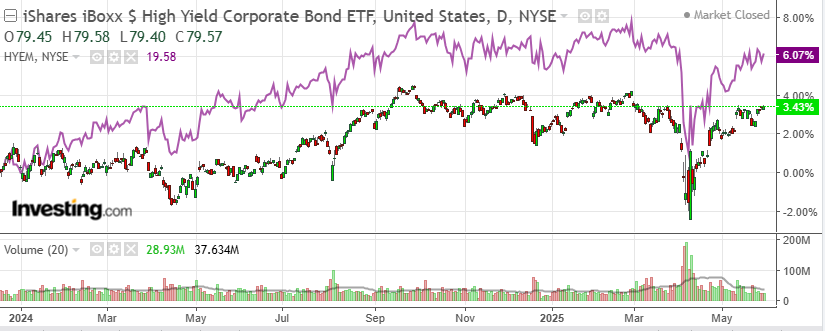

Junk all good.

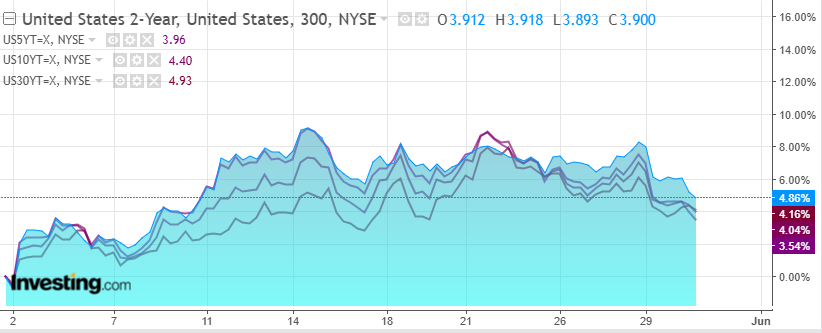

Yields helping.

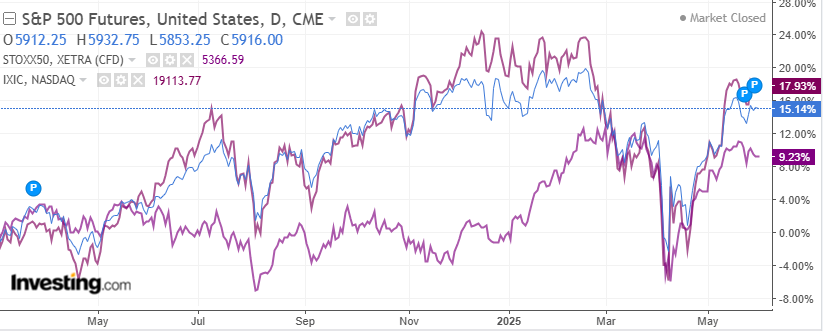

Stocks on hold.

Is the Australian dollar still going to 50 cents? No. This thesis was at least half based on the persistence of US exceptionalism, which is clearly diminished, if not entirely extinguished.

How shrunken is it? BofA sasy we’re about to find out.

We must acknowledge the positives. The US economy seems to have a dynamism that has allowed it to keep surprising upward despite many shocks in recent years.

Market discipline seems to be working this year, keeping US policy implementation away from initial extreme announcements, including on trade policy.

DOGE and plans for substantial spending cuts are out. Tax cuts can support long-term growth.

However, we believe the negatives dominate. Policy uncertainty on multiple fronts remains.

Companies may pause hiring and investment plans until the is greater clarity. In most scenarios, we see tariffs much higher than the starting point, with current levels being the minimum.

The market is reacting negatively to further fiscal policy loosening from already historically high deficits, leading to higher borrowing costs.

The Fed is stuck because of rising inflation expectations, unable to step in pro-actively,until the economy weakens enough to address credibility concerns.

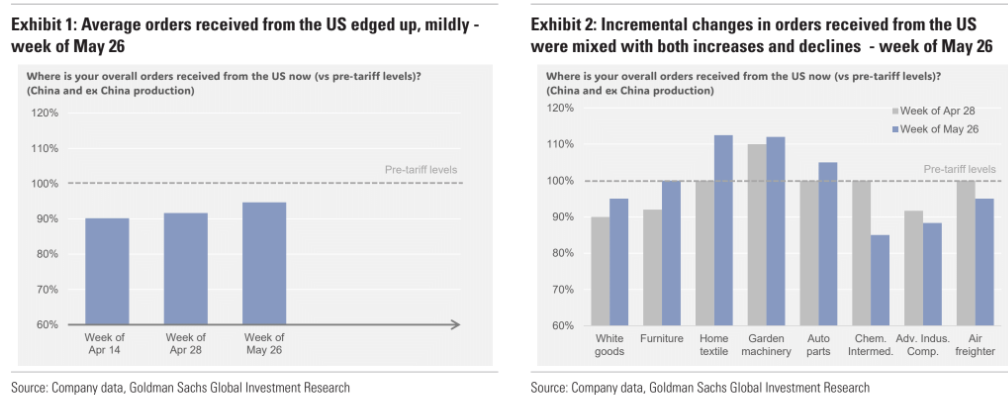

Migration flows have collapsed. Demand increased in Q1 ahead of tariffs but maybe about to fall.

The rebound in trade has also been modest since the break out of tariff peace.

I tend to agree that we have not yet seen the economic impact of the child president and when it comes DXY aught to breakdown as the Fed comes back into the picture.

We did get to 0.59 cents but AUD is now a rising bet, though held back by China, and 50 cents has gone the way of all flesh.