The Reserve Bank of Australia’s (RBA) 25 bp rate cut last month had an immediate effect on the housing market.

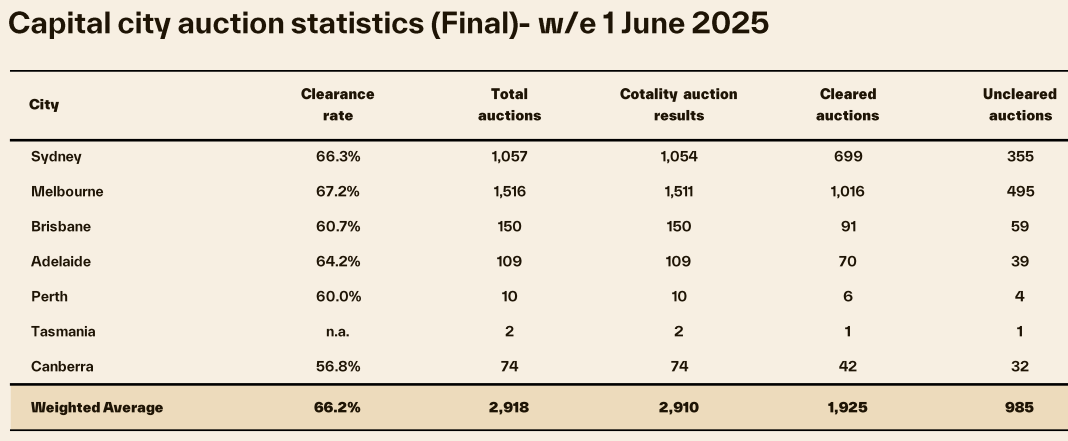

The final auction clearance rate across the combined capital cities soared to its highest level since early July 2024, despite the second-highest auction volumes (2,918) of the year.

Source: Cotality

According to Cotality, 66.2% of auctions resulted in a sale across the combined capital cities, led by Melbourne (67.2%) and Sydney (66.3%).

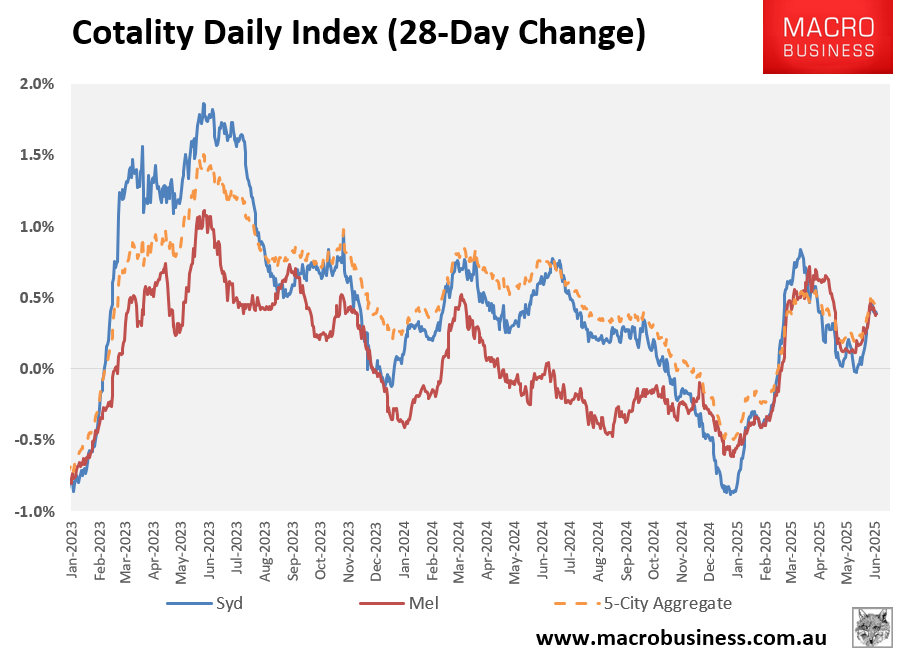

Cotality’s daily dwelling values index has also bounced; albeit growth remains modest:

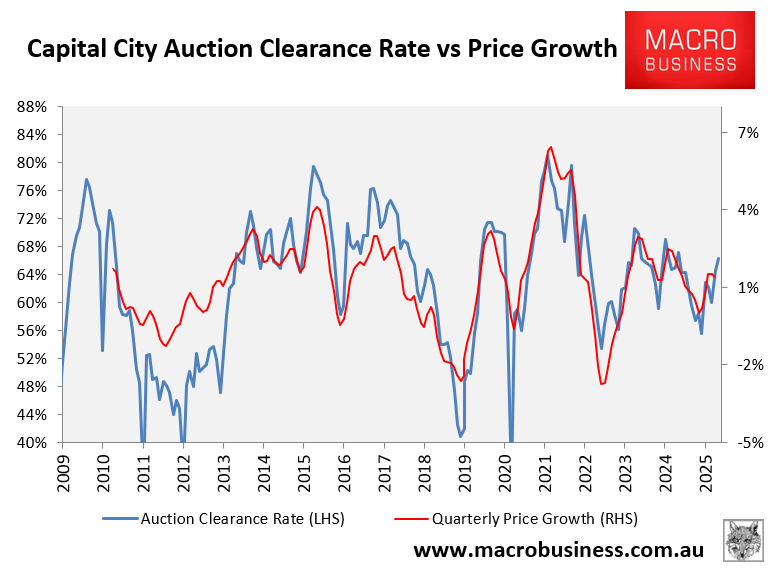

However, given the strong historical relationship between auction clearance rates and prices, illustrated below, value growth should soon rise:

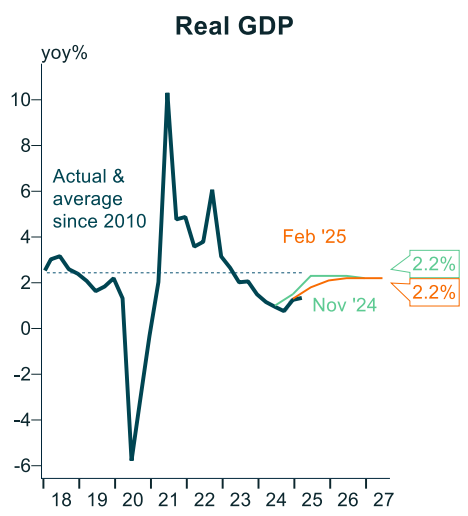

Wednesday’s Q1 national accounts data was unambiguously soft, with real GDP growth printing at only 0.2% for the quarter (-0.2% in per capita terms), which was well below the Reserve Bank of Australia’s (RBA) forecast of 0.45% growth:

Source: Alex Joiner (IFM Investors)

As a result, the probability of the RBA cutting interest rates has increased, with financial markets assigning a 90% probability to a 25 bp July rate cut and tipping another two 25 bp rate cuts this year.

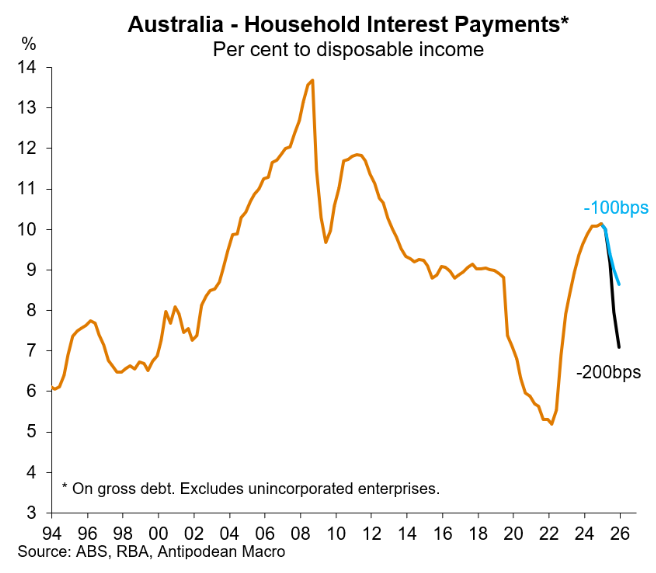

Justin Fabo from Antipodean Macro estimated that a 100 bp reduction in interest rates would reduce the average interest paid on mortgages by around 1.5% of disposable income.

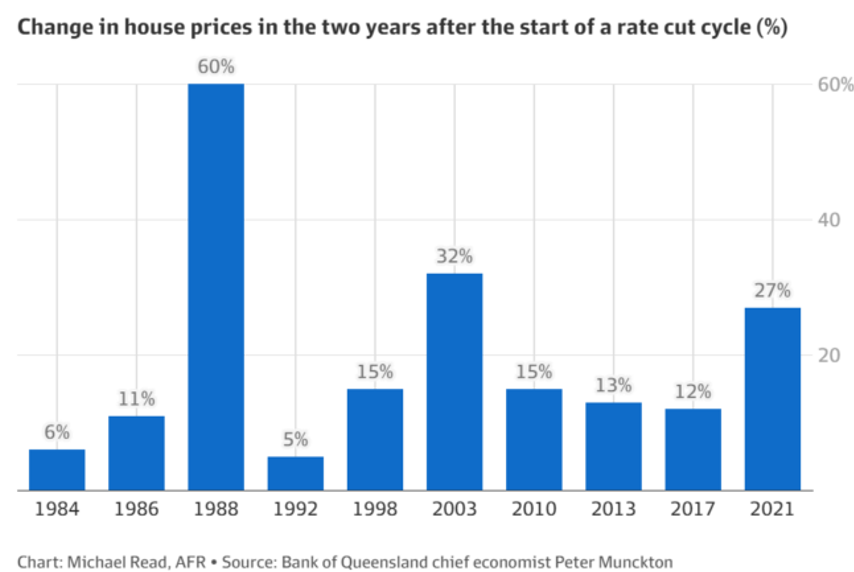

The following chart from The AFR also shows that house prices generally record double-digit growth following a rate-cutting cycle:

The Albanese government’s 5% deposit scheme for first home buyers will also take effect from 1 January 2026, which will further inflate demand and prices.

Interest rate cuts and Labor’s 5% deposit scheme will ignite another upswing in Australian home prices.

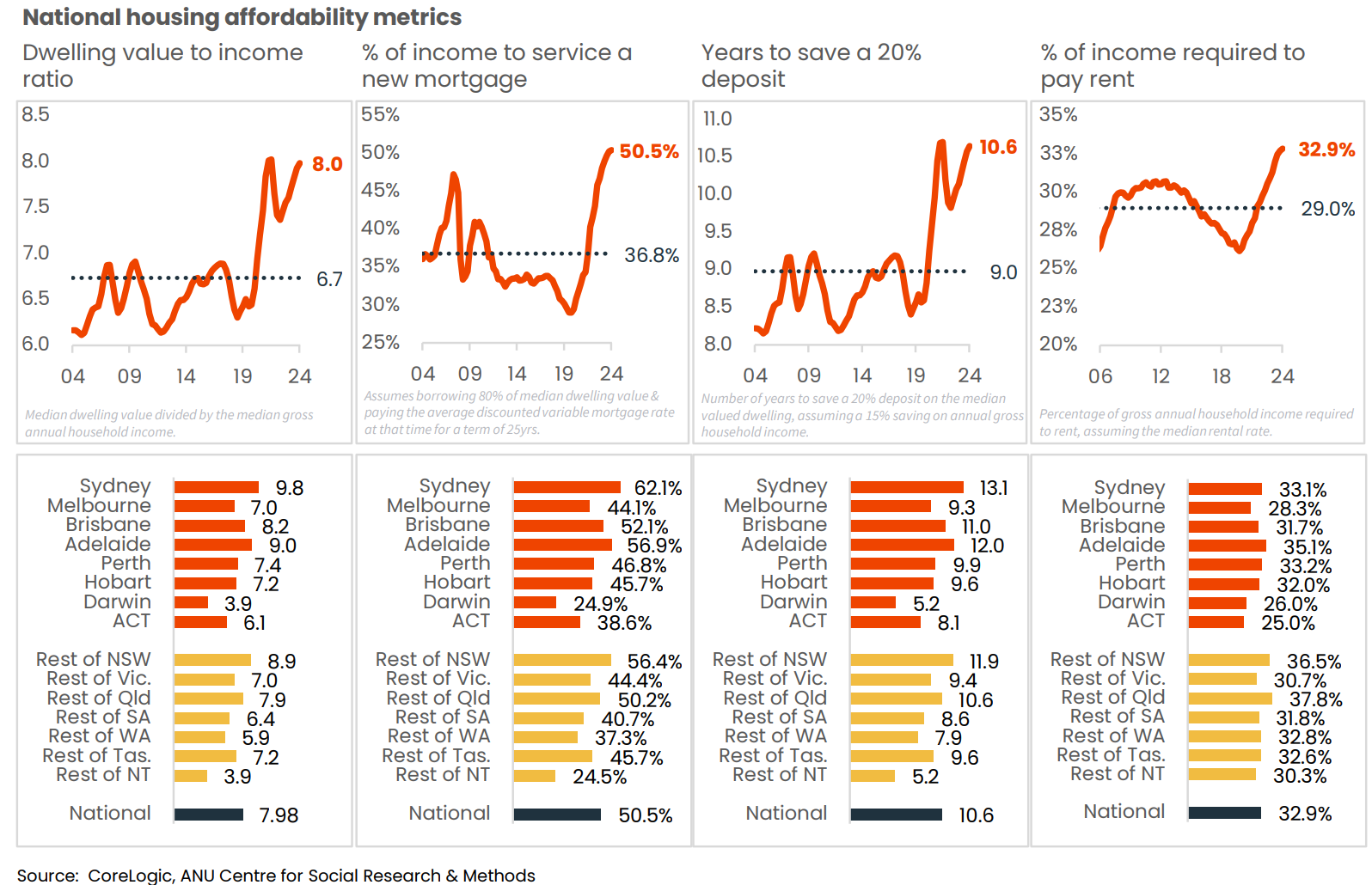

Australian housing is already unaffordable on every metric.

As a father with two teenage children, I would rather not see housing become more expensive.

Adding more mortgage fuel to the housing bonfire is the last thing Australia needs.