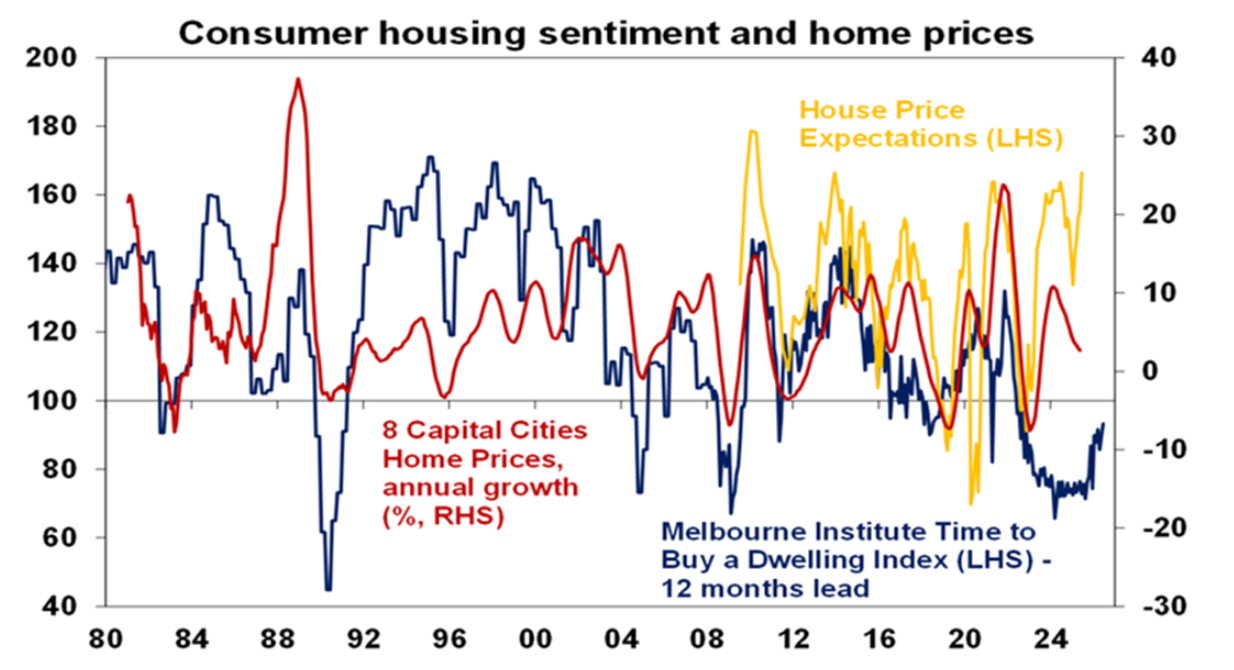

Westpac’s latest consumer sentiment survey suggested that Australians have turned bullish on housing.

As illustrated below by AMP chief economist Shane Oliver, house price expectations hit a cyclical high in May. The “time to buy a dwelling” sub-index has also bounced:

Source: Shane Oliver (AMP)

The rebound in sentiment and house price expectations is understandable given that the Reserve Bank of Australia (RBA) has delivered two 25 bp rate cuts this year.

Financial markets and most economists also expect the RBA to deliver another three 25 bp cuts by the end of the year, which would lower the official cash rate to 3.10%.

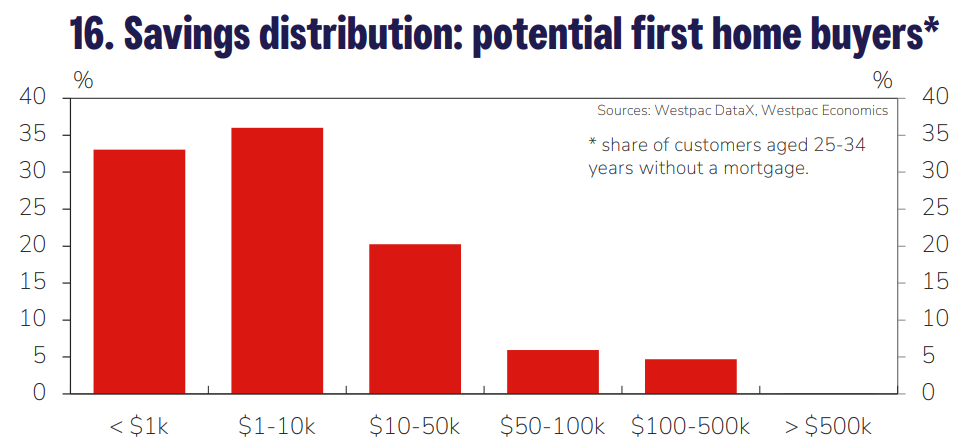

During the recent federal election campaign, the Albanese government announced that from 1 January 2026, all first home buyers would be able to purchase a home with only a 5% deposit without requiring lenders’ mortgage insurance.

This would be achieved by the government (read taxpayers) guaranteeing 15% of all first home buyer mortgages.

Analysis from Westpac’s latest Housing Pulse showed that almost one in six young Australians have enough money saved to purchase a property under Labor’s 5% deposit scheme.

“With the median Australian dwelling price sitting at just over $825k, a 5% deposit under the FHG scheme would require at least $41k”, Westpac’s Matthew Hassan said.

“Based on our Panel data, just over 15% of 25-34 year olds without a mortgage have savings that meet this criteria. Without the scheme, just 4% of this pool would have enough savings for a 20% deposit on a median home purchase”.

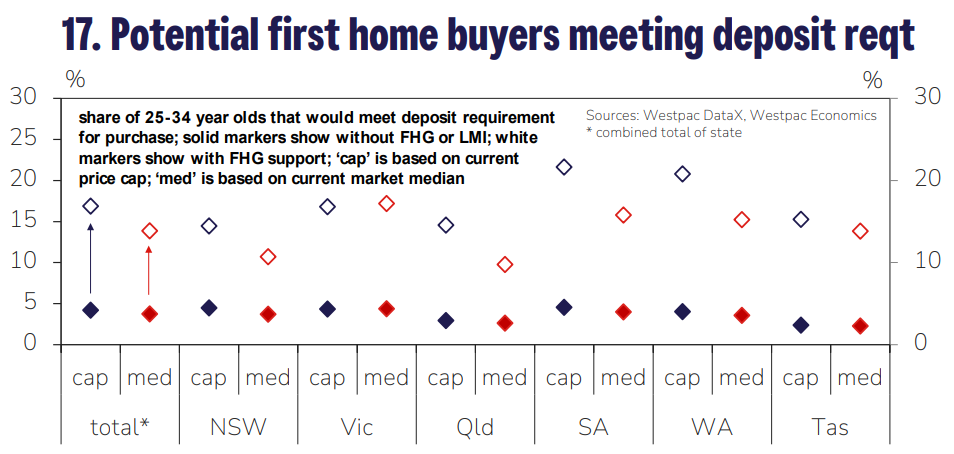

“By state, we find that around 22% of local buyers would have enough savings to purchase in SA, 21% in WA, 17% in Vic, 15% in Qld and Tas, and 14% in NSW”, Hassan estimated.

Hassan estimates that the implied pool of prospective first home buyers qualifying under the new 5% scheme is in the order of 400,000 nationally.

However, first home buyers will also need to have sufficient income to meet lenders’ loan seviceability tests, which will reduce the pool of potential buyers.

“Notably, the FHG scheme means these tests are applied to a larger loan (95% of the purchase price rather than 80%)”, noted Hassan.

Irrespective, falling mortgage rates combined with Labor’s 5% deposit scheme will add significant stimulus to house prices this year and next.