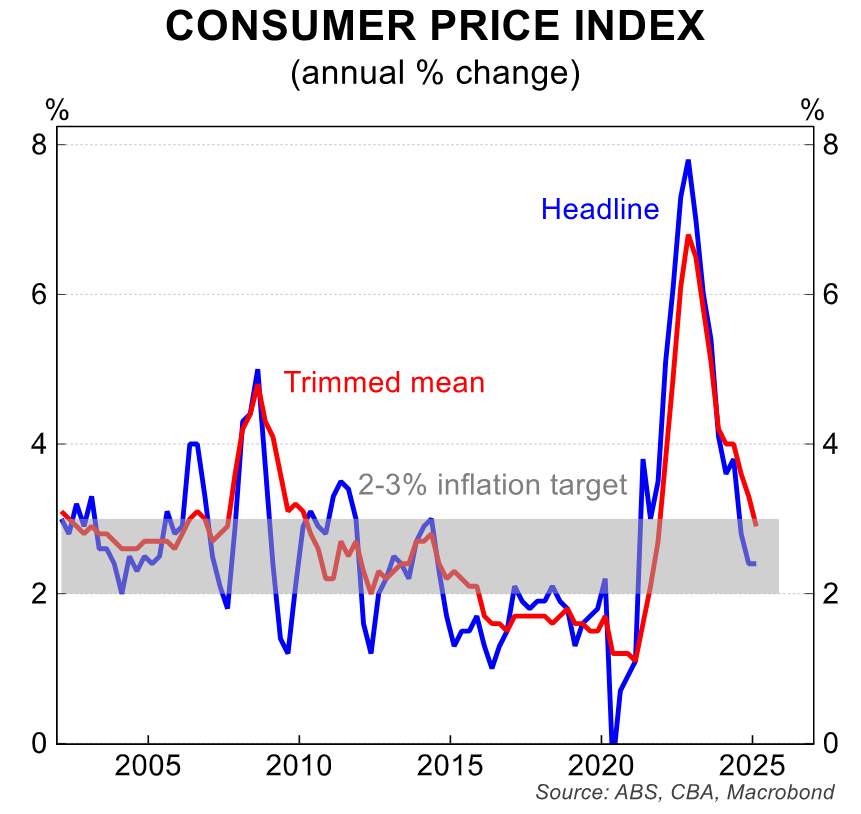

The official Q1 CPI inflation print from the Australian Bureau of Statistics (ABS) showed that the policy-important trimmed mean inflation rate declined to 2.9% year-on-year, within the Reserve Bank of Australia’s (RBA) inflation target of 2% to 3%.

RBA Governor Michele Bullock’s media appearance following last month’s 0.25% rate cut suggested that she was less concerned about inflation than a slowdown in the global economy.

Bullock’s dovish commentary took market participants by surprise, with Jamieson Coote’s portfolio manager, James Wilson, claiming that it “sounded like a victory lap in the fight against inflation”.

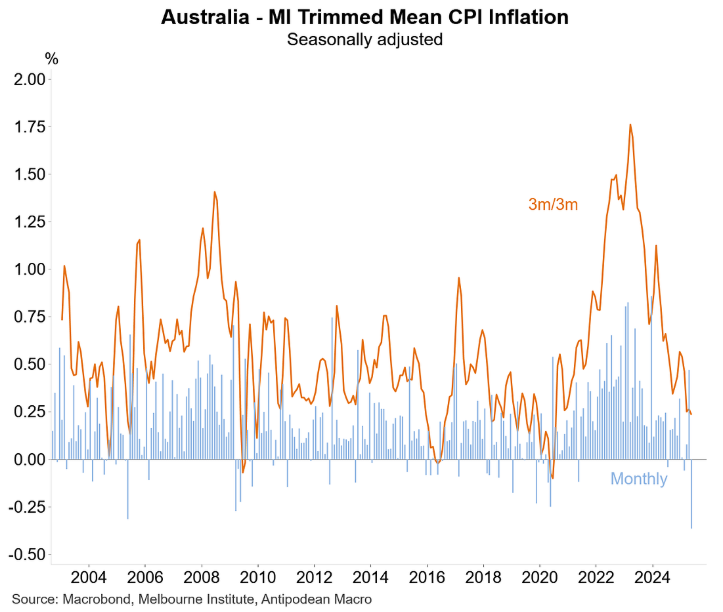

The RBA would be heartened by May’s inflation gauge from the Melbourne Institute (MI), which supported the view that underlying inflation is easing.

The MI trimmed mean inflation gauge pulled back sharply in May after a bounce in April. As illustrated below by Justin Fabo from Antipodean Macro, the measure has fallen sharply in quarterly terms:

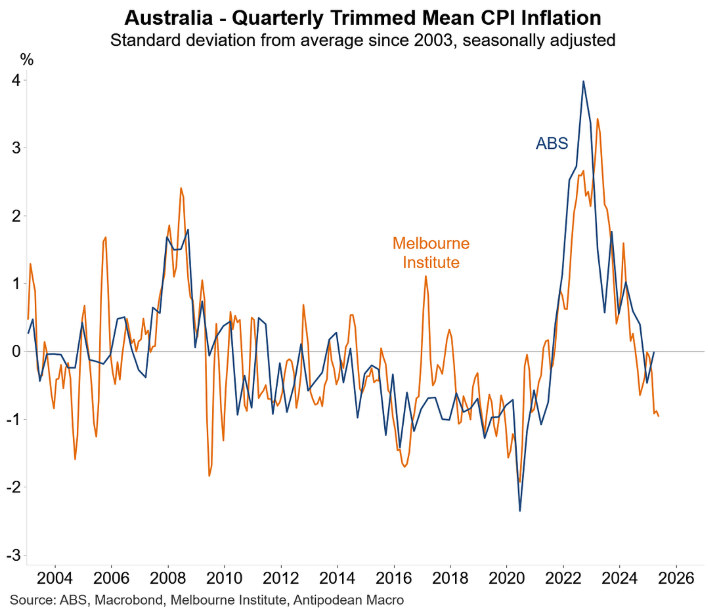

Fabo also shows that MI trimmed mean inflation was tracking well below the long-run average:

Last week’s weak capex and retail sales releases from the ABS, which both reported falls, suggested that Australia’s economy remains in a fragile state, which supports further monetary easing from the RBA.

Indeed, financial markets are tipping another three 0.25% rate cuts in 2025 and an end-of-year cash rate of 3.1%.