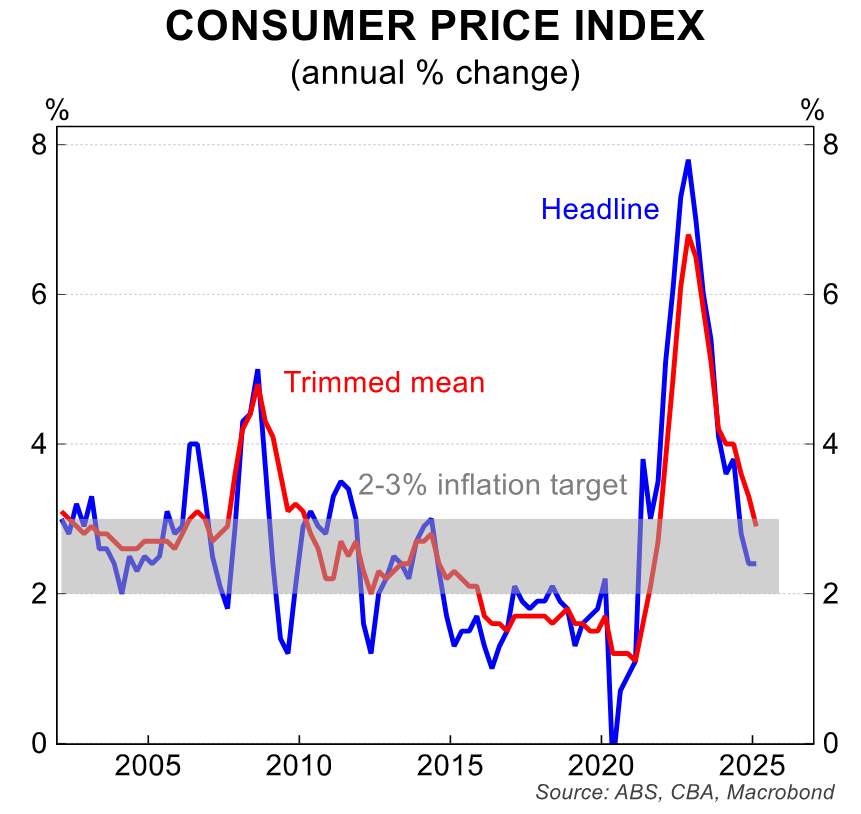

The official Q1 CPI inflation data from the Australian Bureau of Statistics (ABS) revealed that the policy-important trimmed mean inflation rate fell to 2.9% year over year, staying within the Reserve Bank of Australia’s (RBA) inflation target range of 2% to 3%.

RBA Governor Michele Bullock’s media appearance following last month’s 0.25% rate cut suggested that she was more worried about a slowing global economy than inflation.

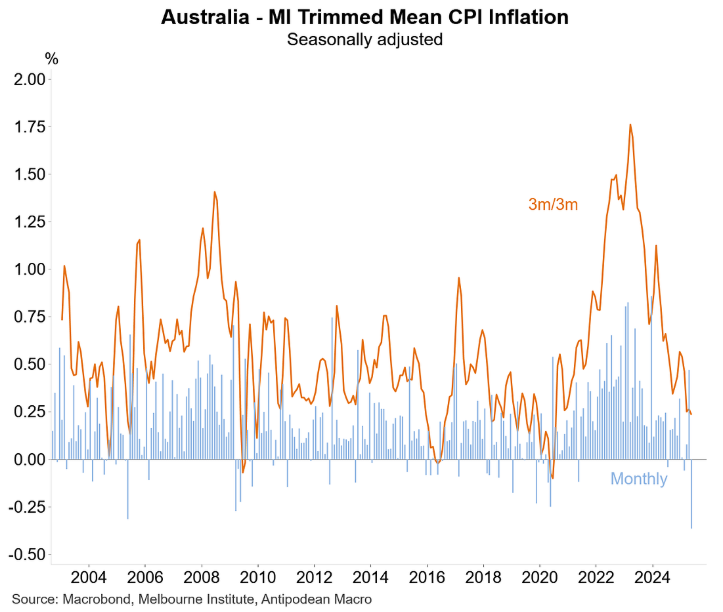

The Melbourne Institute’s (MI) inflation gauge for May supported the view that the rate of inflation is falling.

The MI trimmed mean inflation gauge fell substantially in May following a rebound in April. As shown below by Justin Fabo of Antipodean Macro, this measure has declined sharply in quarterly terms:

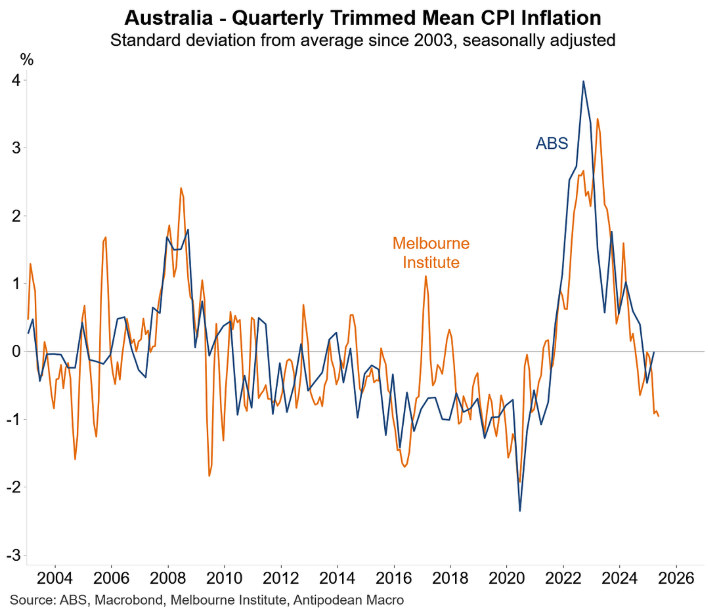

Fabo also showed that MI-trimmed mean inflation was running well below the long-run average:

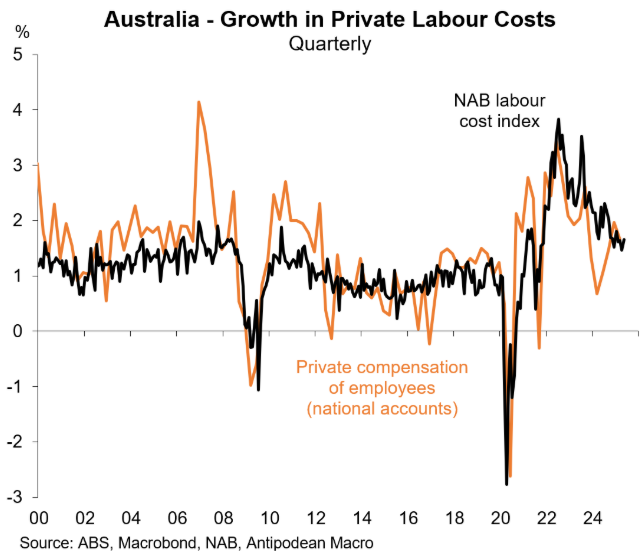

Tuesday’s NAB business survey offered more good news on the inflation front. As illustrated below by Fabo, firms reported softer labour costs:

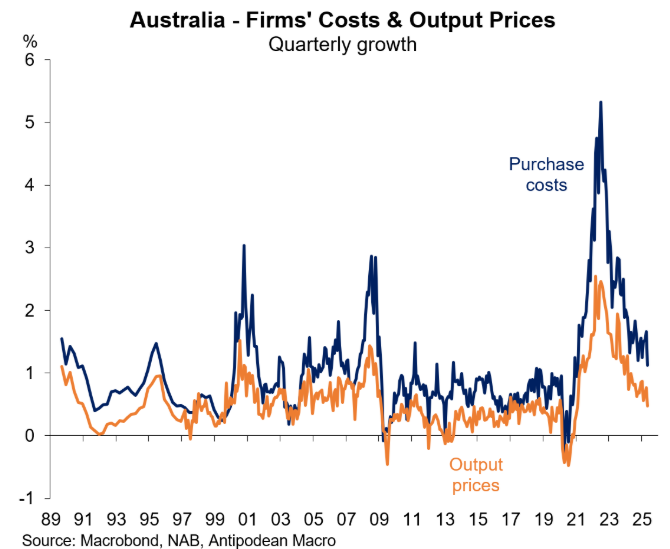

Most importantly, firms’ output costs and prices have plummeted:

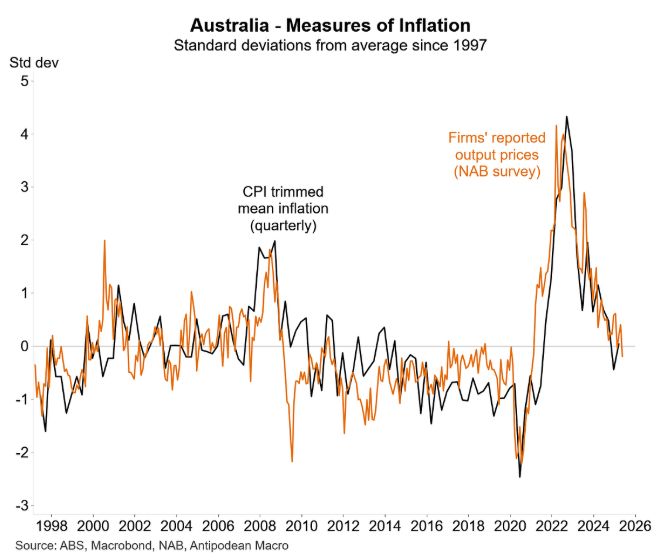

And firms’ reported output prices typically track ABS trimmed mean inflation closely:

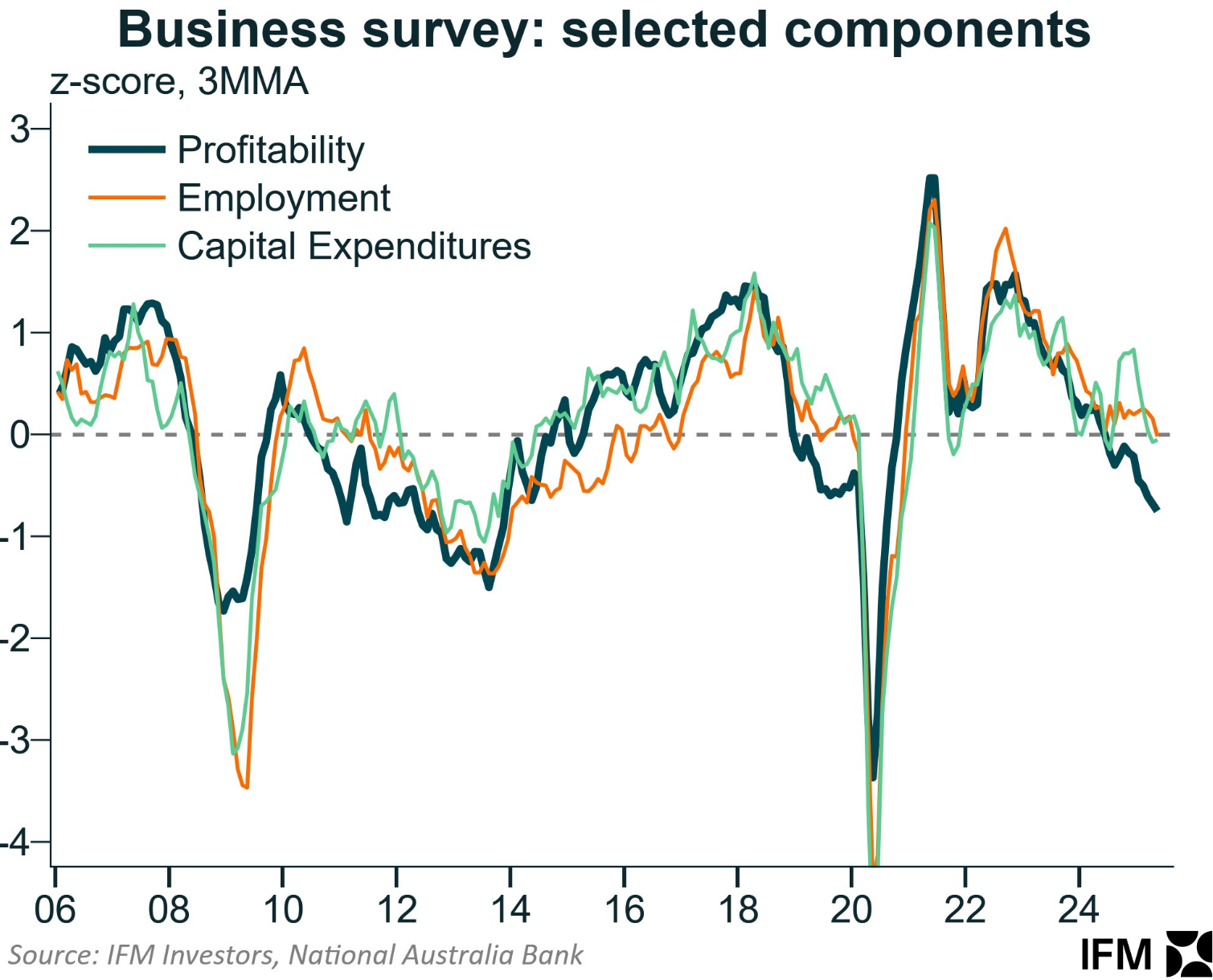

The NAB business survey and the latest retail trade and capex figures from the ABS depict a deteriorating consumer and business economy, characterised by sluggish demand, declining investment intentions, and declining profitability.

As a result, the RBA is near certain to cut rates at next month’s monetary policy meeting. The question is by how much? Will it opt for an oversized 35 bp cut to bring the cash rate into its standard 25 bp increments?

As of close of business Tuesday, financial markets were still tipping three 25 bp rate cuts this year with an end-of-year cash rate of 3.10%:

While further rate cuts are justified given the soggy state of the economy, they will also put a rocket under home prices.

Such is the Australian economy.