DXY fell Friday, but WWIII should be enough to restore it this morning.

AUD is bunkering.

We’ll see a nice oil pop this morning. I say short it. MAGA ain’t pleased.

Metals grind on.

The mining bear market is huge and only just begun.

EM meh.

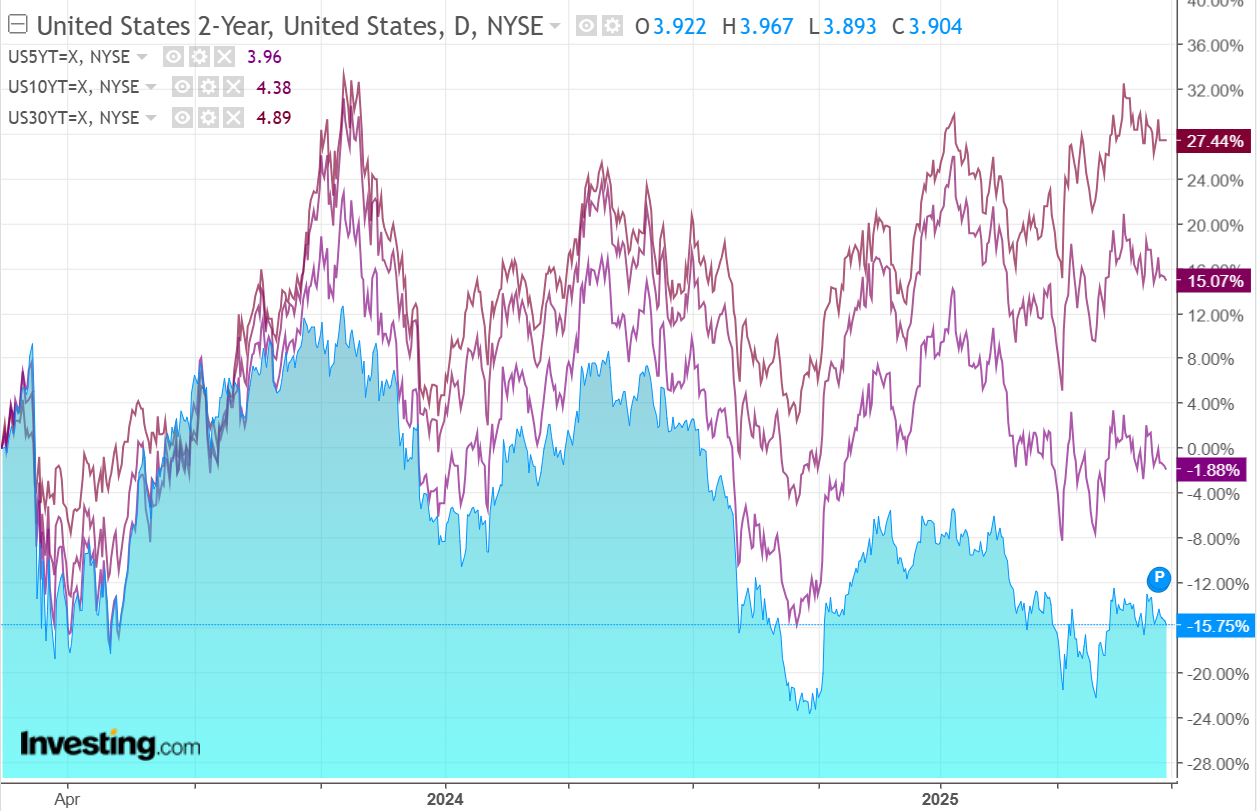

A safe haven bod for Treasuries.

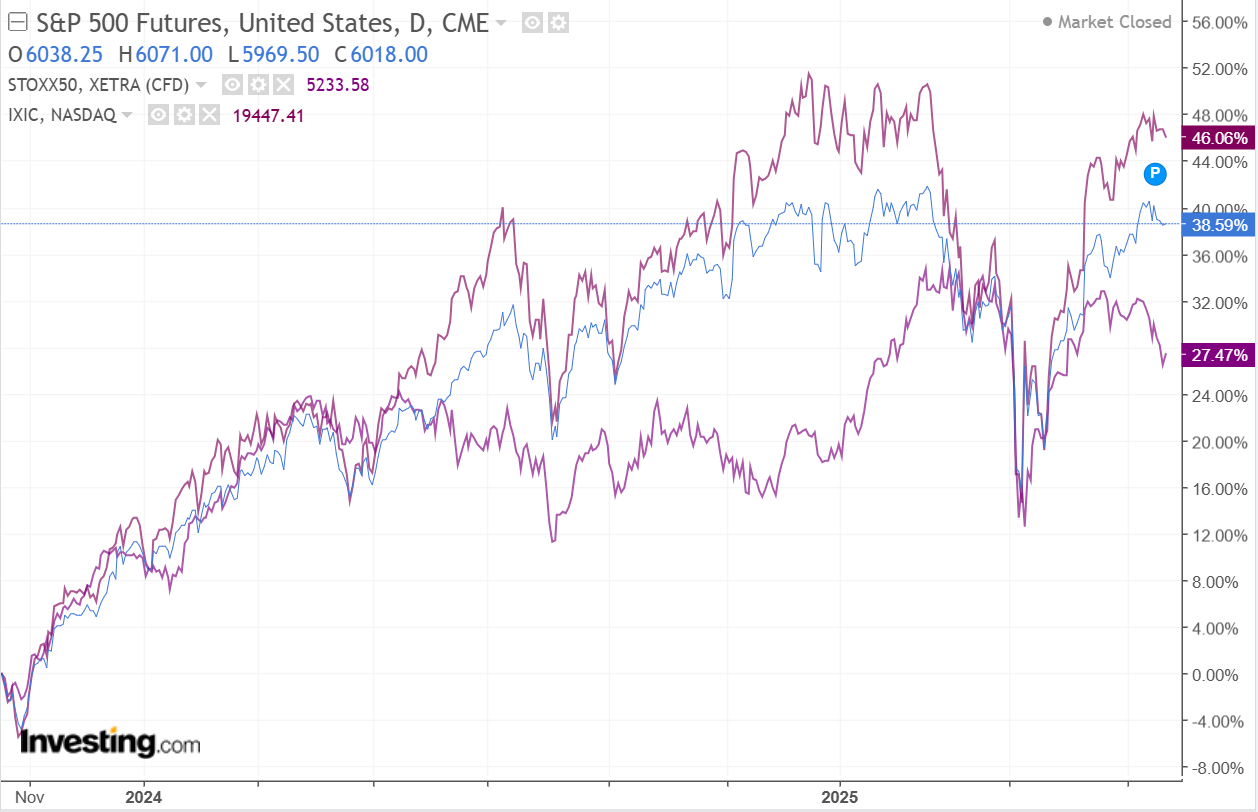

Stocks only go up.

An oil spike is not welcome anywhere, but it is less bad in some places than others, and relativity is the FX game.

The US oil patch will get relief after a difficult period. Whereas Europe will get the opposite. Morgan Stanley.

Euro area headline inflation surprised on the upside in August.

The main reason was a significant rebound of energy prices (3.2%M) triggered by a strong and rapid pass through from higher oil prices to retail fuel prices.

Over the past months, falling energy inflation has contributed to 85% of the fall of headline inflation from its peak at 10.6%Y in October 2022 to 5.3%Y inAugust.

So, oil prices edging up again raises concerns about 1) the impact this could have on the prevailing investor thesis of rapid disinflation over the next months and 2) the effect of higher oil prices on the macroeconomic outlook.

…we think that consumption is likely to pick up on the back of accelerating real income.

A sharp and persistent increase in oil prices would markedly change this view and we would probably have to downgrade our forecast for 2024, a weak 0.7%Y already, by around 30bp if Brent prices were to be 30 dollars higher than we currently think.

I do not expect the war to last. It is too damaging in the US as well, both politically and economically.

But while it does, AUD goes down with EUR.