Australia is a housing bubble with an economy attached

The Australian Bureau of Statistics (ABS) released data on Australia’s housing stock, which was valued at a record $11,366 billion as of Q1 2025, equating to $1,002,500 per dwelling.

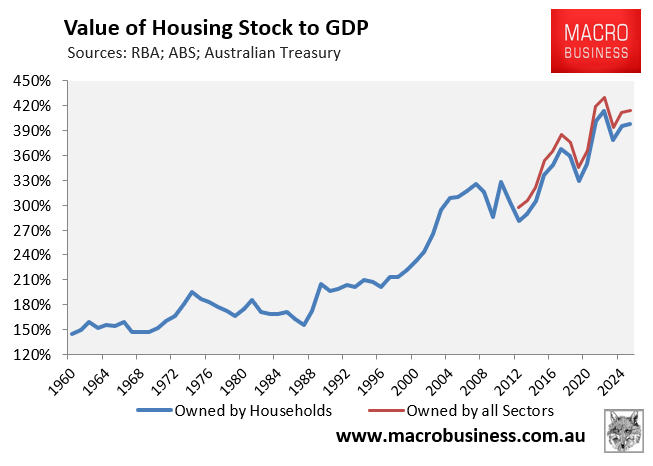

The following chart plots the value of Australia’s dwelling stock against the nation’s GDP and shows that the total stock was worth 4.14 times the size of the Australian economy in Q1 2025:

Australia’s housing stock was valued at $396,400 per person in real terms in Q1 2025, and has more than tripled over the past 30 years:

This hyperinflation of housing values helps to explain why Australian households are considered to be among the wealthiest people in the world, even though higher home values are useless to owner-occupier households who merely need somewhere to live.

The following chart from Alex Joiner at IFM Investors plots the value of Australia’s housing stock relative to the United States, which is valued at only 1.6 times GDP.

“The ABS just reported that the value of the Australian housing stock was above $11 trillion, that’s over four times annual GDP compared with the US at 1.6 times”, noted Joiner on Twitter (X).

“An enormous amount of capital devoted to a very low productivity asset. This is a handbrake on our economy”, Joiner said.

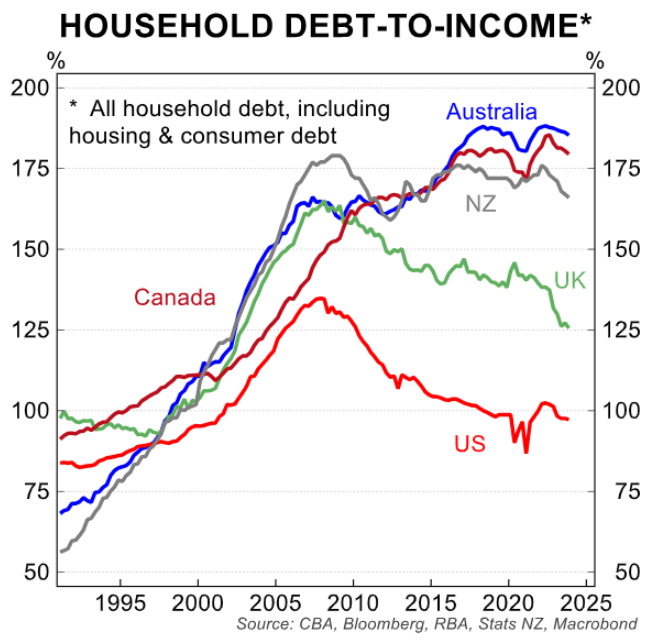

Meanwhile, Australians are drowning in debt, taking out ever-larger mortgages to pay ever-higher home prices.

As a result, Australian households carry some of the world’s highest debt loads.

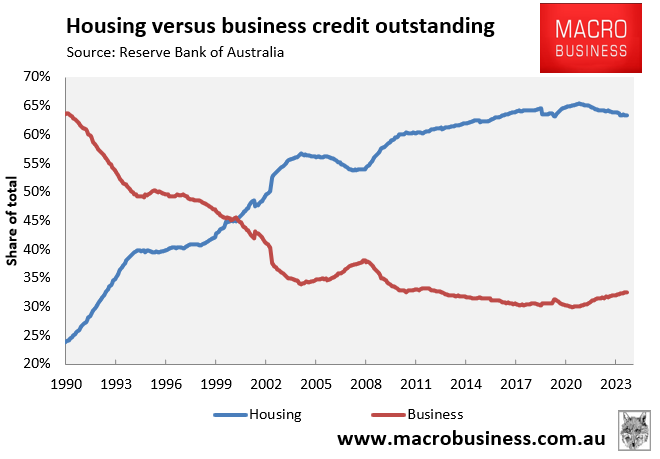

Australia’s banks have grown into enormous building societies that prioritise residential loans over productive businesses.

In 1990, businesses received about two-thirds of all bank loans, with mortgages accounting for only around a quarter.

Thirty-five years later, the ratio has flipped, with more than two-thirds of bank loans for housing and only one-third for businesses.

AustralianSuper CEO Paul Schroder argued at the March AFR Business Summit that the country’s property obsession has diverted capital away from the productive economy.

“All we’ve done is pour all of this money into houses, which has deprived the economy of heaps and heaps of productive capital”, Schroder said.

“We’ve got all this money in domestic houses and we’re not backing business, we’re not creating new things, we’re not driving productivity”…

“I think the big, burning productivity and cost of living problem is housing. I think we keep underestimating how worrying housing is”.

John Kehoe noted similar concerns last week at The AFR:

Five of the 10 most valuable companies on the Australian Securities Exchange are banks: ANZ, CBA, National Australia Bank, Westpac and Macquarie Group, though the last is more of an entrepreneurial global fund manager.

It’s a stark contrast to the American sharemarket, where innovative technology companies take out the top seven positions: Nvidia, Microsoft, Apple, Amazon, Google owner Alphabet, Facebook owner Meta and Broadcom. Productivity is booming in the tech-savvy US…

While healthy banks are a positive, bank profits are earned from lending to a relatively unproductive asset class: residential property. The national obsession with loading up on debt to build wealth from property is likely contributing to stagnant productivity, a lack of business dynamism and failure to produce more world-leading businesses.

Our household debt is the third-highest among rich club Organisation for Economic Co-operation and Development nations, overwhelmingly due to high house prices…

“Our big companies on the ASX lend largely into a non-productive asset class, which is established housing,” [Alex] Joiner says. “If we want to be a highly productive economy, we need companies that can do that”…

It’s not surprising that bank values have soared because the size of the home loans they grant is directly related to property prices…

The high cost of residential property is bad for entrepreneurs in two ways. First, expensive housing makes it harder for people to afford to take time off a regular job to risk starting a new business venture…

Second, Reserve Bank research suggests that high house prices relative to incomes make it harder for young entrepreneurs to access business finance…

Sadly, the Albanese government has committed to allowing all first-time home buyers to purchase a property with only a 5% down payment, with the government (taxpayers) guaranteeing 15% of the borrowers’ loan.

Labor has also stated that mortgage lenders will no longer be required to include student debts in their serviceability assessments.

Labor’s policy, combined with lower interest rates, will further increase household debt and property prices, as well as divert more of the nation’s capital into non-productive housing.

I discussed these issues in last week’s podcast with Martin North from Digital Finance Analytics.