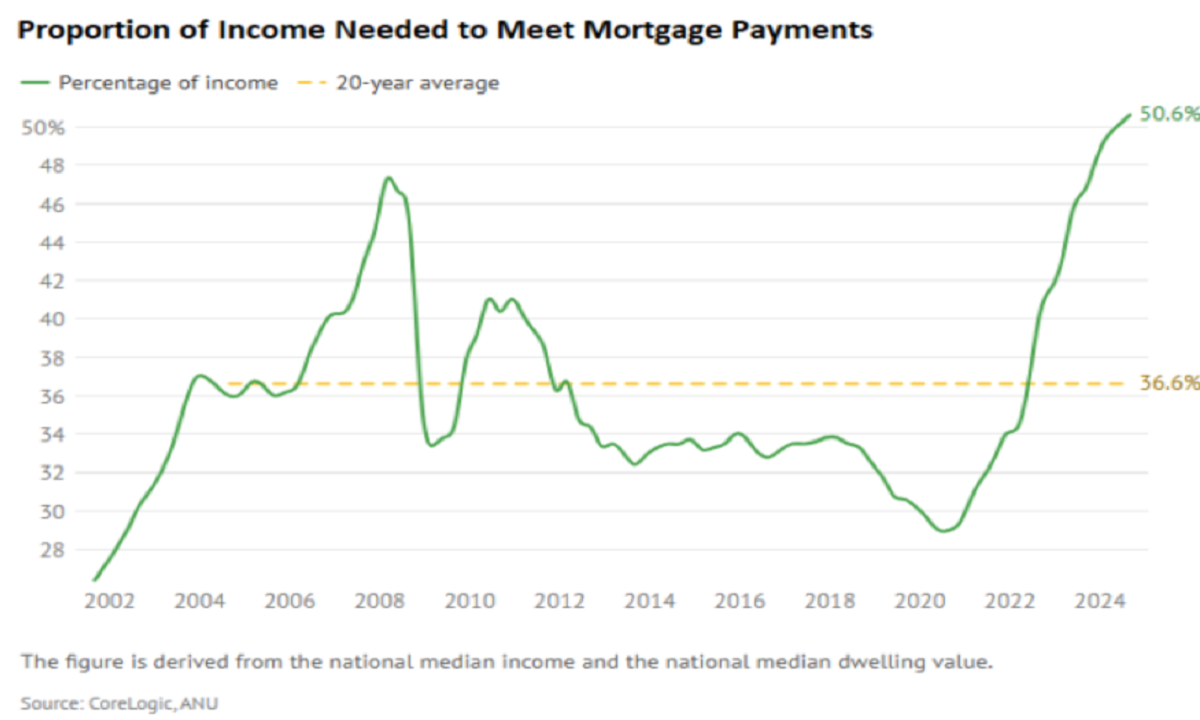

At the end of 2024, Australia’s mortgage affordability was the worst on record, with households required to sacrifice a record share of their incomes to repay the median-sized new mortgage.

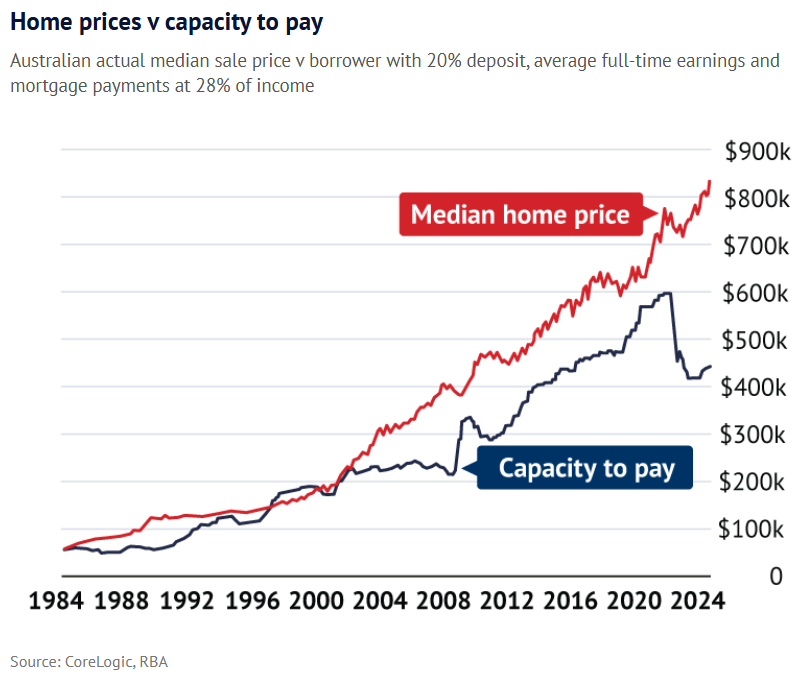

There was also a record gap between the median home price and borrowers’ capacity to pay, assuming traditional affordability metrics.

So far this year, the Reserve Bank of Australia (RBA) has lowered the official cash rate by 0.50% to 3.85%, which should reduce scheduled principal and interest mortgage repayments on the median-priced Australian home by around 5% once passed on to borrowers.

These rate cuts will, therefore, improve the above charts by reducing the proportion of income needed to meet mortgage repayments and reducing the gap between the median home price and capacity to pay.

However, the impacts could be temporary, as the lower interest rates will inevitably be capitalised into larger loan sizes and higher prices.

Indeed, industry insiders are warning that the rate cuts from the RBA will drive a rise in prices, squeezing first-home buyers and driving FOMO (‘fear of missing out’).

Broker Alya Manji from Aussie Home Loans Hurstville told the ABC that there’s roughly “an eight-week window” to buy after a rate cut before it drives up prices.

“If you don’t act within that time, it gets tougher”, she said.

Manji said a 0.25% rate cut could increase borrowing power by $10,000 to $25,000 on a $500,000 loan, driving a corresponding price rise.

“I see buyers feeling such FOMO that they sign on properties they’re not even sure they want. They feel there’s no choice”.

Domain’s chief of research and economics, Nicola Powell, added that lower interest rates combined with chronic housing shortages would drive prices higher.

“A rate cut prompts buyers to act quickly, fearing further price increases. Buyer inquiry volumes are up year-on-year in all of our capital cities”, she said.

REA Group senior economist Eleanor Creagh agreed, citing rising demand amid persistent supply shortages.

“In terms of housing supply, we’ve still got constraints on the delivery of new homes, particularly in major capitals”, she said.

The situation will only intensify next year when the Albanese government’s 5% deposit scheme for all first home buyers comes into effect from 1 January 2026.

This policy will increase borrowing capacity and pull forward demand, further fueling prices.

“We know that if you increase subsidies around housing, it can increase capacity around borrowing and push up those prices”, Meg Elkins, a behavioural economist at RMIT, told the ABC.

In short, rate cuts combined with inflationary policies like Labor’s 5% deposit scheme are about to birth another round of FOMO and housing Hunger Games.