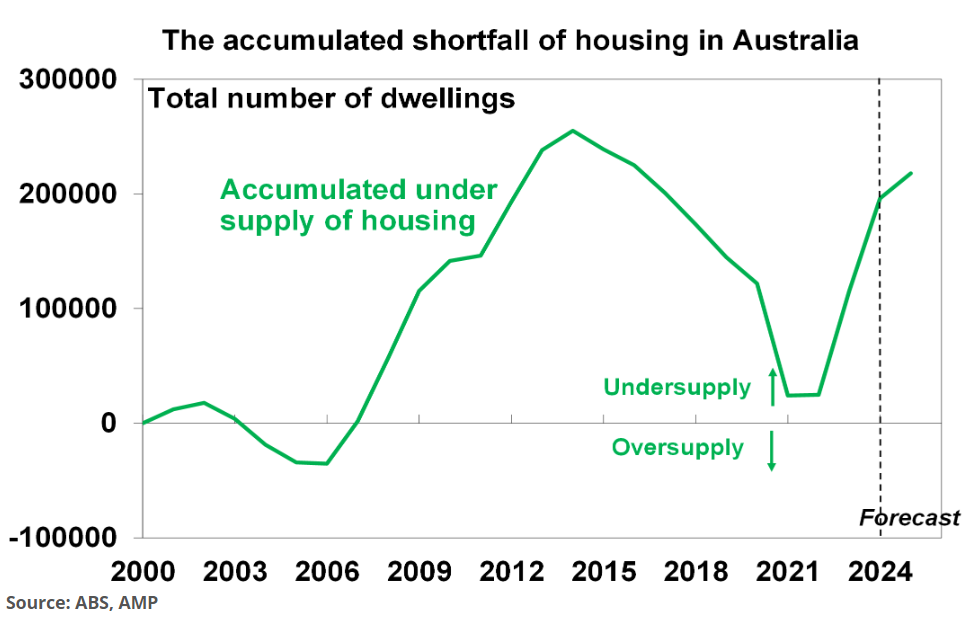

The latest State of the Land Report 2025 from the Urban Development Institute of Australia (UDIA) forecasts that the nation’s housing crisis will worsen as demand from population growth (immigration) continues to outrun housing construction:

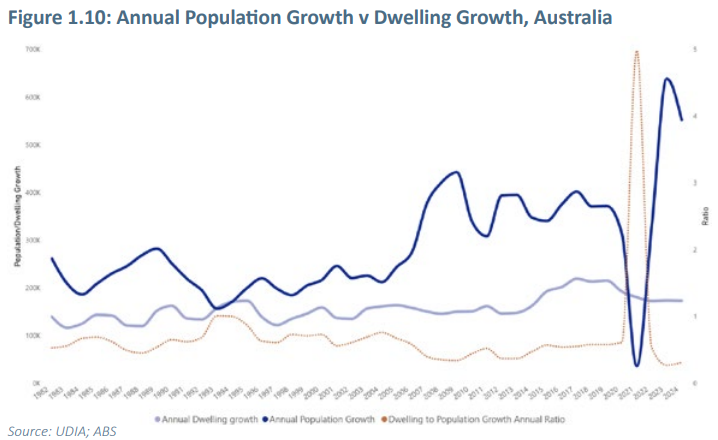

UDIA’s long-run analysis of national population and dwelling growth highlights a serious divergence in new dwelling supply not keeping pace with upward fluctuations in population growth…

The significant uplift of population growth recorded from 2007 and maintained until the commencement of the pandemic in 2020 has now been dwarfed by the extraordinary net population growth of 638,000 recorded in the 2023, followed by 552,000 in 2024.

There were a total of 173,200 dwellings completed in 2024 which equates to a dwelling to population ratio of 0.31, which maintains the lowest level this ratio has ever been, with only the Global Financial Crisis impacted period of 2007 and 2008 recording a ratio anywhere near this level when the ratio reached 0.35.

Underpinned by an upswell in net overseas migration, the dramatic growth in population in the last two years is clearly not being met with a suitable growth trajectory of new dwelling production…

The current trajectory of a significantly elevated population growth-driven demand profile, against a declining supply profile indicates another phase looms of extremely strong housing value growth, very low rental stock availability and broad-based erosion of national housing affordability.

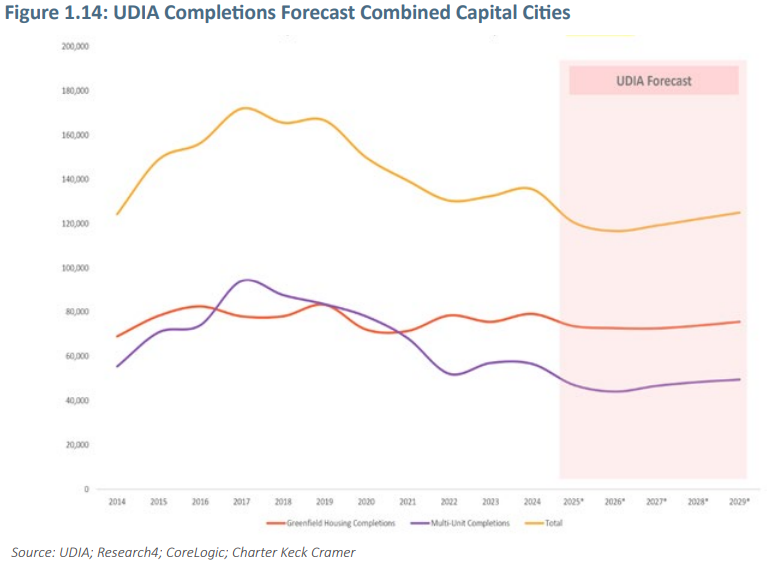

UDIA also forecast that Australia will face a critical shortage of nearly 400,000 homes by 2029:

UDIA modelling indicates there was 135,600 dwellings completed in 2024 in our assessment of combined capital city new residential market supply…

UDIA’s modelling of current and forward pipeline activity indicates there will be a 11% drop in aggregate volumes of combined capital city new residential market supply delivered in 2025 to 120,660 aggregate completions, with multi-unit sector production weakness holding back improvements in greenfield sector delivery.

There will then be a further reduction in aggregate supply in 2026 to 116,700 dwellings followed by a modest recovery over the back end of the five year forecast period with 2029 expected to yield around 125,000 new homes.

Figure 1.17 presents the forward outlook for combined capital city dwelling production against the National Housing Accord target over the coming five years. This analysis indicates there will be around 393,000 dwelling shortfall which is underpinned by expectations of sustained weakness in the multi-unit sector.

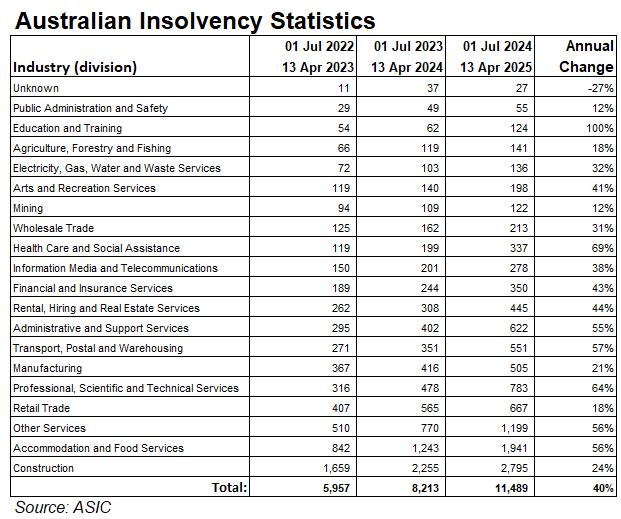

Data from the Australian Securities & Investments Commission shows that 3,393 businesses were declared insolvent in the March quarter, 27.6% higher than the same period in 2024.

Meanwhile, some 11,489 businesses have appointed insolvency specialists so far in the financial year, with the figures current as of April 13, representing an increase of 40% year over year.

As shown above, the construction sector leads the nation’s insolvencies, with 2,795 firms going under so far this financial year, representing a 24% increase on 2024.

Jarvis Archer from Business Reset says overall insolvencies are on track to exceed 15,000 in 2024-25.

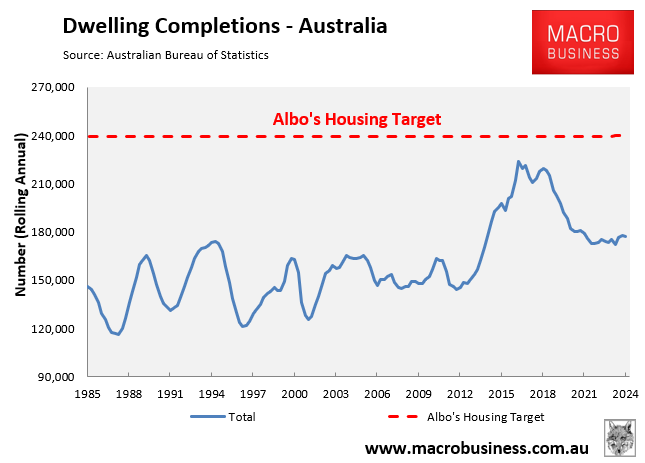

The high number of construction insolvencies is acting as a barrier to the Albanese government’s target of building 1.2 million homes in five years—a level of construction that Australia has never achieved.

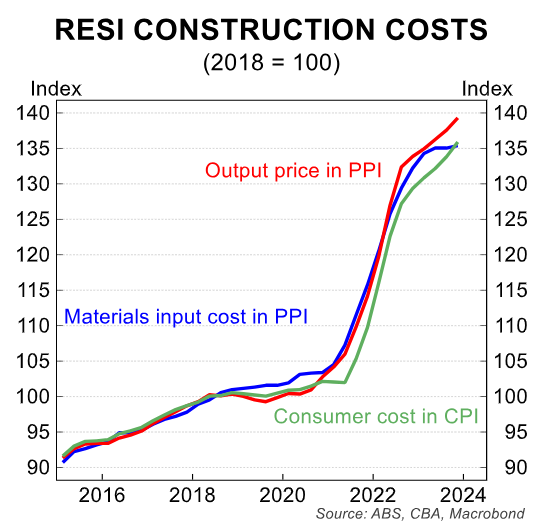

Combined with substantially higher construction costs, mortgage rates, and labour shortages, capacity in the homebuilding industry has been significantly decreased.

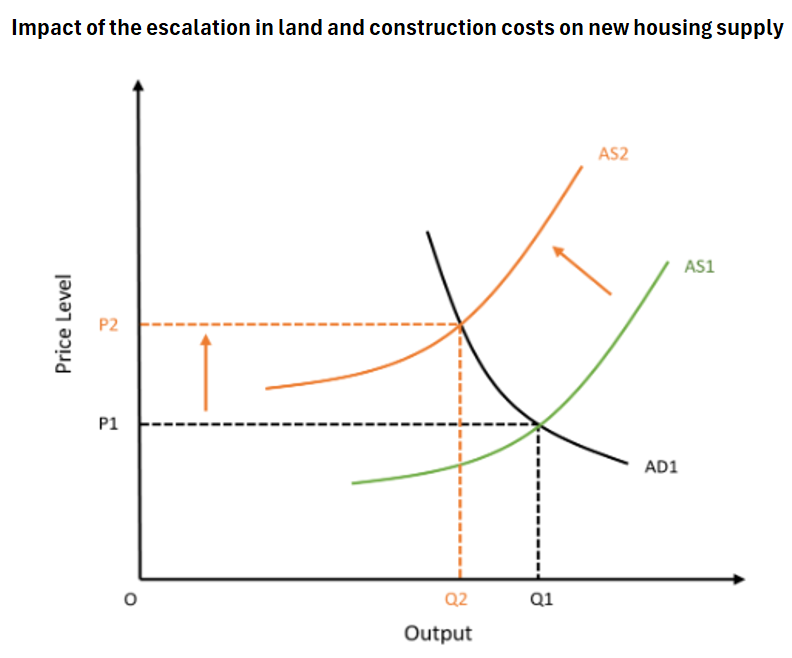

In fundamental economic terms, the supply curve for home building has shifted to the left, limiting the number of units that can be produced at each price point.

To restore market equilibrium, the federal government must significantly reduce demand by cutting immigration. Otherwise, Australia’s structural housing shortage will continue to worsen.