Westpac summarises the drivel.

One area that the RBA had previously pointed to as a reason for not being confident that inflation can be sustained at current levels is the tightness of the labour market. While it still highlighted indicators that suggested remaining tightness, the forecasts for unemployment have been lifted slightly, while those for employment and wages growth have been reduced slightly.

Documents released under Freedom of Information show that, as at March this year, the RBA’s models were implying that the NAIRU was 4.69%, only marginally down from the 4.75% estimate these models produced at the time of the February 2025 SMP. This is noticeably above the average estimate of the market economists that the RBA itself polls, and slightly above the maximum estimate reported in its survey.

The May SMP noted that its assessment of the location of full employment was unchanged, but both there and in the media conference, it was acknowledged that they could be overestimating the NAIRU and underestimating full employment. This contributed to some downward judgement in their inflation and wages growth forecasts.

While the staff are clearly grappling with the possibility they have been underestimating full employment, much of the analysis released in March centred on a ‘straw-man’ alternative hypothesis of a 4% NAIRU. Yet a NAIRU of 4¼% (in line with average estimate of market economists) would be enough to overturn the RBA’s concerns that the labour market is still too tight.

Of course, the Governor would counter that they look at a broader range of metrics than just the unemployment rate relative to NAIRU estimates when assessing where the labour market is relative to full employment. In the end, though, their inflation models require a NAIRU estimate, so their inflation outlook hinges on the realism of those estimates.

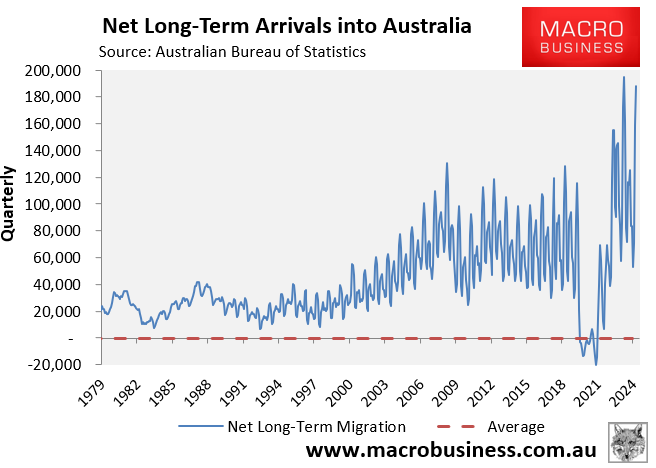

It should not be the NAIRU. It should be the NAIRI. The Non-Accelerating Rate of Immigration.

This is what will determine future interest rates.

If the NAIRI falls, that is immigration increases, then rates will fall as wages fade away.

If the NAIRI rises, that is, the immigration decreases, then rates will be more sticky with wages.

I put it to you that the NAIRI is currently running rather low.

And so, you can expect further rate cuts as wages are slowly cooked in the tandoor.