Although the macro newsflow was relatively light on overnight it was all about the bond and currency markets as the latest Canadian inflation numbers following yesterday’s cut by the RBA led to further introspection on the trajectory of the ECB, which has led to the USD being pushed back across the board. US sovereign debt concerns are still on the mind of traders alongside Japanese bond yields while the increased pressure on the UK looking to reverse its Brexit trade relations with the EU continues to highlight that there is next to nothing going on with other trade deals with the Trump regime.

The USD was sold off against the majors with Euro and Pound Sterling making new weekly highs while the Canadian Loonie continued to firm alongside the Australian dollar which has absorbed all of yesterday’s cut by the RBA to remain above the 64 cent level.

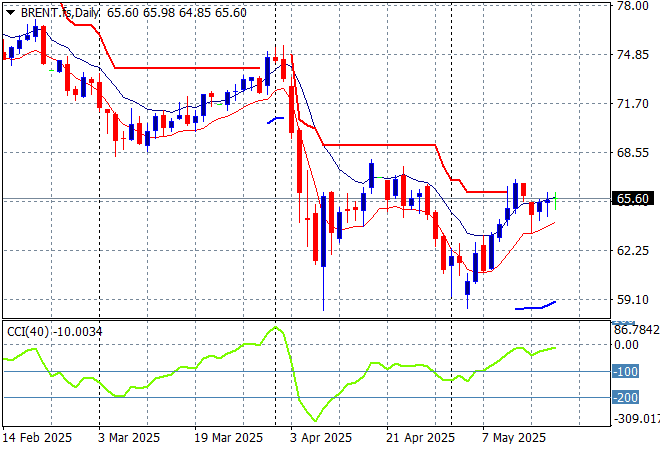

10 year Treasury yields stayed around the 4.5% level while oil prices remain somewhat weak with Brent crude still stuck above the $65USD per barrel level. Meanwhile gold is trying much harder after almost crossing below the $3200USD per ounce level on Friday night, with a big lift that approached the $3300 level this morning.

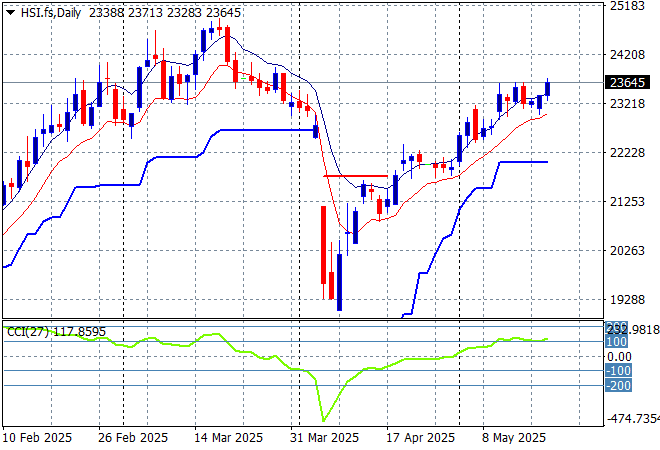

Looking at stock markets from Asia from yesterday’s session, where mainland Chinese share markets were able to hang on to their gains in afternoon trade with the Shanghai Composite up 0.4% to just above the 3380 point level while the Hang Seng Index lifted more than 1.4% to almost push above the 24000 point level.

The daily chart shows a near complete fill of the March/April selloff although momentum is now picking up again and remains slightly overbought as the 90 day “relief” continues without any further positive news:

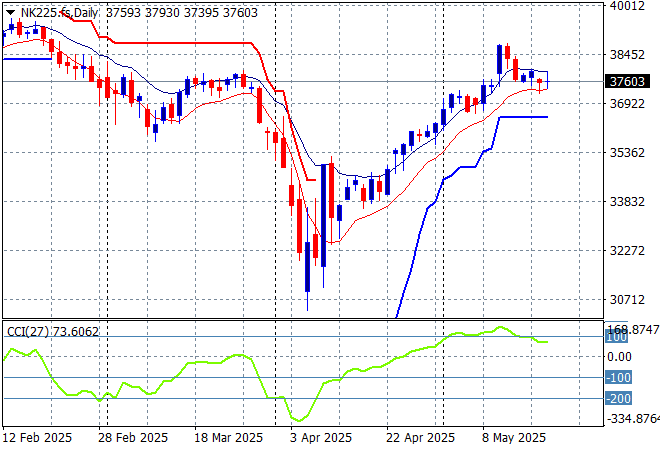

Japanese stock markets were treading water however on the stronger Yen with the Nikkei 225 up just 0.1% to 37528 points.

Daily price action is looking very keen indeed although daily momentum has slowed down somewhat, it has cleared resistance at the 36000 point level with another equity market that looks stretched:

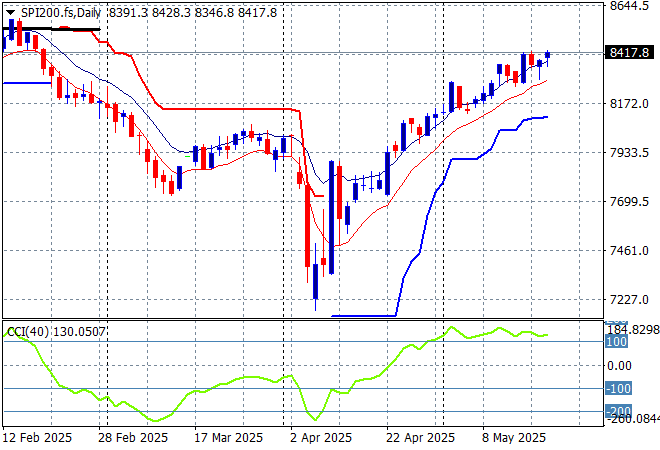

Australian stocks also put in a solid session to clawback the start of week losses with the ASX200 up 0.6% at 8343 points.

SPI futures are up more than 0.6% despite the pullback on Wall Street overnight. The daily chart pattern suggests further upside is still possible as the inverted head and shoulders pattern is nearly complete with the RBA cut yesterday helping boost this even further:

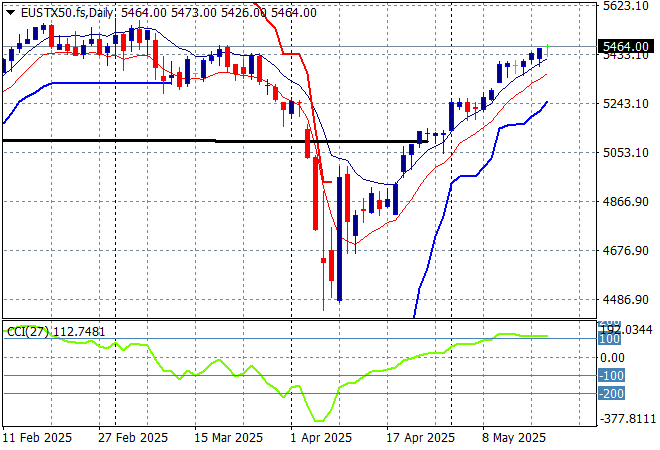

European markets had much more solid sessions across the continent with the FTSE leading the way up nearly 1% on “Brex-in” news as the Eurostoxx 50 Index 0.5% higher at 5454 points.

Support at the previous monthly support levels (black line) at 5100 points is now firmly held with the bounce off the 2024 lows at the 4400 point level indicating a massive fill of this dump and pump action with the former February highs nearly complete. Potentially further cuts from the ECB may help support this rally:

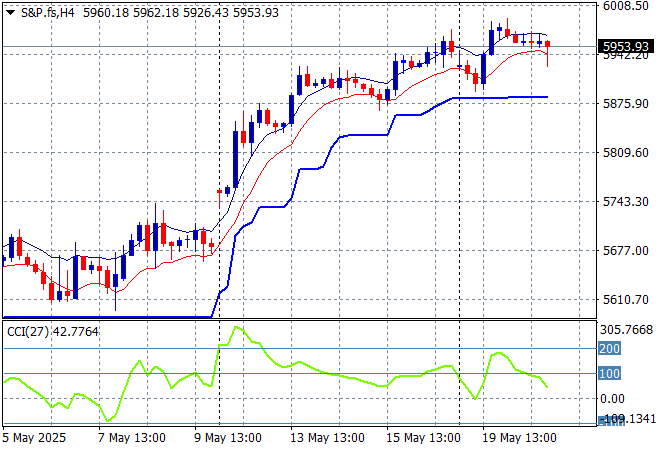

Wall Street however is stalling at best with the NASDAQ and the S&P500 both finishing nearly 0.4% lower at the end, the latter unable to close back above the 6000 point level at 5940 points.

The four hourly chart is supporting a potential slowdown action here that could be translating to a top on the daily chart as prices gets back above the pre-Trump Tariff Tax day at the same time that the real macroeconomic effect on them is starting to be felt by US consumers:

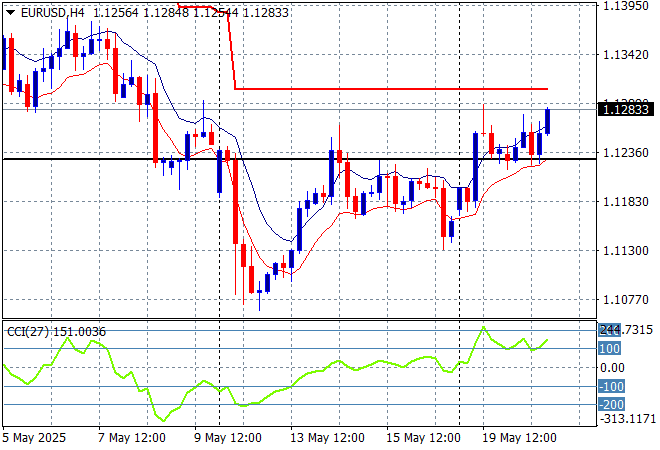

Currency markets are slowly coming back against USD following the Moody cut from Friday night with Euro getting well above the 1.12 handle overnight, with Pound Sterling also pushed up to a new weekly high and the Loonie drifting higher as the latest Canadian inflation number came in slightly hotter than expected.

The union currency was pushed back below the 1.13 handle last week as support bounced back to the 1.12 level which corresponds to the 2023 and 2024 highs but a potential breakout above trailing ATR resistance here on the four hourly chart is brewing:

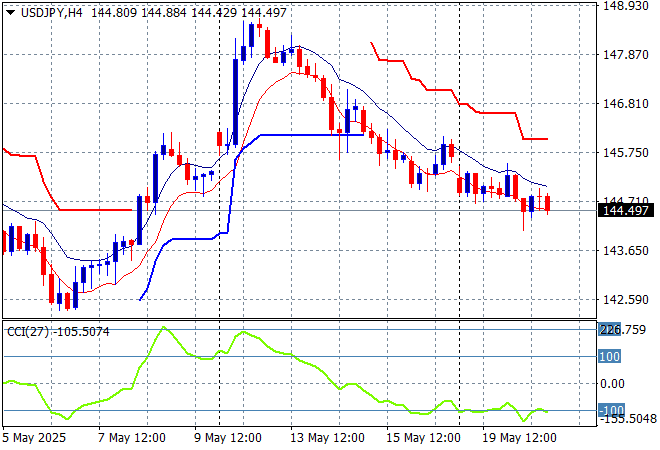

The USDJPY pair retraced all last trading week after getting way ahead of itself at the 149 level, and continues to be pushed back down to the 144 handle with the potential to break below in the coming session.

I still contend we need to watch for any sustained break below the 139 level which completes a multi year bearish head and shoulders setup that could see the 110 to 120 level revisited. No trade deal yet!

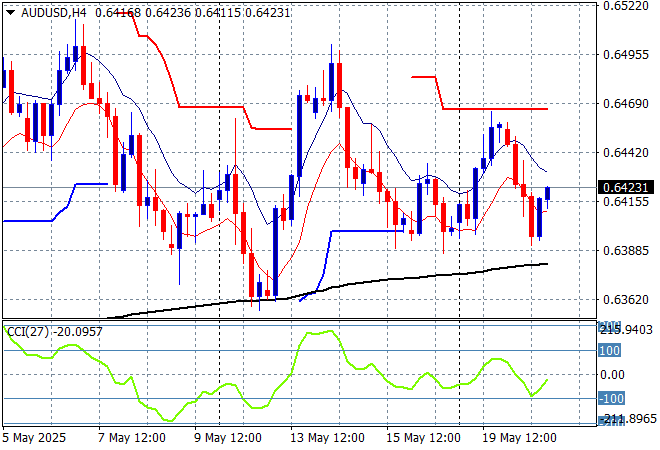

The Australian dollar was previously slowly extending its gains above the 64 cent level to extend above the pre-tariff announcement levels, with a mild pull back looking to be filled again as we yesterday’s RBA meeting and 25bps cut was largely absorbed overnight.

Stepping back for a longer point of view (and looking at the trusty AUDNZD weekly cross) price action has crossed back above the 200 day MA (moving black line) after bouncing off a near new five year low. This is all about the USD, not the Australian economy – or is it? – so I’m wary here but you’ve got to follow price, keeping an eye on temporary support at the 63 cent level:

Oil markets are trying hard to hold onto its post tariff bounce but continue to face other geopolitical ructions and OPEC pushing supply with Brent crude still stuck around the $65USD per barrel level again after recently almost making a new weekly low.

The daily chart pattern shows the post New Year rally that got a little out of hand and now reverting back to the sideways lower action for the latter half of 2024. The potential for a return to the 2024 lows is still building here as domestic demand in the US is likely to continue to decline as the Trump Taxes take effect:

Gold pulled back again on Friday night after sharply moving higher in recent weeks as it got way ahead of itself at least on the short term charts but is now making a very solid effort to get back on track back as it almost breached the $3300USD per ounce level overnight.

Short term support had firmed immensely in recent sessions showing real strength but momentum became considerably overbought so this was inevitable as price action has reverted back to the uptrend line from the April lows. There is further support at the $3200 level that could be tested next on the overshoot:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out/wrong on your position, so cry uncle and get out!