The big news of the day is a possible reversal of ALL of the Trump regime’s tariffs (except steel/aluminium) due to a court order, although it remains to be seen if Don Taco will actually abide by the legal decision. This has seen a big relief rally across all risk markets and with the USD taking a small hit as the Australian dollar solidifies above the 64 cent level, but this could be temporary as the latest Q2 GDP estimates roll in later tonight.

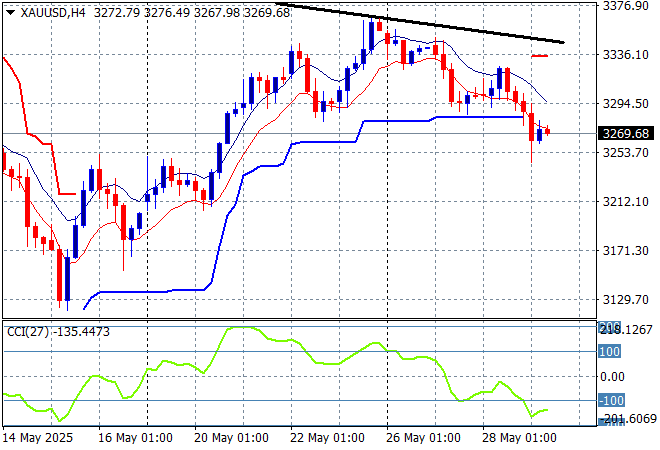

Oil markets are seeing a small bid higher after recently losing momentum with Brent crude now above the $64USD per barrel level while gold is failing to consolidate as it remains depressed below the $3300USD per ounce level:

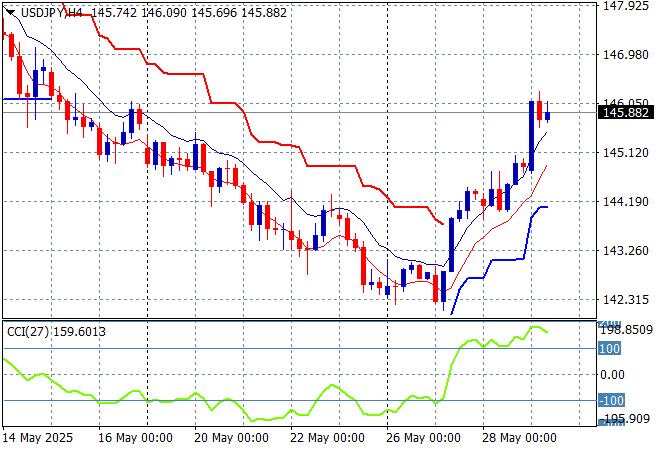

Mainland Chinese share markets are surging in the afternoon session with the Shanghai Composite up more than 0.6% while the Hang Seng Index is doing even better, up by more than 0.9% to extend well above the 23000 point level. Japanese stock markets are outperforming everyone however with the Nikkei 225 up more than 1.8% to 38455 points while trading in the USDPY pair has seen a return back above the 145 level:

Australian stocks were able to eke out a small lift higher with the ASX200 closing up just 0.1% to 8409 points while the Australian dollar has steadied somewhat just above its former point of control around the 64 cent level:

S&P and Eurostoxx futures are lifting much higher going into the London session with the S&P500 four hourly chart showing a potential return to the recent highs near the 6000 point level as short term momentum gets considerably overbought:

The economic calendar includes the latest 2Q GDP estimates for the US plus weekly initial jobless claims.