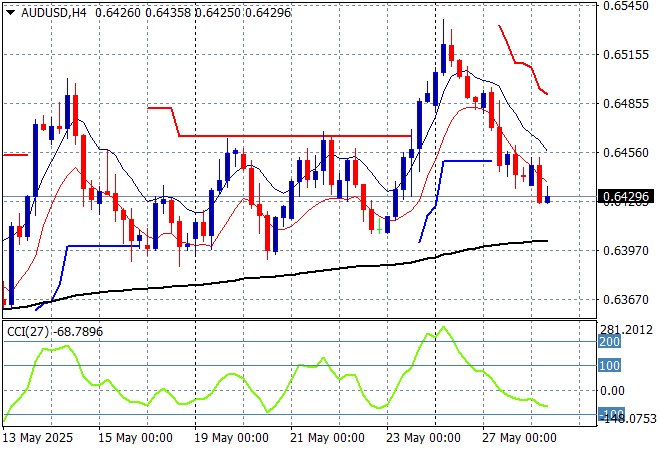

A couple of comments from the BOJ over the Japanese bond market and the ongoing trade war with the US didn’t upset most risk markets in Asia as they move in correlation with a resurgent Wall Street. The latest local inflation figures came in a little hotter than expected but this was overshadowed somewhat by the latest RBNZ cut with local shares steady while the Australian dollar fell back slightly to remain slightly above the 64 cent level.

Oil markets are trying to stabilise but are losing momentum with Brent crude pushed down to the $64USD per barrel level while gold is also consolidating after its Friday night surge above the $3350USD per ounce level:

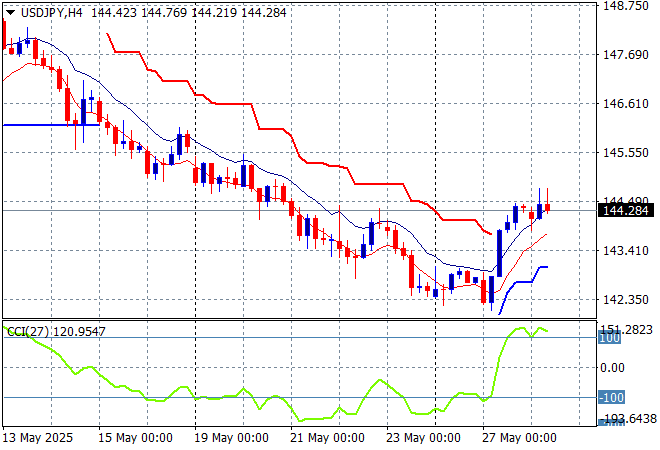

Mainland Chinese share markets fell slightly in the afternoon session with the Shanghai Composite still down 0.1% or so while the Hang Seng Index is off by more than 0.7% to remain just above the 23000 point level. Japanese stock markets are again doing better on the weaker Yen with the Nikkei 225 up more than 0.3% to 37822 points while trading in the USDPY pair has seen a return back above the 144 level, but this could be brief:

Australian stocks were unable to continue the recent upward momentum with the ASX200 losing some 0.1% to 8401 points while the Australian dollar also has returned to its former point of control around the 64 cent level after moving lower in sympathy with the RBNZ cut:

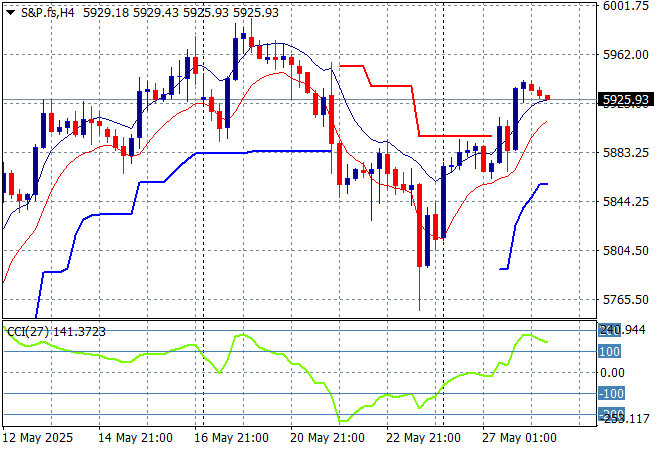

S&P and Eurostoxx futures are steady going into the London session with the S&P500 four hourly chart showing a potential return to the recent highs near the 6000 point level although short term momentum is considerably overbought:

The economic calendar includes German unemployment and the release of the latest FOMC minutes.