Risk markets in Asia are mainly stepping back in response to the falls overnight on Wall Street but more so on the burgeoning bond troubles as the US fiscal position looks to go into permanent deficit decline with the imminent passing of the Trump regime’s “tax” aka wealth redistribution billr. In currency markets, the USD is still losing ground with Yen firming despite some saccharine comments about trade while Euro and Pound Sterling hold on to their new weekly highs as the Australian dollar remains robust above the 64 cent level.

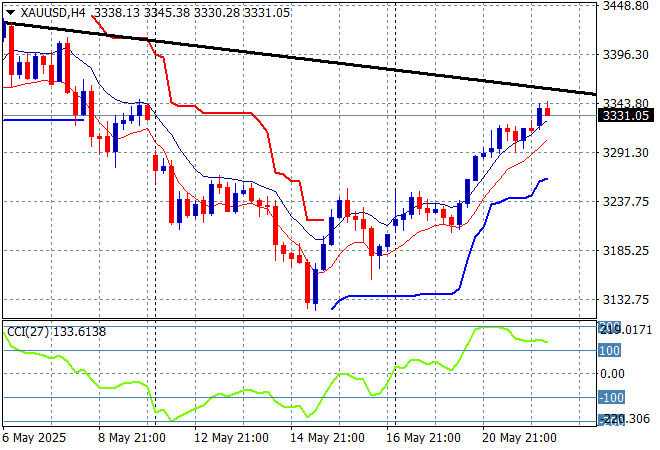

Oil markets are trying to stabilise with Brent crude retracing back below the $65USD per barrel level again while gold is pushing higher after fighting back from its recent decline, now extending above the $3330USD per ounce level this afternoon:

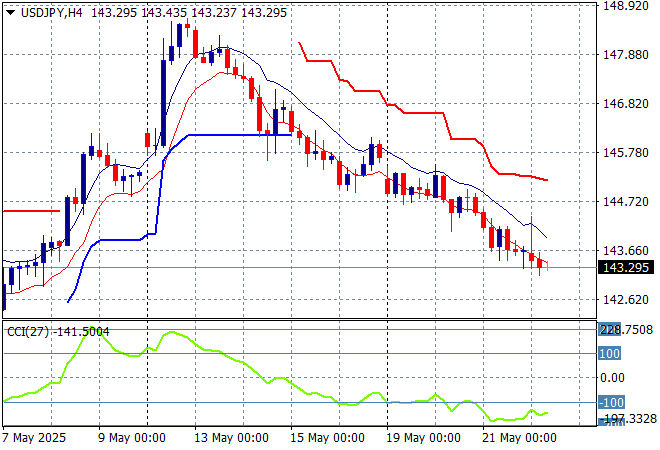

Mainland Chinese share markets are sliding back in the afternoon session with the Shanghai Composite down 0.2% while the Hang Seng Index has lost nearly 1% as it fails to push above the 24000 point level. Japanese stock markets are seeing similar losses on the strengthening Yen however with the Nikkei 225 down more than 0.9% to 36958 points while trading in the USDPY pair has seen a further move lower as it heads towards the 144 level:

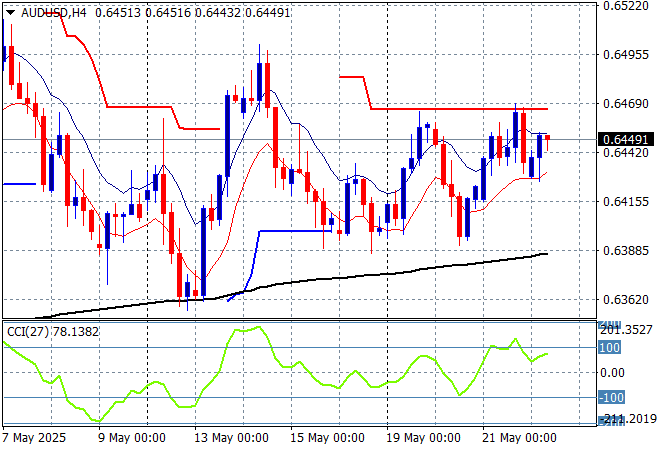

Australian stocks were the best of a bad bunch with the ASX200 losing only 0.4% at 8350 points while the Australian dollar has held around the mid 64 level to match its post RBA meeting move with markets keeping the Pacific Peso contained for now:

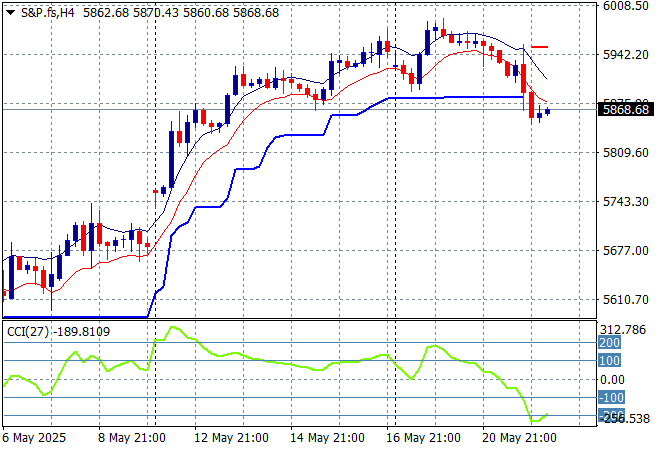

S&P and Eurostoxx futures are sliding back further going into the London session with the S&P500 four hourly chart still showing a slowdown here in short term momentum in the wake of the Moody’s cut, as price heads back down to the 5900 point level:

The economic calendar is relatively quiet again tonight although we do get the latest US initial jobless claims and a slew of flash PMI surveys.