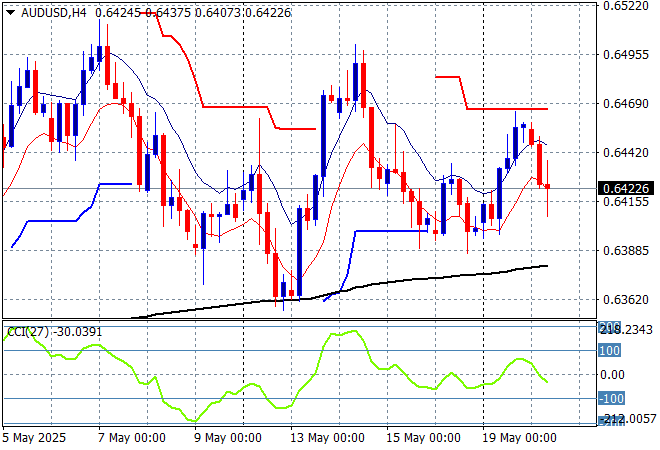

Risk markets in Asia are somewhat mixed in reaction to the flat sessions on Wall Street overnight with the Friday night cut by ratings agency Moody on US debt still reveberating, particularly within bond markets. The Trump regime is still failing to make deals with Japan which is seeing further strength in Yen while today’s 25bps cut by the RBA has seen the Australian dollar only lose minor ground as it stays well above the 64 cent level against USD.

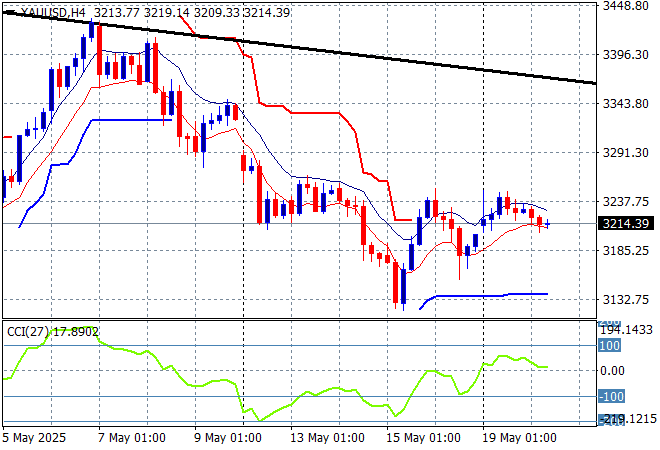

Oil markets are still trying to stabilise with Brent crude stuck at the $65USD per barrel level while gold is trying to fight back but is just holding on below the $3220USD per ounce level this afternoon despite a weaker USD:

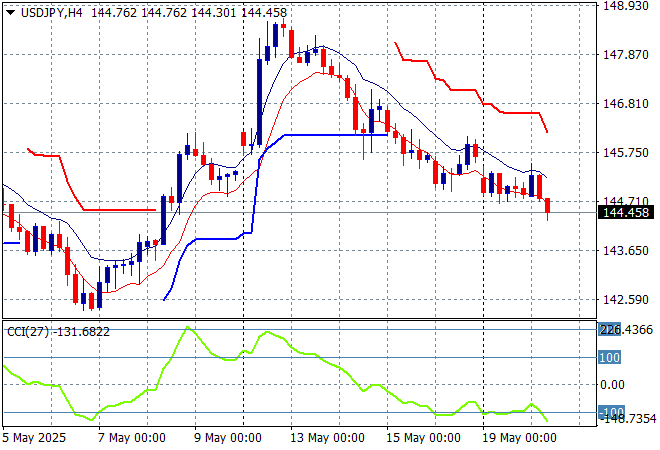

Mainland Chinese share markets are doing better in afternoon trade with the Shanghai Composite up 0.4% to just above the 3380 point level while the Hang Seng Index has gained more than 1.2% to almost push above the 24000 point level. Japanese stock markets are treading water however on the stronger Yen with the Nikkei 225 down more than 0.2% to 37468 points while trading in the USDPY pair has seen a further move lower as it retraces back to the 144 level:

Australian stocks have put in a solid session to clawback the start of week losses with the ASX200 up 0.6% at 8343 points while the Australian dollar has held just above the 64 handle despite the expected cut in today’s RBA meeting:

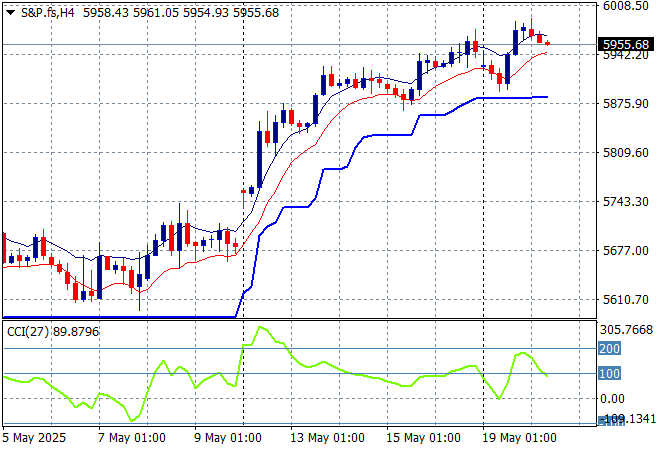

S&P and Eurostoxx futures are sliding back a little going into the London session with the S&P500 four hourly chart still showing a slowdown here in short term momentum in the wake of the Moody’s cut back down to the 5900 point level:

The economic calendar is relatively quiet again tonight with a slew of Fed speeches.