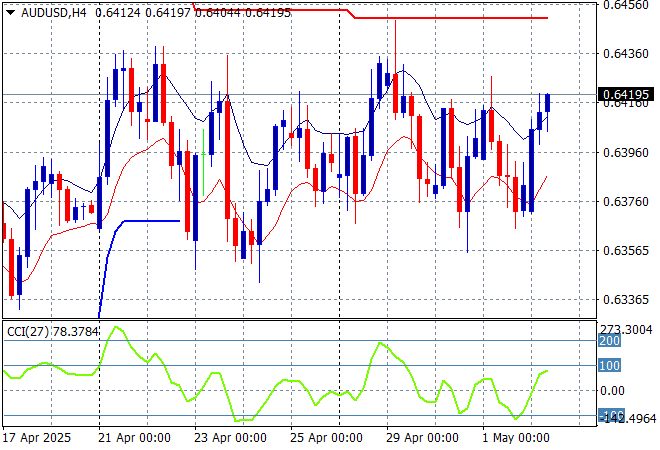

Risk markets are having a solid finish to the trading week while recent news that the Chinese may actually be open to talking about tariffs with the US, plus the Canadian auto industry seemingly getting another exemption on parts, with futures indicating an even better start in Europe. All eyes will be on the latest US jobs figures tonight although the USD is starting to pullback a little as the Australian dollar gets back above the 64 cent level this afternoon.

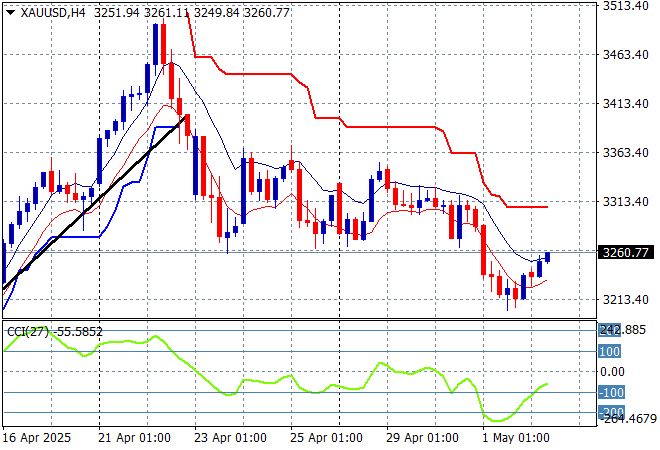

Oil markets are trying to stabilise with Brent crude getting back above the $62USD per barrel level but still looking weak while gold is fighting back after slipping below the $3300USD per ounce level with a small bounceback this afternoon:

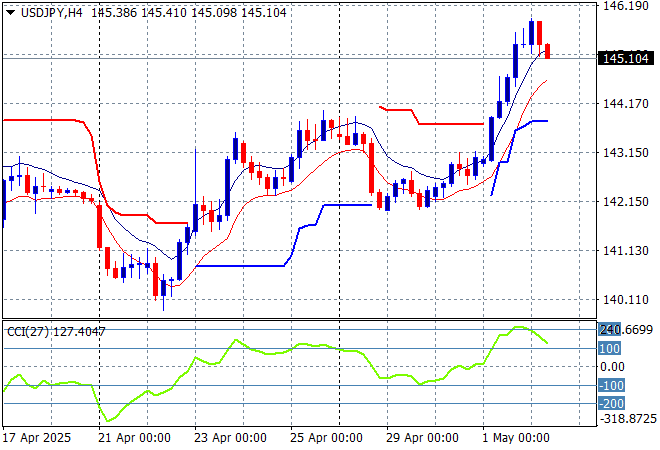

Mainland and offshore Chinese share markets are closed for the May day holidays while Japanese stock markets are up strongly again with the Nikkei 225 lifting more than 1% higher to 36808 points while trading in the USDPY pair has seen a pullback after overshooting overnight above the 145 level:

Australian stocks have managed a very solid session with the ASX200 up 1% to8238 points while the Australian dollar has been able to get back above the 64 handle as it thinks about another breakout before this weekend’s election:

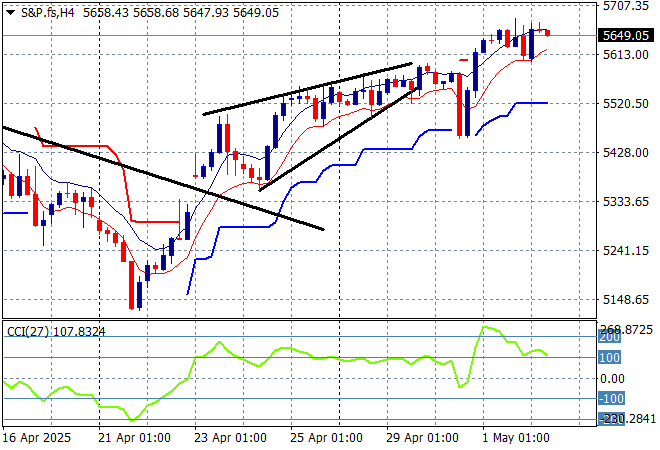

S&P and Eurostoxx futures are jumping a bit on some Canadian auto tariff pullback as we go into the London session with the S&P500 four hourly chart showing a potential to breakout again at the 5600 point level:

The economic calendar will focus squarely on tonight’s NFP. If its good, Trump will claim its because of him, if it’s bad, it was Biden’s fault.