Westpac with the note.

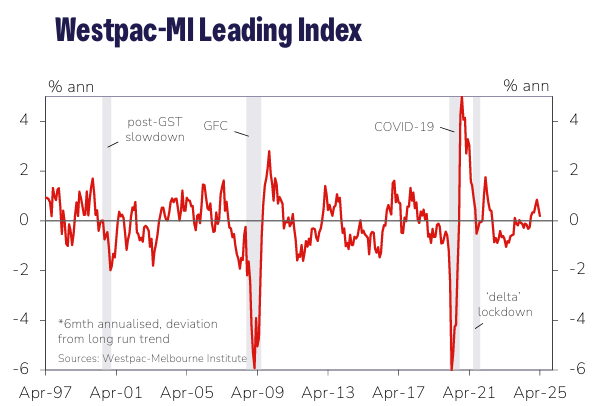

The six-month annualised growth rate in the Westpac

Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, slowed to 0.2% in April from 0.5% in March.

The above-trend growth pulse that emerged at the start of the year has all but disappeared. The shift reflects heightened uncertainty around global trade and a less supportive commodity price backdrop.

While most of the drag is ‘external’, domestic drivers are also fairly mixed with labour market momentum slowing and interest rate settings providing only modest support.

The overall picture is consistent with some stalling in what was already expected to be a gradual growth recovery for the Australian economy in 2025.

Westpac expects GDP growth to lift to 1.9%yr by year-end, a sub-par result by historical standards. The Leading Index growth rate is now unchanged on six months ago.

Over that time, five of the eight components have seen weaker signals while the remaining three have firmed.

The weakening signal has come from financial market and sentiment-based components.

The biggest additional drags have come from: the Westpac–Melbourne Institute Consumer Expectations Index (taking 0.23ppts off the headline growth rate); the S&P/ASX200 (–0.12ppts) and the WestpacMelbourne Institute Consumer Unemployment Expectations Index (–0.1ppts).

Dwelling approvals and total hours worked have also shaved a further 0.1ppts off the headline growth rate on a combined basis.

Over the last six months, this additional drag has been offset by more positive contributions from commodity prices (adding 0.24ppts to the headline growth rate), US industrial production (+0.17ppts) and the yield spread (+0.15ppts).

However, all of these components have become less supportive in the last few months. In the case of commodity prices, which are measured in AUD terms, strong gains late last year have given way to a partial retracement since January.

US industrial production has also moderated from a mini-surge late last year. The yield spread component is also providing less positive impetus – reflecting, at short end of the interest rate curve, the RBA’s gradual policy easing and, at the long end, downgraded global growth prospects.

The Reserve Bank Monetary Policy Board next meets on July 7–8. As expected, the Board lowered the cash rate target by 25bps to 3.85% at its May meeting, citing increased confidence around inflation and an expectation The Westpac-Melbourne Institute Leading Index of Economic Activity is designed to assist in identifying turning points in the economy.

The index combines variables that reflect different aspects of the economy into a single index that generally produces a more reliable cyclical indicator than any single component taken individually.

The Leading Index of Economic Activity provides advance information on the state of the economy and gives early warnings of cyclical turning points. that international developments would exert some drag on the economy.

That drag is already starting to show through more clearly in Leading Index growth reads. That said, it does not look too threatening at this stage, with most of the effect coming via sentiment and financial markets rather than a hit to trade and export prices.

As such, we continue to expect the RBA to take a cautious, measured approach to policy easing with the meeting in early July likely to see policy left on hold as it awaits another quarterly update on inflation on July 30.