From Goldman:

From a macro perspective, we leave our forecasts for Australia unchanged given the outcome was not a surprise and the ALP’spost-Budget policy announcements have been fairly modest (0.0-0.1% of GDP).

We note most of the policies announced in the Budget on 25 March, including income tax cuts for households, have already been legislated.

We continue to expect overall fiscal settings in Australia to add around 0.7ppts to GDP growth over 2025 (compared to 1.4ppts over 2024), with overall GDP rising 1.7% in 2025 – above last year’s outcome (1.0%) but below our estimate of potential GDP growth in Australia (~2.6%).

Of course, had the LNP won, interest rates would likely have headed materially lower given the scale of spending cuts being mooted.

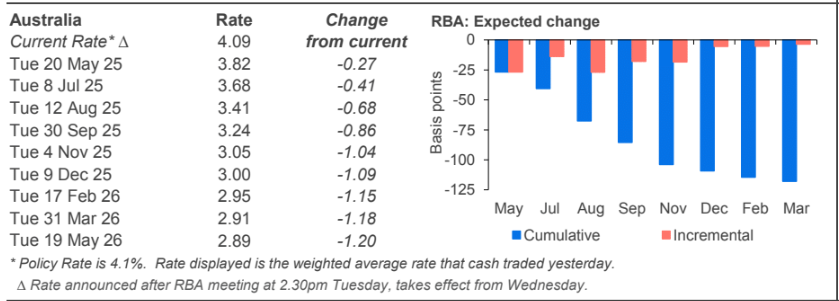

Markets are expecting four cuts in the year ahead, which seems fair.

Where I differ from markets is in the view that 2026 will be the bottom of the cycle. As iron ore prices are killed by the supply deluge and ongoing Chinese slowdown, and local inflation is squashed by mass immigration, I expect rates to keep falling next year as well.