The latest data suggests that momentum in the housing market has softened as buyers await further interest rate cuts from the Reserve Bank of Australia (RBA).

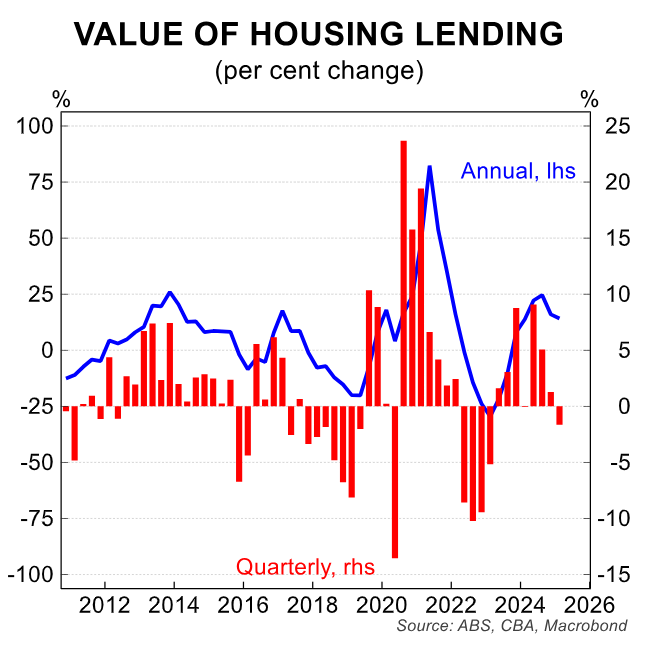

This week’s mortgage finance data from the Australian Bureau of Statistics (ABS) showed that the value of new housing lending declined by 1.6% in the March quarter, taking the annual growth rate down to 14.2%.

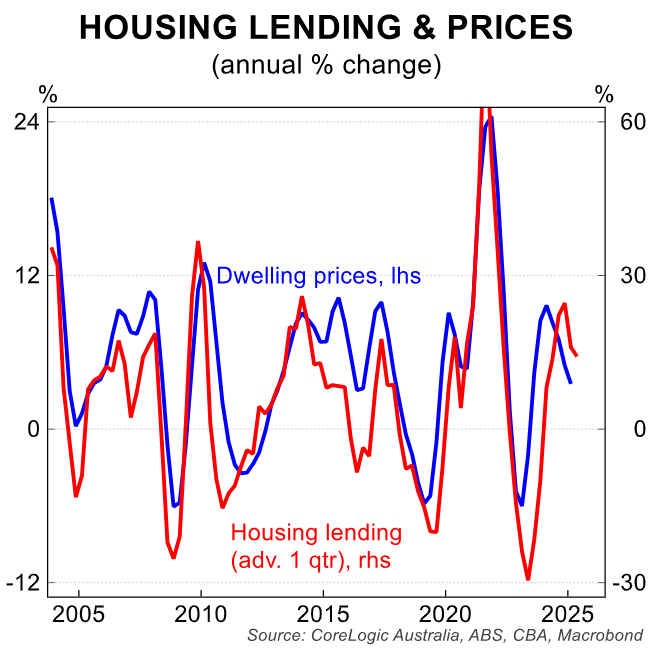

The slowdown in mortgage lending is being reflected in home prices, where growth has also moderated.

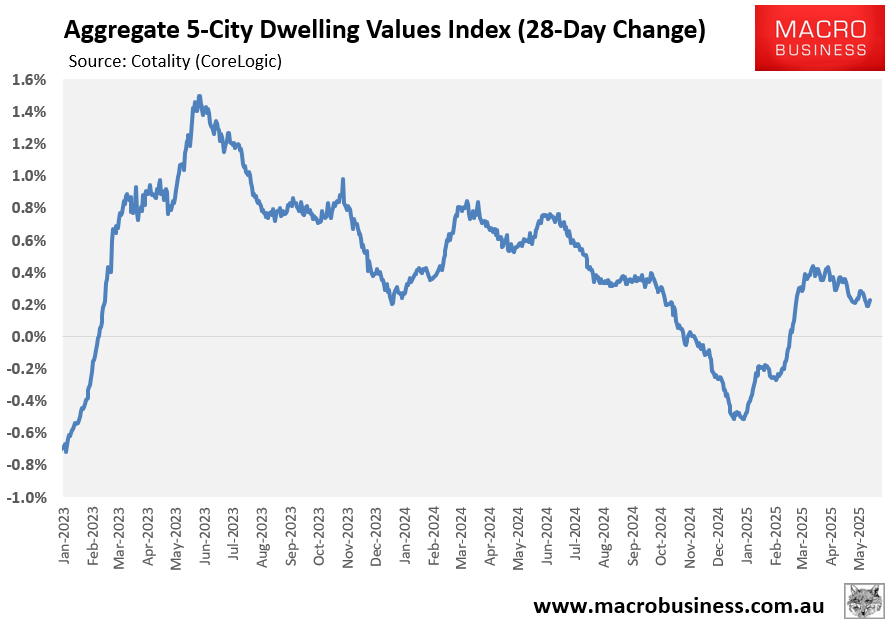

Cotality’s (formerly CoreLogic’s) daily dwelling values index shows that the rate of growth across the five major capital cities has halved from the recent peak in March following the RBA’s February interest rate cut.

However, buyer interest is growing in anticipation of imminent interest rate cuts and stimulatory policy changes.

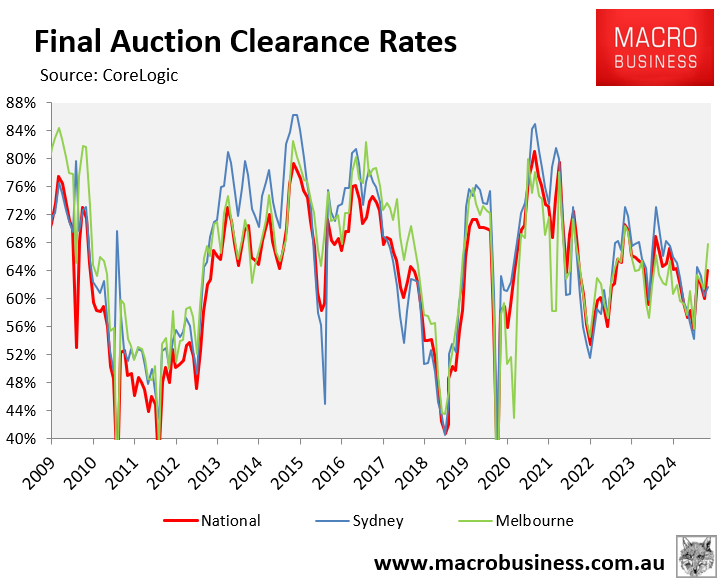

Auction clearance rates are rebounding, with last week’s combined final clearance rate of 65% the highest since July 2024.

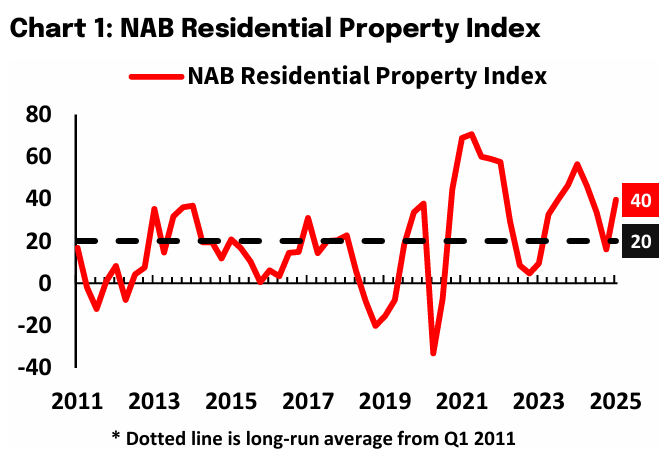

NAB’s latest Residential Property Survey of industry insiders shows that sentiment rose to a level well above average (+40) in March, with most property professionals believing the market is at the start of a recovery.

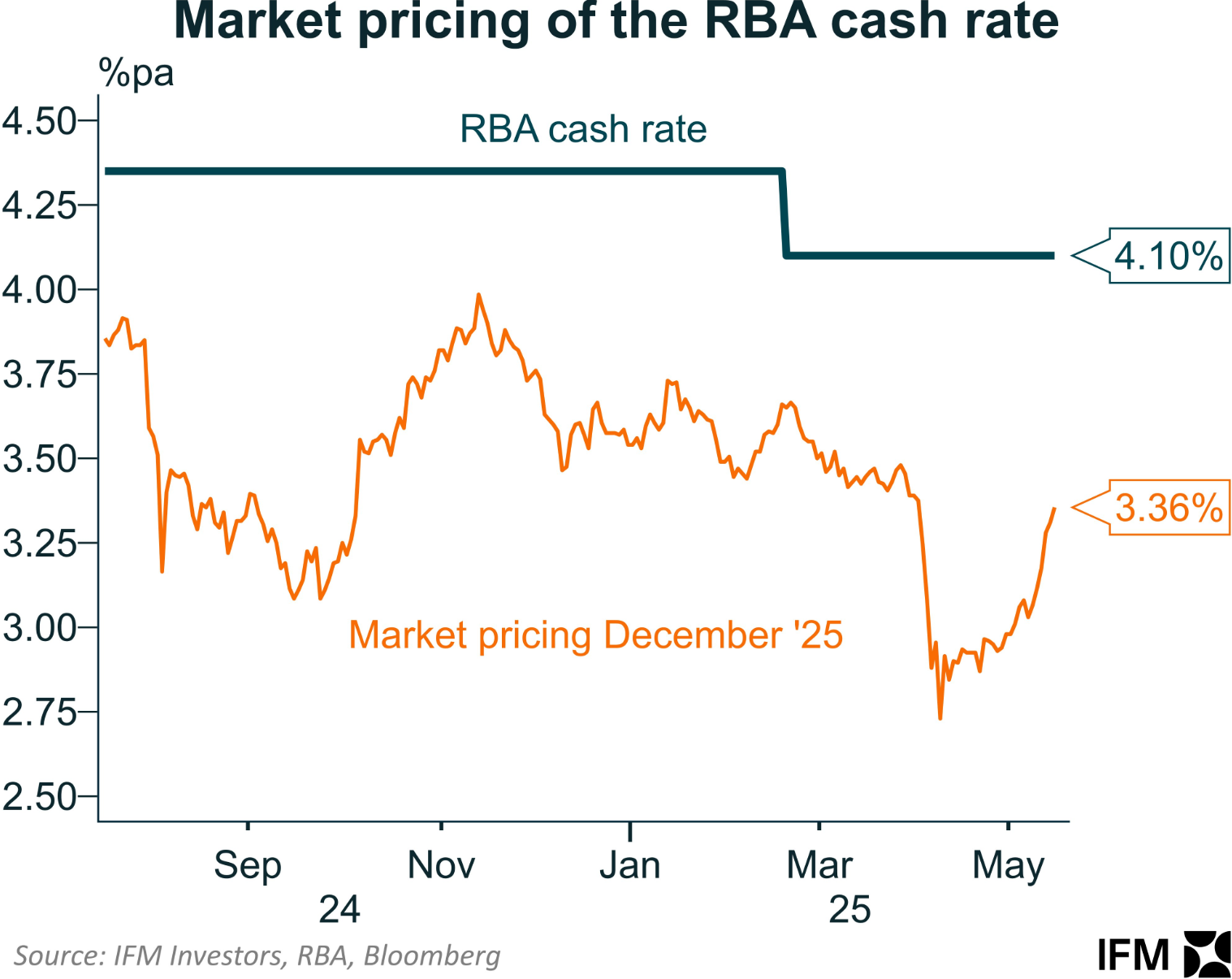

The most recent forecast for interest rates in the futures market predicts that Australia’s official cash rate will reduce by 0.75% this year, ending 2025 at 3.35% (versus 4.10% currently).

CBA and Westpac have the same rate forecast, whereas NAB is more dovish, tipping an end-of-year cash rate of 2.85%.

Regardless, interest rate cuts will provide significant stimulus to the market.

The housing market will receive further stimulus once the Albanese government’s 5% deposit scheme for first home buyers comes into effect on 1 January 2026.

The government’s tax on unrealised capital gains for superannuation accounts with balances over $3 million could also see some high net worth investors shift their money out of superannuation and into residential property, further stimulating demand.

The upshot is that the combination of lower interest rates and stimulatory policies is likely to boost housing demand, driving up prices.