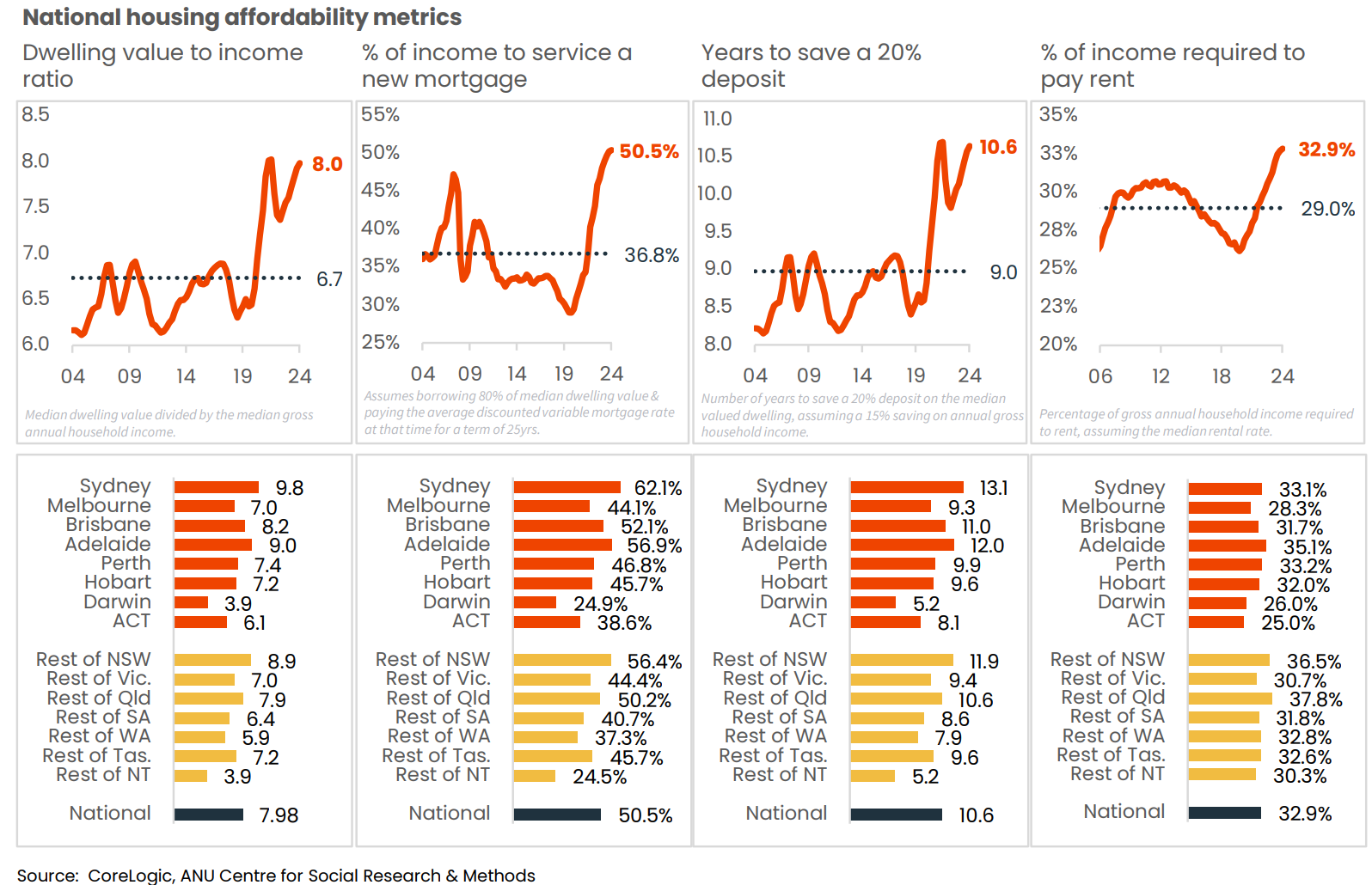

Australia is experiencing a housing crisis because its home prices are among the highest in the world compared to incomes, we have some of the most indebted households in the world, and tenants are paying a record share of their income on rent.

According to CoreLogic, the total value of Australia’s housing stock was $11.3 trillion in April 2025, with the average home valued at exactly $1 million.

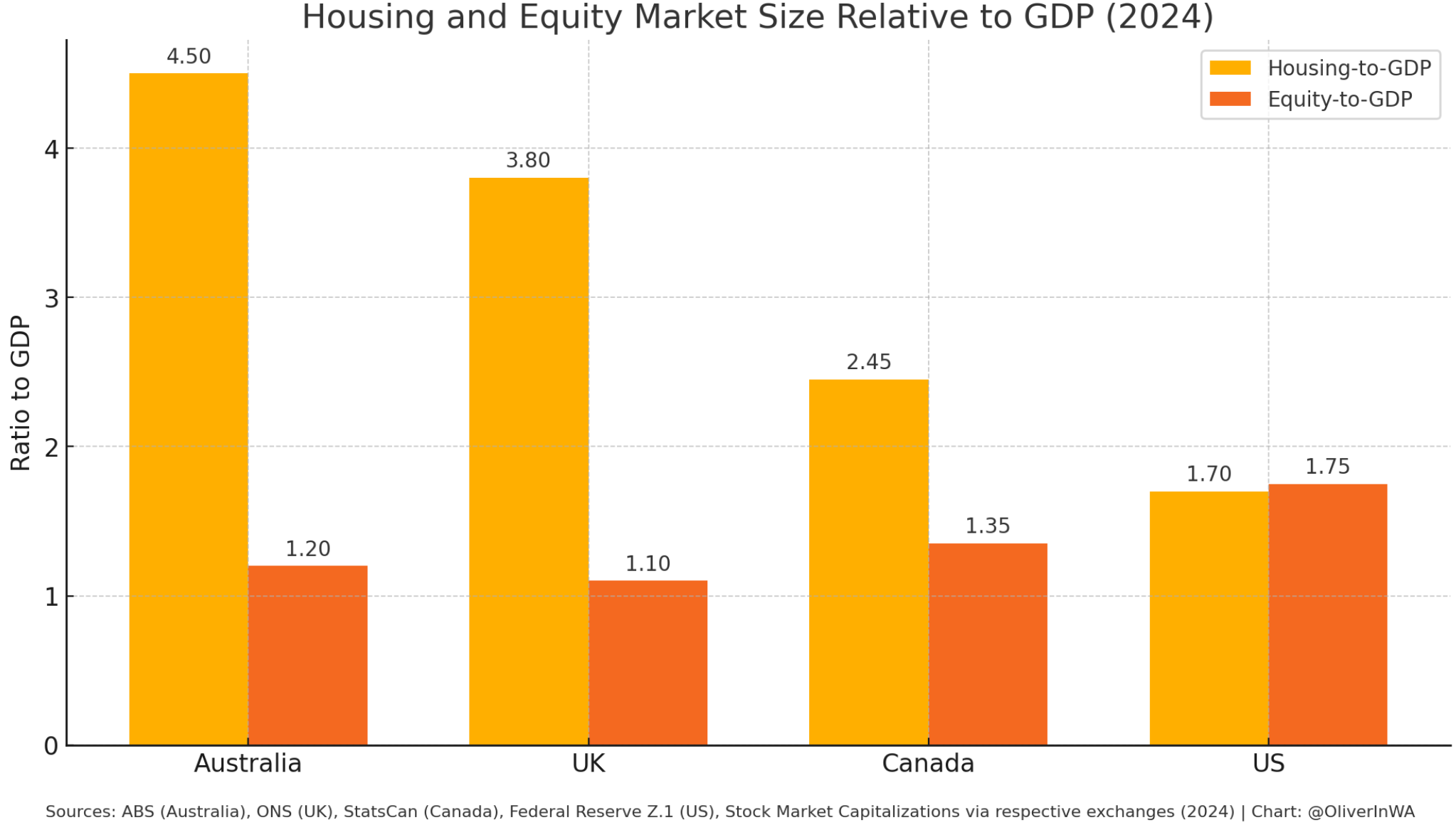

Compared to other English-speaking nations, Australians have more wealth tied up in housing and less in stocks.

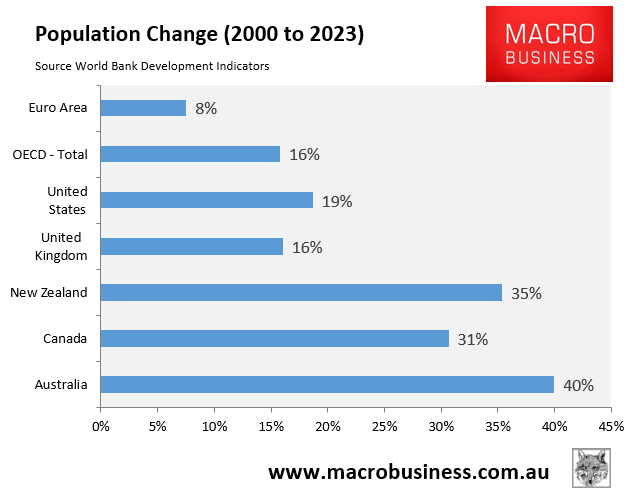

One reason why property prices and rentals are so expensive is because Australia has experienced an abnormally large population increase due to immigration, and demand has far outpaced supply.

According to the ABS population clock, Australia’s population has increased by 8.7 million people (46%) this century, the highest percentage rise in the developed nations.

One person arrives to live in Australia every 44 seconds.

This population surge has resulted in a persistent lack of housing for purchase and rental.

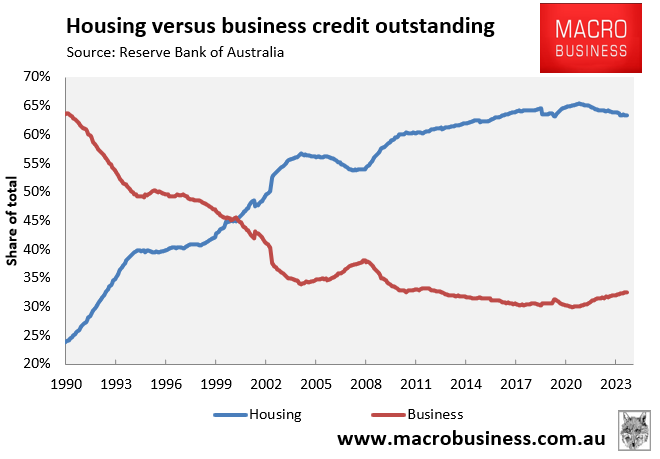

The flood of funds into property has also deprived businesses of capital and reduced Australia’s productivity.

In 1990, businesses received about two-thirds of all bank loans, with mortgages and personal loans accounting for the other third.

Thirty-five years later, the ratio has flipped, with around two-thirds of bank financing for housing.

Australia’s housing crisis to worsen:

House prices in Australia are set to grow sharply in the coming year or so.

Financial markets expect the Reserve Bank of Australia (RBA) to slash interest rates four more times this year, with the cash rate expected to fall to 3.10% by the end of 2025.

Lower interest rates will increase borrowing capacity and buyer demand, lifting prices.

House prices will also rise significantly when Labor’s 5% deposits for all first-time purchasers come into effect on January 1, 2026.

Labor’s policy will boost borrowing capacity and attract more first-time home buyers into the market, increasing overall buyer demand and prices.

Australian renters are also facing bleak conditions.

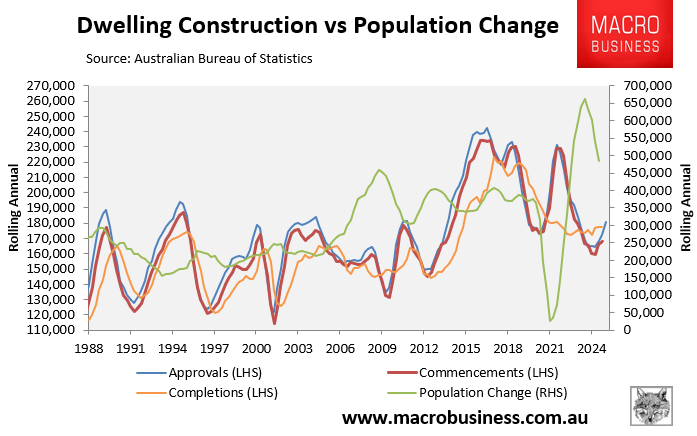

Data on dwelling approvals and commencements continues to fall significantly short of the government’s housing construction target.

Only 168,050 homes began construction in the year to Q4 2024, 71,950 (30%) lower than the annual run rate of 240,000 required to reach Labor’s housing target, which came into effect on July 1, 2024.

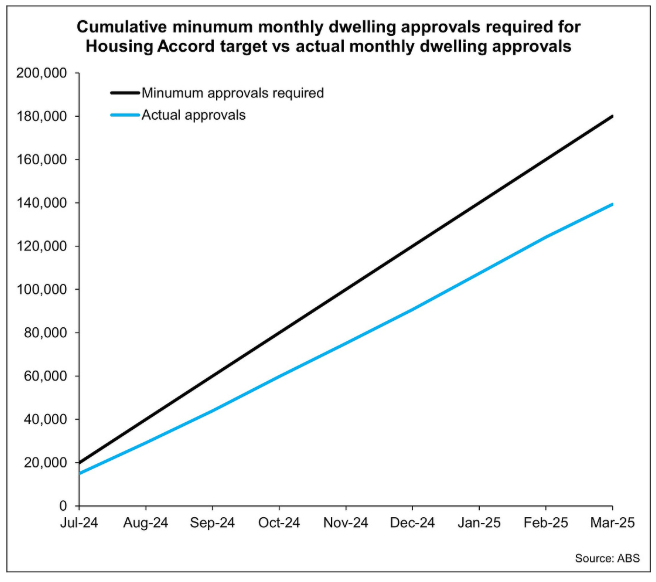

Over the first nine months of the Housing Accord, 139,352 homes were approved for construction, which is 23% less than the requirement of at least 180,000.

Chart by Cameron Kusher

Historically, only around 94% of approvals end up being completed, suggesting that the supply situation is worse than suggested in the chart above.

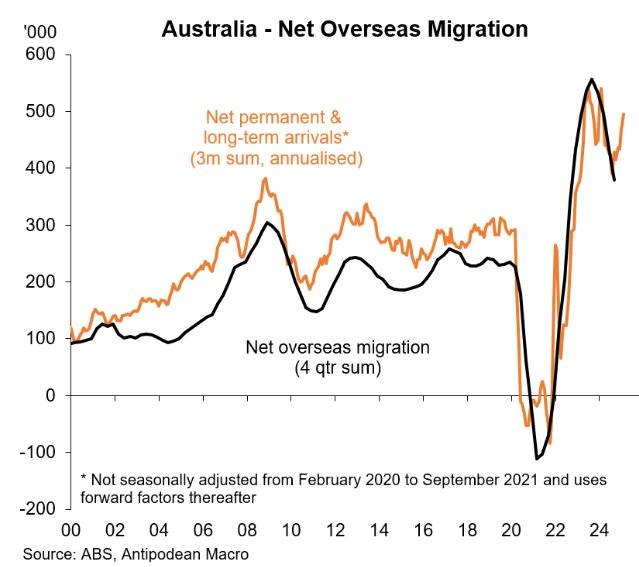

At the same time, immigration appears to be picking up again.

Certainly, the joyous celebrations of migration agents, international students, and the Indian community following the Albanese government’s reelection suggest that immigration will remain hot:

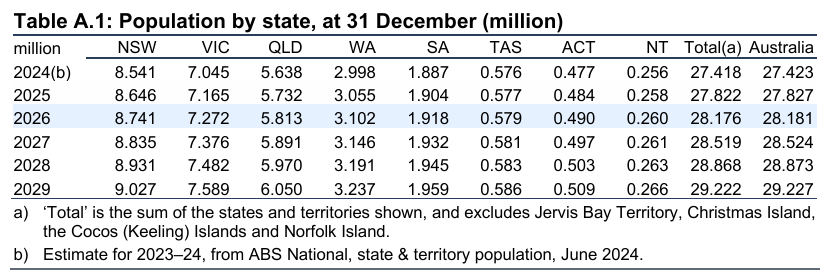

The March federal budget conservatively forecast a 1.8 million population rise over the next five years, with the majority settling in New South Wales, Victoria, and Queensland.

Source: March 2025 federal budget

Where will they live?

I discussed these issues in my weekly Treasury of Common Sense on Radio 2GB/4BC.