DXY is grinding higher.

AUD fell.

Lead boots are doing OK.

Gold’s shakeout contines.

Metals revert to mean.

Miners yawn.

EM yawn.

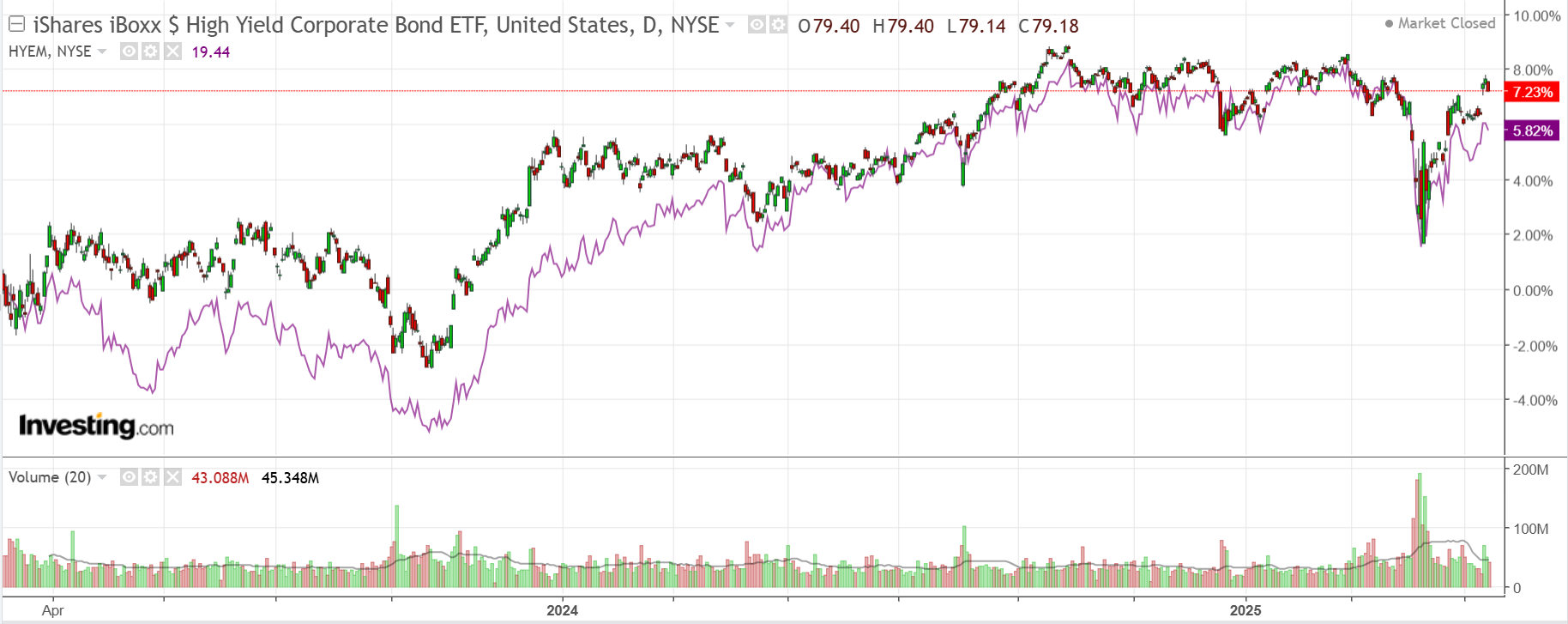

Junk yawn.

Yields are not co-operating.

Stocks short squeeze from hell.

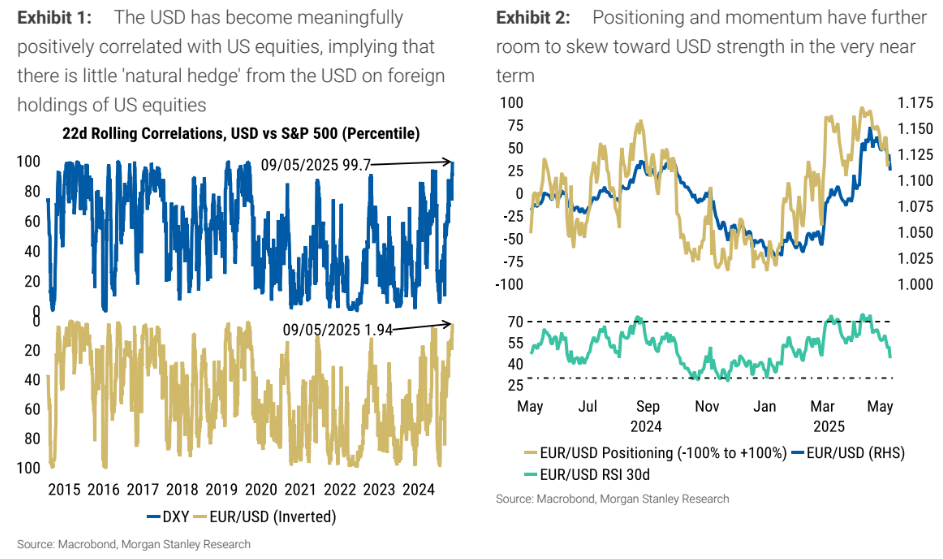

Morgan Stanley has a crack.

This weekend’s US-China trade news has further bolstered the USD’s correction, pushing EUR/USD below our 1.11 re-assessment level.

While the US-China tariff rates have fallen, volatile and uncertain trade policy suggests investors may price in cautious behavior from producers and consumers.

The incentive for foreign US equity holders to FX hedge their investments remains high as the near-term USD-S&P 500 correlation reached near-record positives.

US long-end rate and growth convergence remains an important medium-term theme, and we don’t think investors will stop debating the USD’s safe haven status.

We can’t rule out a further upside USD correction but think current EUR/USD levels are attractive for medium-term investors and hedgers to add long positions.

That sounds reasonable, so long as Europe can get its act together on peace. In that event, yes, EUR could attract a lot more capital based upon better fiscal support and growth.

But Europe still has major problems, not least being its dying car industry.

Despite the dummy spits of the child president, the US is still the world’s productivity and profit epicenter.

So it seems to me that 120 is a long way off and will not be easy to reach.

For AUD, it means more falls while we correct recent over-stretches, but then moderate rises with EUR as the child president’s agenda fails.