DXY took a breather.

AUD bounced.

Lead boots to the moon.

Gold prays it ain’t so.

Metals go for growth.

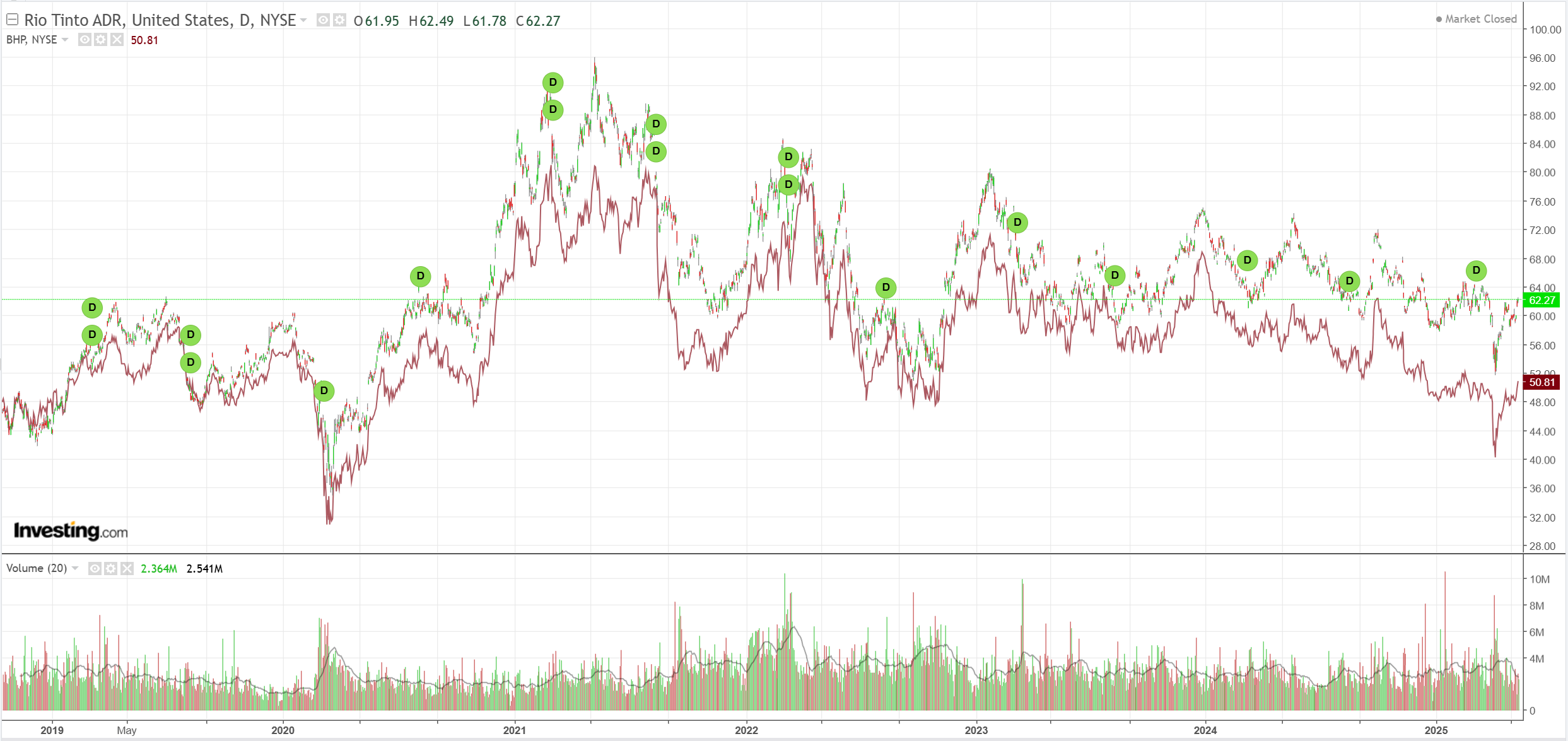

Miners still stuffed.

EM yawn.

Junk says nothing ever happened.

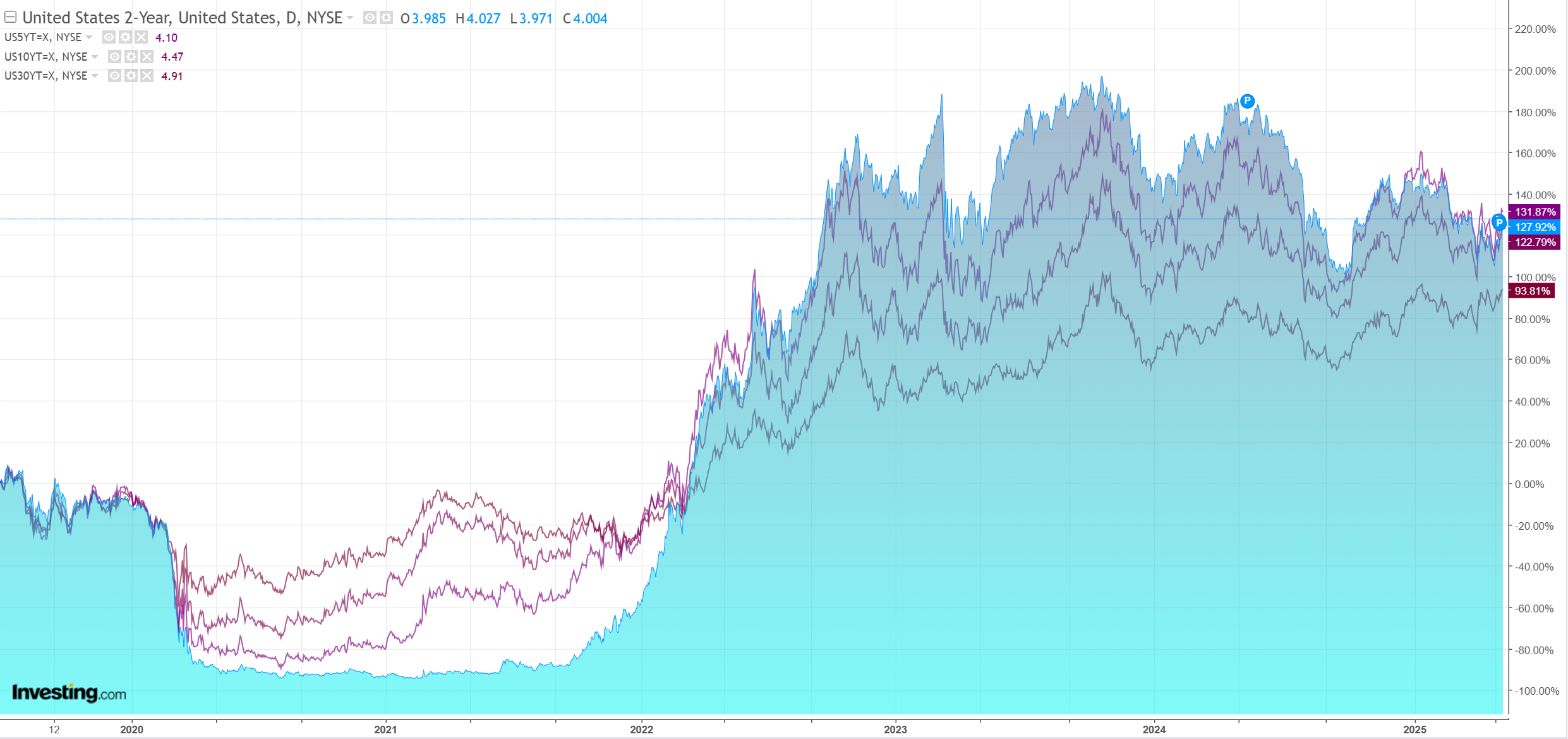

No yield relief.

Stocks only go up.

Wall Street bears are in full retreat. Goldman.

We expect this move to leave the US effective tariff rate increase at +13pp, assuming that likely sectoral tariffs on pharmaceuticals and semiconductors take effect, slightly below our previous assumption of +15pp.

In light of these developments and the meaningful easing in financial conditions over the last month, we are raising our 2025 growth forecast by 0.5pp to 1%Q4/Q4 and reducing our 12-month recession odds to 35%.

I expect absolutely crazy data for the rest of the year as the artificial inventory cycle plays out. First, a growth dive as consumption and inventory volumes plunge with exports, offset by diving imports. Then a surge as consumption and inventory volumes surge with exports, offset by jumping import volumes.

Good luck figuring out how each sector is affected and how that impacts profits.

As for AUD, my base case at this point is probably some slow chop downwards as this Trump-sized pig eases its way through the python.

But that is only if the unfortunate snake isn’t forced to eat another lump of Trump.