DXY wobbling all over.

AUD is stuck but still in a rising channel.

Lead boots are a little lighter.

Oil and gold becalmed.

Metals no bueno.

Mining big bear.

EM meh.

Junk OK.

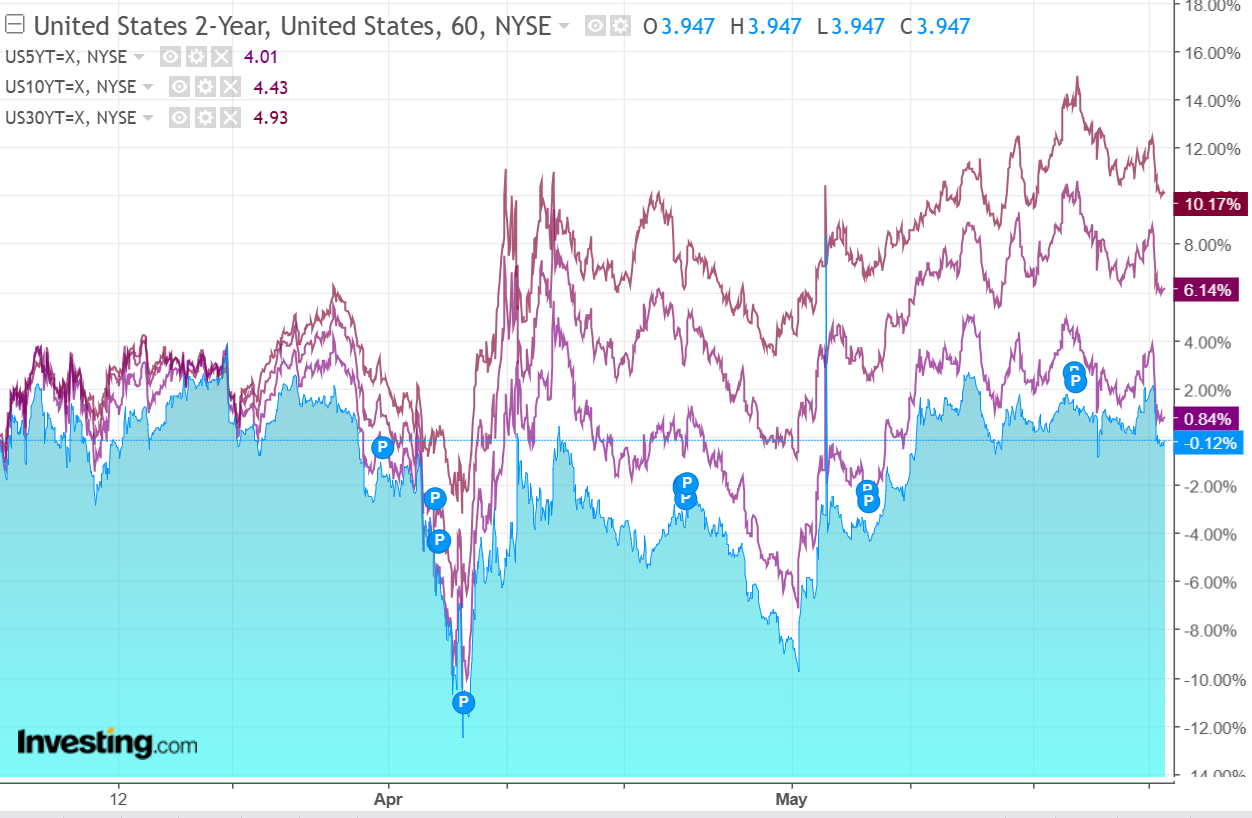

Have yields rolled over?

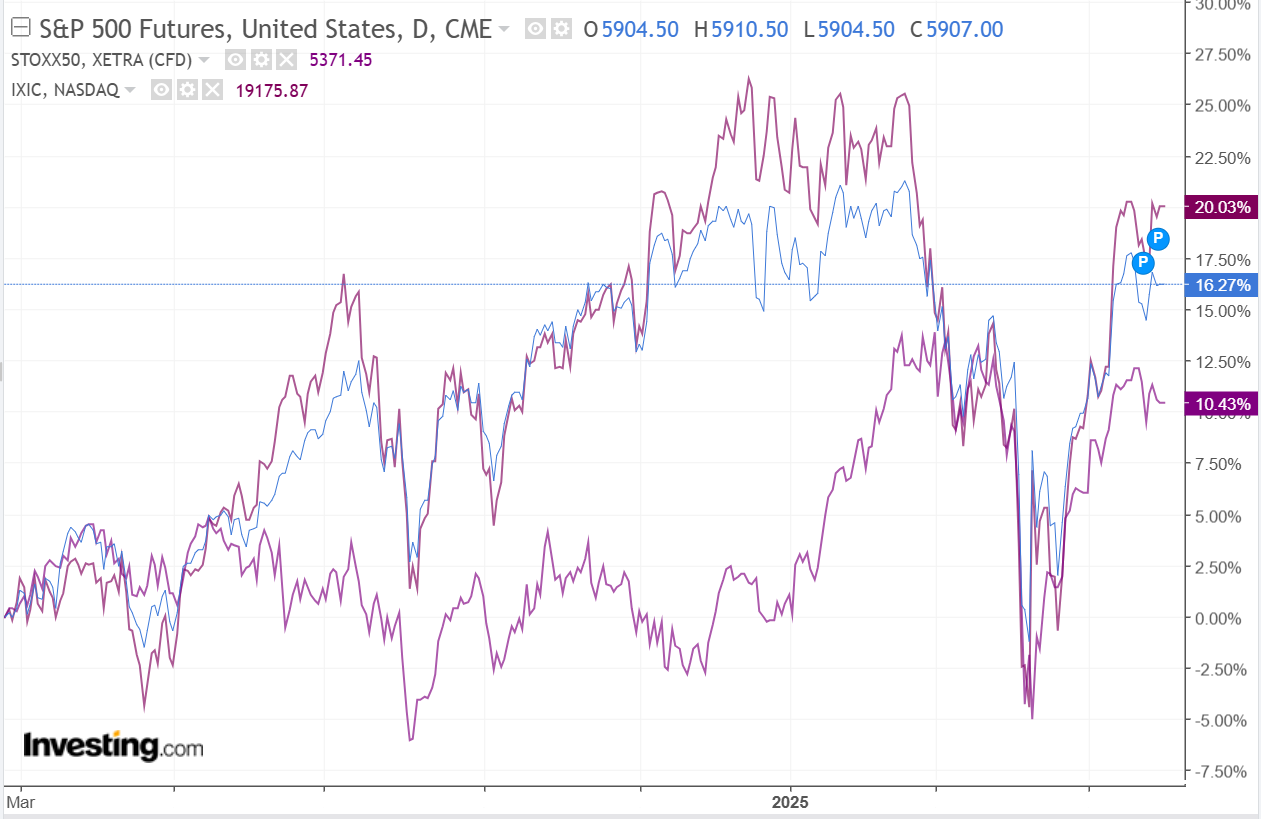

Liberating stocks?

The EUR, and its supposed fiscal underpinnings, is a big story about AUD strength. Credit Agricole.

The ECB will very likely cut its rates by 25bpat its 5 June meeting, setting the deposit rate at 2.00%.Beyond this decision that seems to be rather consensual among the Governing Council, the discussion will likely focus on the next step.

As the ECB is close to its neutral rate–possibly already below it–the question of a pause, or a full stop, in the cutting cycle will likely come under discussion.

In recent weeks, hawkish members, starting with Isabel Schnabel, have started fighting against the dovish market pricing and have opened the debate regarding the end of the cuts.

The update of macroeconomic projections should reassure on the Eurozone economic outlook; at the same time, forecasts for inflation and core inflation could be revised downwardly due to the high level of the EUR, low oil prices and declining wage pressures.

Overall, we believe that the ECB will cut in June and then start signalling a pause for July. We do not expect it to commit beyond that, but the pause suggested for July could help the market to de-price future cuts.

If this were to transpire, with doubts largely around the timing and size of tariffs, it does represent the next up leg for the AUD.

Especially so if we remain in a regime of capital revulsion for US assets, which seems likely.

AUD follows EUR, usually down. But this is the new world order and it may follow it up this time.