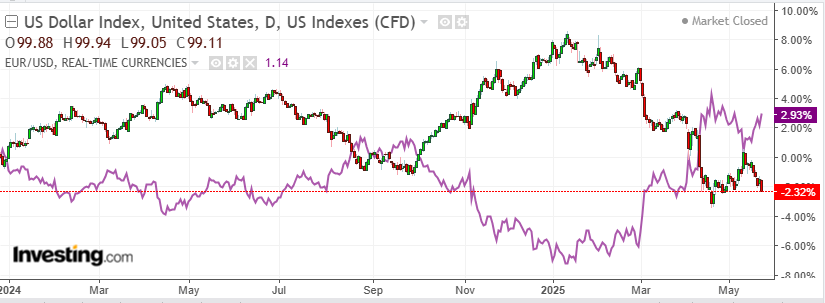

DXy is breaking down again.

AUD looks ready to breakout.

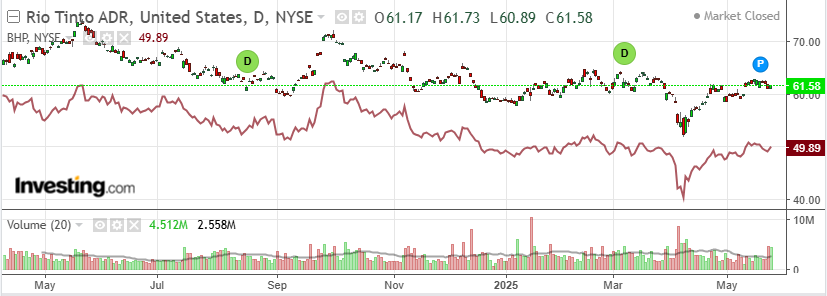

Lead boots plod higher.

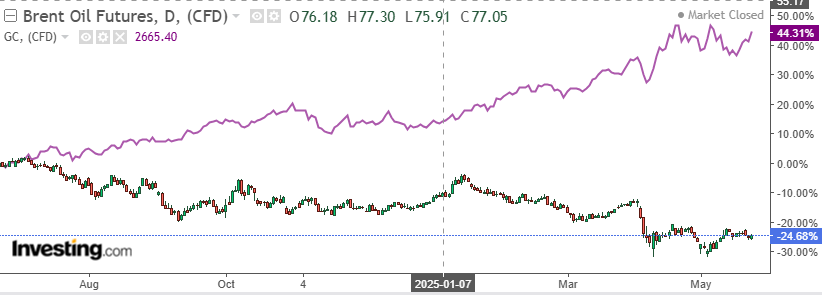

Gold loving DXY, oil nowhere.

Metals also loving the DXY.

Miners not worse.

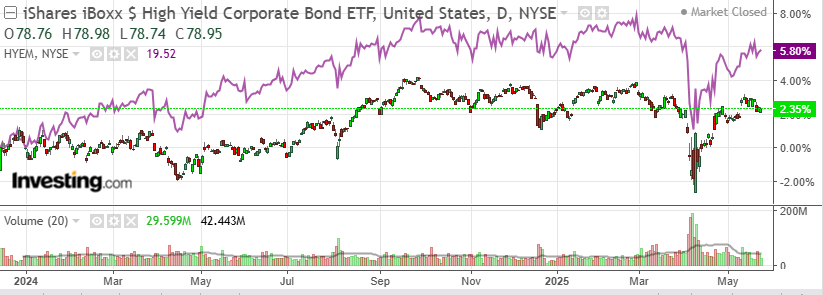

Junk nothing burger.

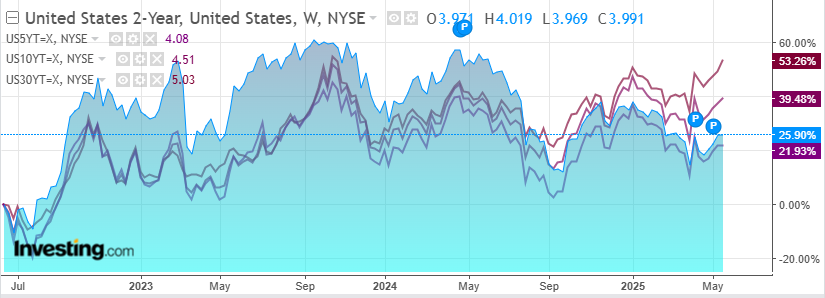

Yields fell on the night but the trend is not your friend.

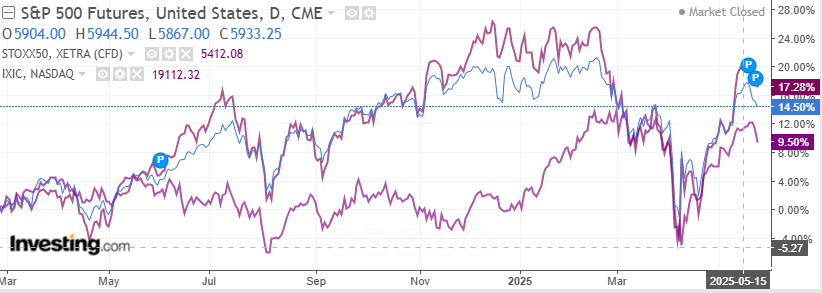

Stocks are not enjoying the regime of the American lira.

Yet the AUD short keeps growing.

Michael Hartnett has a crack.

On that BIG call: government bonds +4%,international stocks +13%, gold +25%; but 30-year US Treasury return-2.5% YTD and investors remain totally sceptical long bonds worth touching (less so International & Gold);we say this is perfectly sensible given “all hat and no cattle” path of US tariff policy (note Trump’s approval rating has also recovered its Liberation Day losses), the “DOGE is out, tax cuts are in”Q2 pivot, investor need to hedge risk“ bubble & boom” policies pursued as politically easiest way to reduce debt as % GDP; but we also say 30-year Treasuries above 5% great entry-point because…“losing the long-end”(and the US dollar) not a winner…>5% bond yields negative for today’s highly “financialized” US economy relative to Rest-of-World, and bond vigilantes incentivized to punish unambiguously unsustainable path of debt &deficit…magic Treasury (5-year) yield number is3¼%, above which the $1.2tn interest payments on US debt grow, below which they stabilize.

I am not a believer in the supply and demand theory of bond prices so I can take this argument.

There is another reason to support it today as well. Goldman.

The Supreme Court granted an emergency request allowing the Trump administration to remove two Federal officials earlier today, but disagreed with arguments that its decision in the case would have implications for removal protections for Federal Reserve officials.

The Court’s decision to preemptively signal that it views the Federal Reserve differently than other government agencies strongly suggests that it is unlikely to grant the President permission to replace governors without “cause”, thereby significantly lowering risks of statutory changes to US monetary policy independence.

That helps US moneyness, especially at the long-end.

However, I don’t think the bond back-up is over yet and economic data is still OK.

Nor am I convinced that the risk of the child president are over.

So I’m still on board for a higher AUD yet.