DXY is making hard work of it.

AUD is ripping your face off now.

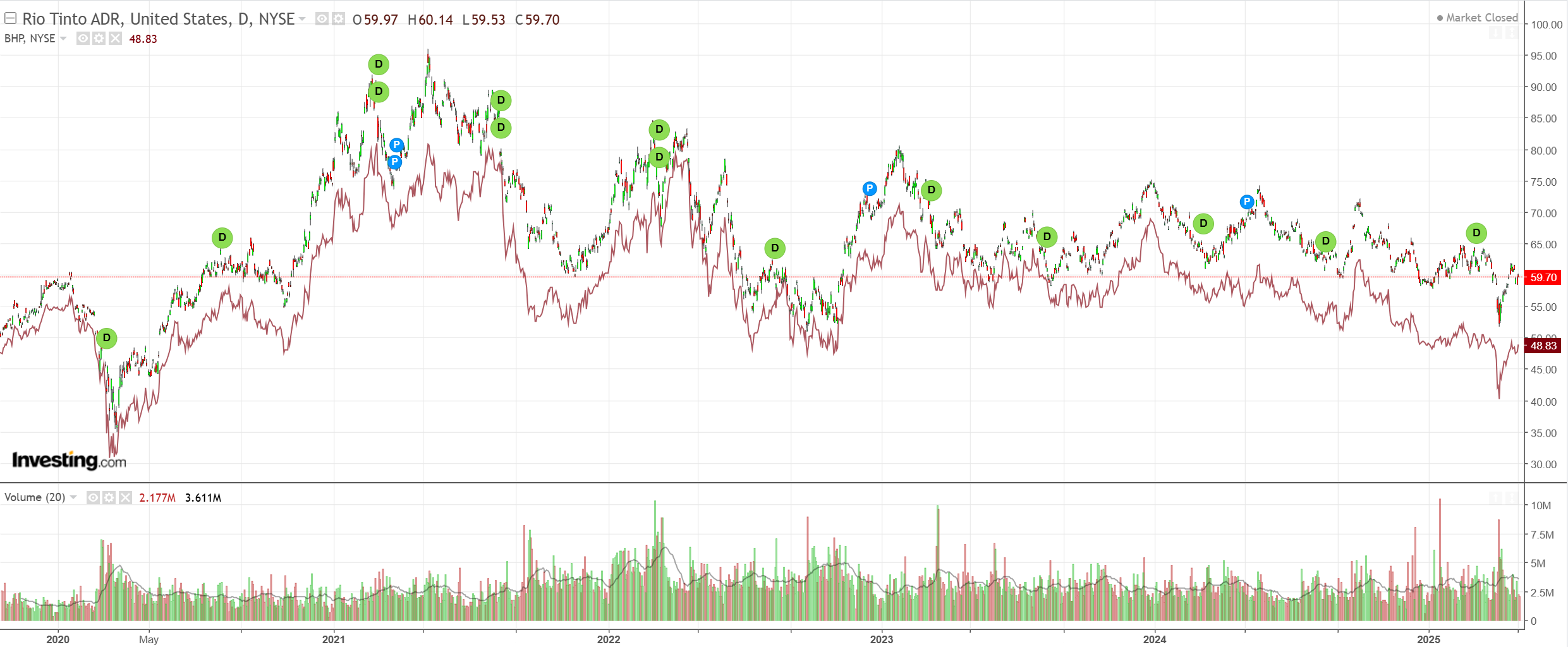

Lead boots will be lead boots.

Oil is about to crater. I will buy a deeper gold pullback.

Metals have no interest in growth.

Miners yuck.

EM gapped into madness.

Junmk says no bueno.

Treasuries are confused.

Stocks are on fire just because.

Goldman wraps the DXY.

USD: EUR hot then you’re cold.

We view this week’s employment report mostly as a reflection of what might have been, rather than a sign of what will be.

Recession watch begins now, and that will mostly dictate the Dollar’s direction over the next few weeks.

Our economists expect that data over the coming months will feature slower spending and higher inflation (Exhibit 1). Our rates strategists have noted that this mix will undermine the relative hedge benefit of Treasuries.

Partly for that reason, it paints a bleak picture for the currency.

Realizing this outcome should weigh on the Dollar’s lofty valuation over time (see below).

That said, as we have previously discussed, it is important to recognize that there have been fundamental drivers to the Dollar’s stabilization in recent weeks; it has not just been a technical or positioning-led move.

In particular, there are signs of some policy recalibration that could alleviate some of the most currency-negative implications.

In addition, data so far have generally reaffirmed that the US economy entered this period with solid momentum.

I’ve got one word to add: oil. The Saudi’s weekend decision to pump is a big DXY negative.

It’s not exactly AUD positive, but it is worse for the US economy than the Australian, especially since lower gas prices boost Aussie activity.

DXY and WTI used to be counter-correlated, but since about 2018, as shale oil grew in importance to US economic activity, the relationship has become correlated.

If oil falls, DXY is going down with it, and AUD will rip your face off going the other way.