A slight exaggeration perhaps, but certainly looser than the always wrong RBA would have you think. Via Goldman.

A key uncertainty in Australia’s monetary policy outlook is whether the labour market is still operating above full employment and therefore a source of inflationary pressures.

In our view, the labour market has arrived at a ‘sweet spot’ and not contributing to inflation, even if indicators such as the unemployment rate remain tight relative to history.

The main argument in favour of a balanced labour market is that wage pressures have already normalised.

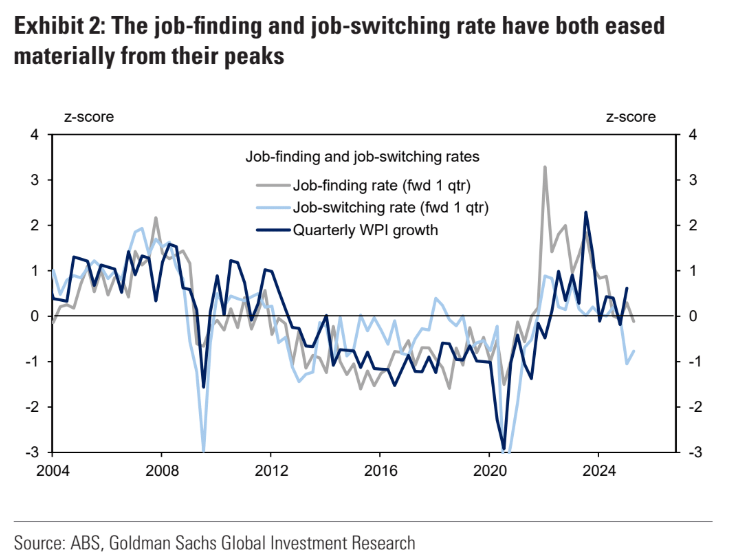

The job-finding rate and job-switching rate, which are important determinants of wage outcomes in theoretical models, have both eased materially.

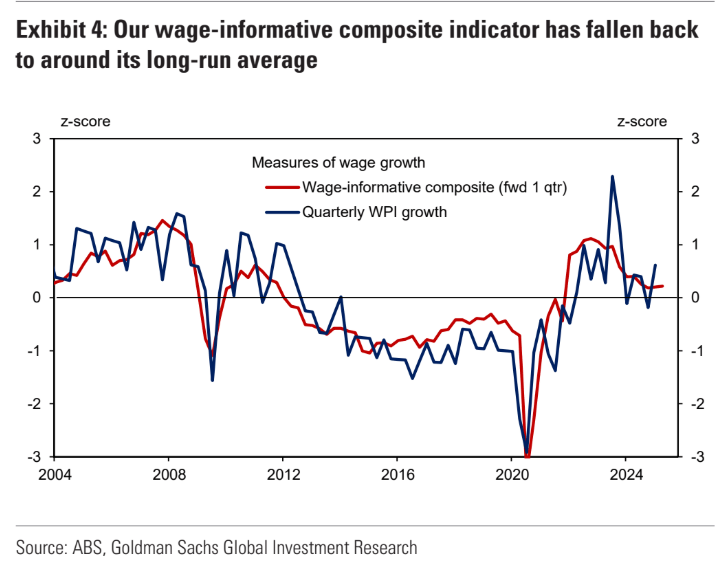

And from an empirical perspective, we estimate the indicators in the RBA’s framework that contain the most informative wage signals have already returned to their historical averages.

Our preferred indicators place the NAIRU around 4.25%, only slightly above the current unemployment rate of 4.1%.

By contrast, the RBA’s model-based estimates of NAIRU are higher and above 4.5%.

We think greater caution is warranted when interpreting these model-based NAIRU estimates because the post-COVID inflation episode has significantly complicated the modeling.

Our assessment of the labour market is consistent with the RBA’s recent dovish pivot to place greater focus on its full employment mandate.

The key risk now is that labour market conditions deteriorate from their currently balanced position –supporting our forecast for three more 25bp cuts to a terminal rate of 3.10%.

As Indians pour in, looser is ahead. Always looser is the reality of the immigration-led labour market expansion growth model.