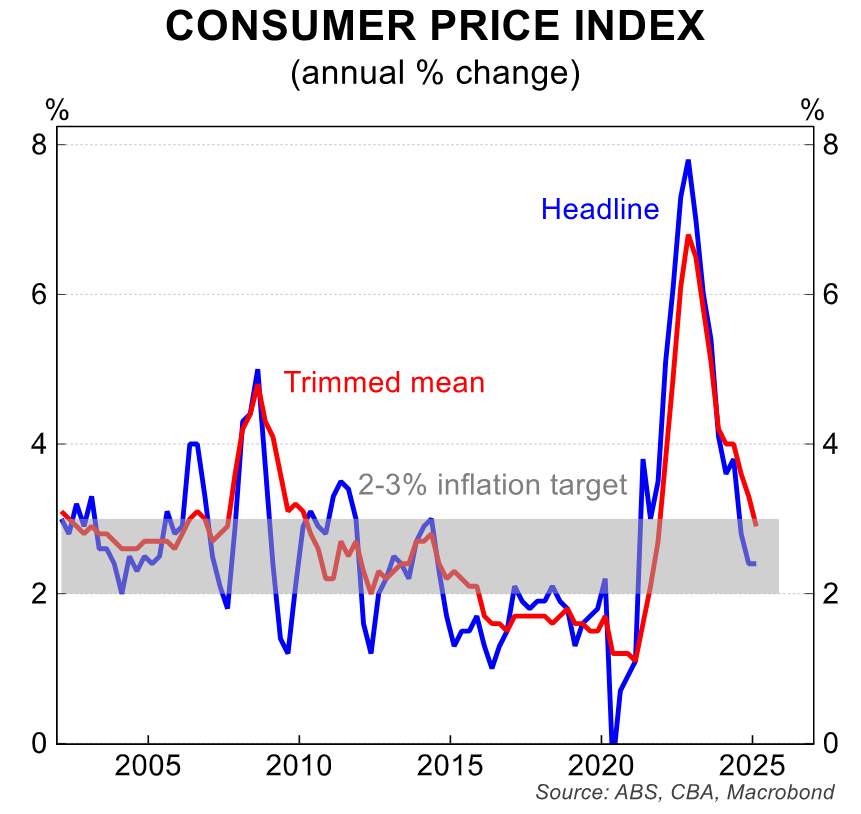

The official Q1 CPI inflation print from the Australian Bureau of Statistics (ABS) revealed that the policy-important trimmed mean inflation fell to 2.9% year-on-year to be within the Reserve Bank of Australia’s (RBA) inflation target of 2% to 3%.

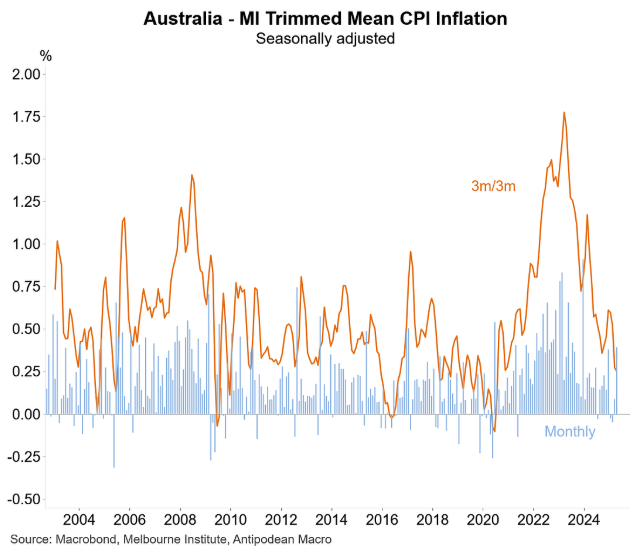

As illustrated below by Justin Fabo from Antipodean Macro, the Melbourne Institute’s monthly trimmed mean inflation gauge rose in April but slowed a little further in quarterly terms:

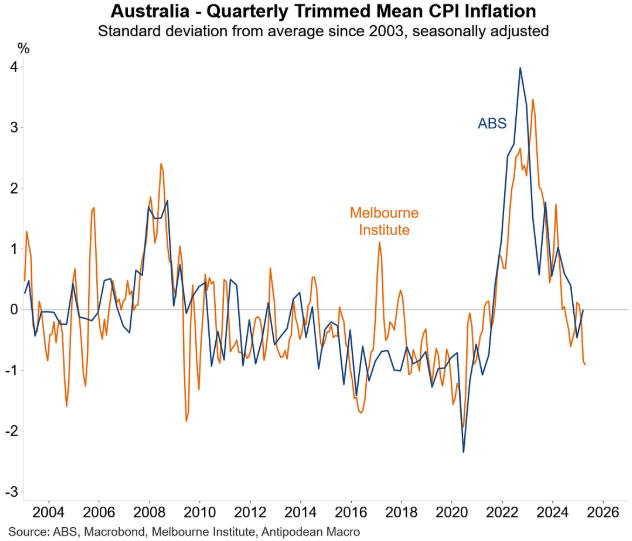

Fabo also shows that the Melbourne Institute’s trimmed mean inflation gauge was comfortably below the long-run average:

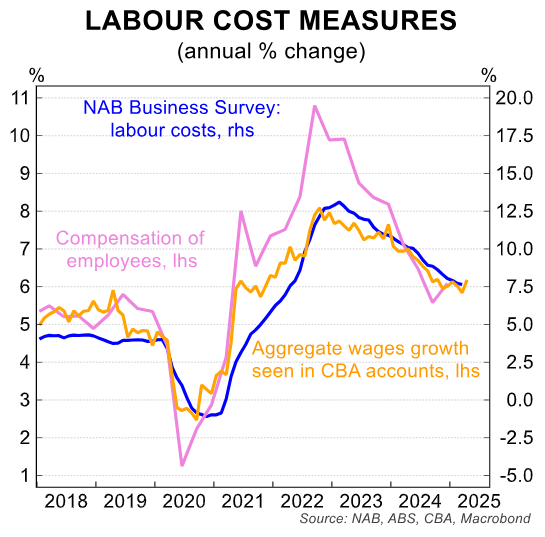

Various labour cost measures, presented below by CBA, continue to point lower:

“For example, aggregate wages growth seen in CBA accounts has stepped down from its late 2022 peaks”, noted CBA senior economist Stephen Wu. “This has closely tracked compensation of employees in the National Accounts”.

“Other indicators of labour costs, such as from the NAB Business Survey, also suggest ongoing moderation”.

Other macroeconomic data released in the past week lean toward rate cuts.

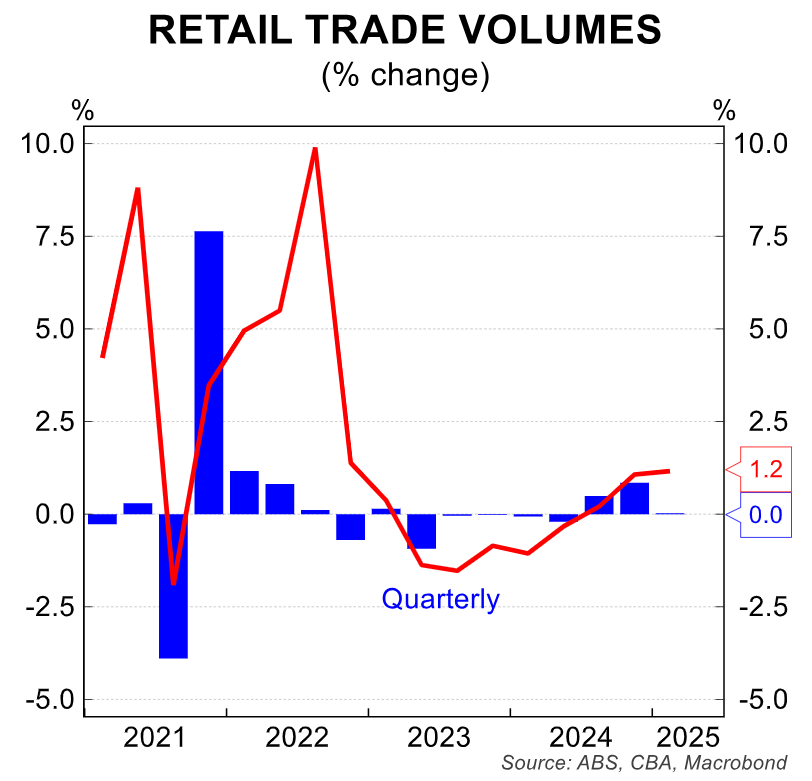

Retail trade volumes were flat in Q1 2025 and fell in per capita terms:

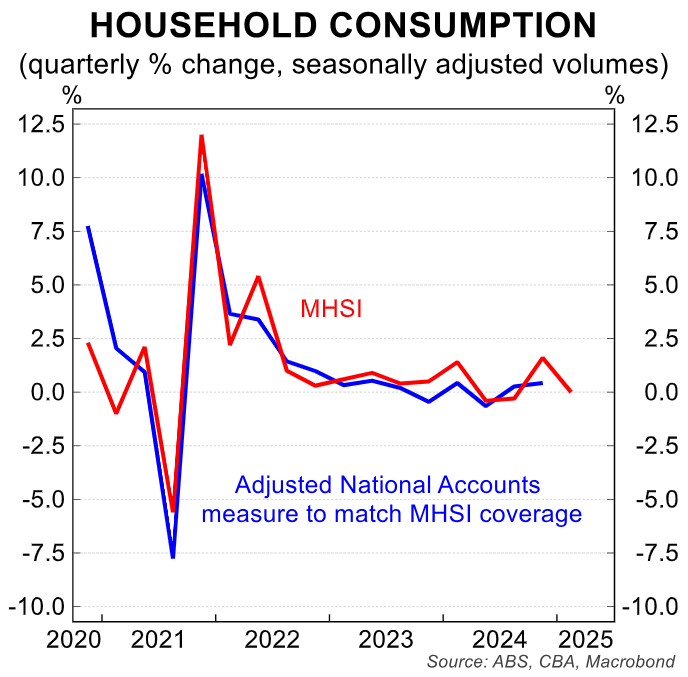

The ABS’ Monthly Household Spending Indicator (MHSI) was also flat in Q1 2025 and fell in per capita terms:

The upshot is that there is little standing in the way of the RBA cutting the official cash rate at its 20 May monetary policy meeting.