Another ‘extend and pretend’ mortgage arrives in Australia

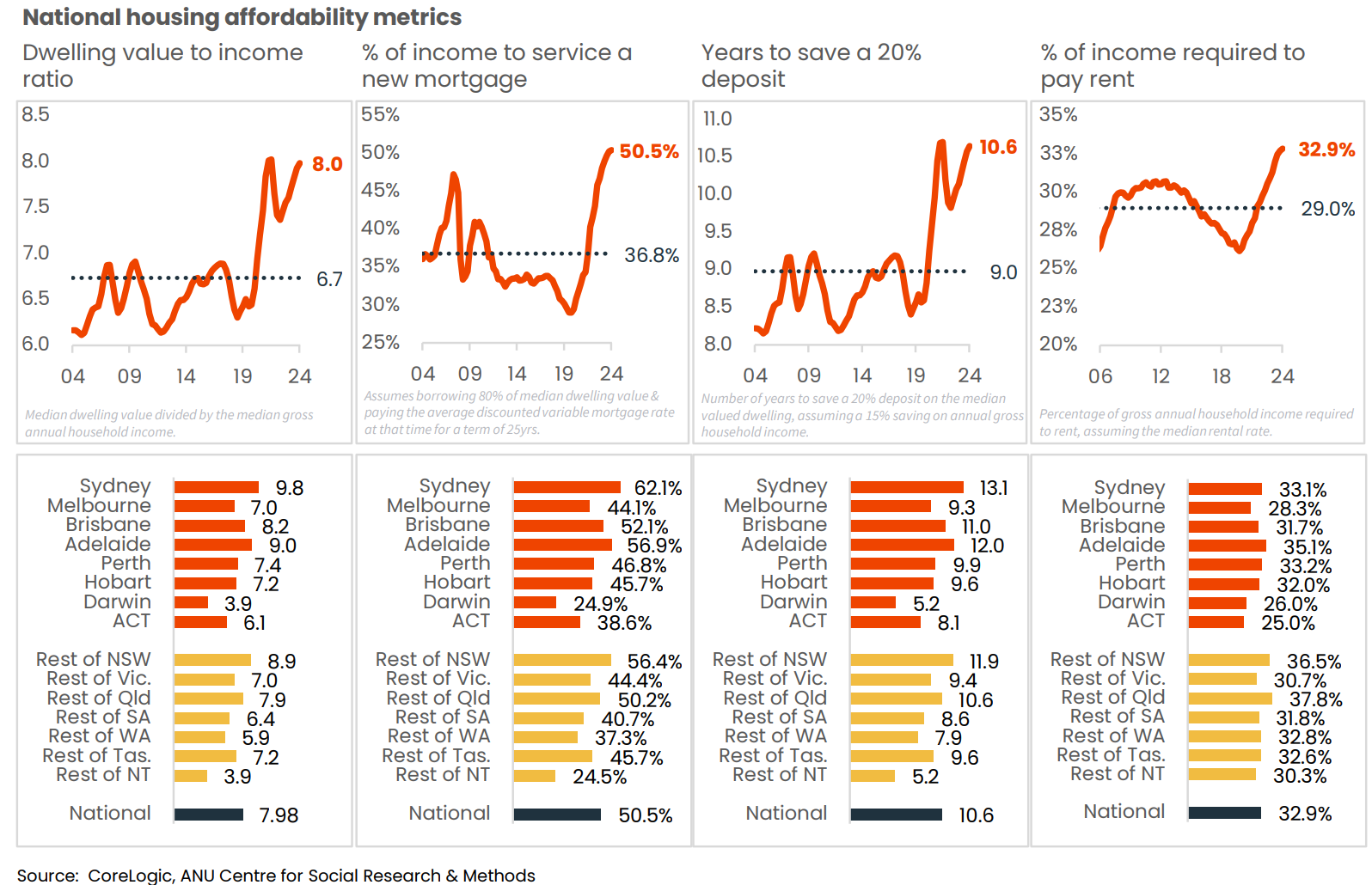

The following graphic from CoreLogic shows Australia’s housing affordability was the worst on record at the end of 2024.

In particular, the dwelling value to income ratio was a record high 8.0 as of 31 December 2024, and the percentage of income required to service a median new mortgage was a record high 50.5%.

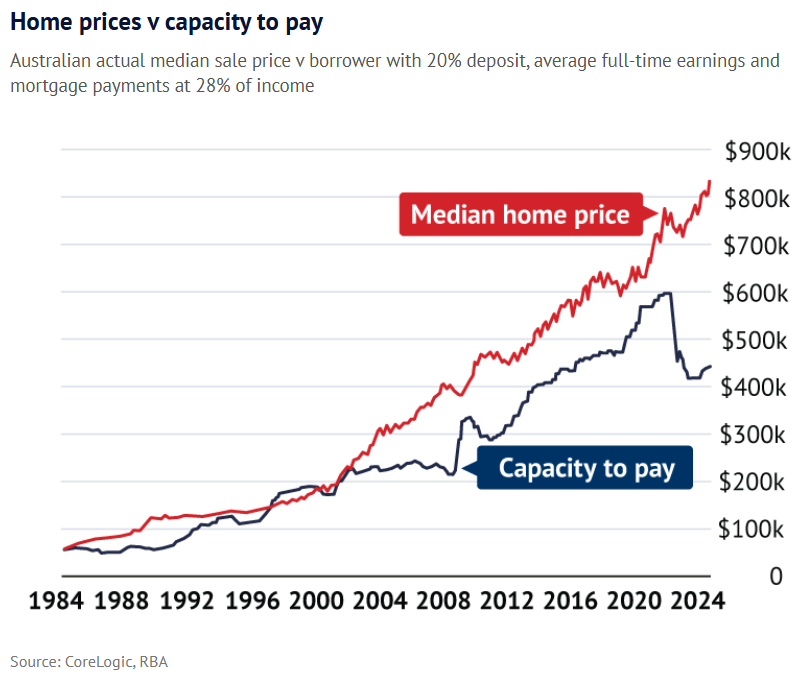

A record gap had formed between borrowing capacity and housing prices before the Reserve Bank of Australia (RBA) cut the interest rate by 0.25% in February.

To artificially bridge this gap, several lenders in Australia have begun offering 40-year mortgages, two of which are solely for first-time home purchasers.

A recent Finder survey also found that nearly one-third of Australian consumers would consider a 40-year mortgage if it reduced their monthly repayments to a more manageable level.

According to Canstar, an individual on a median full-time wage is eligible to borrow up to $24,000 more on a 40-year mortgage than they would on a 30-year term, while a couple working full-time can borrow up to $48,000 more.

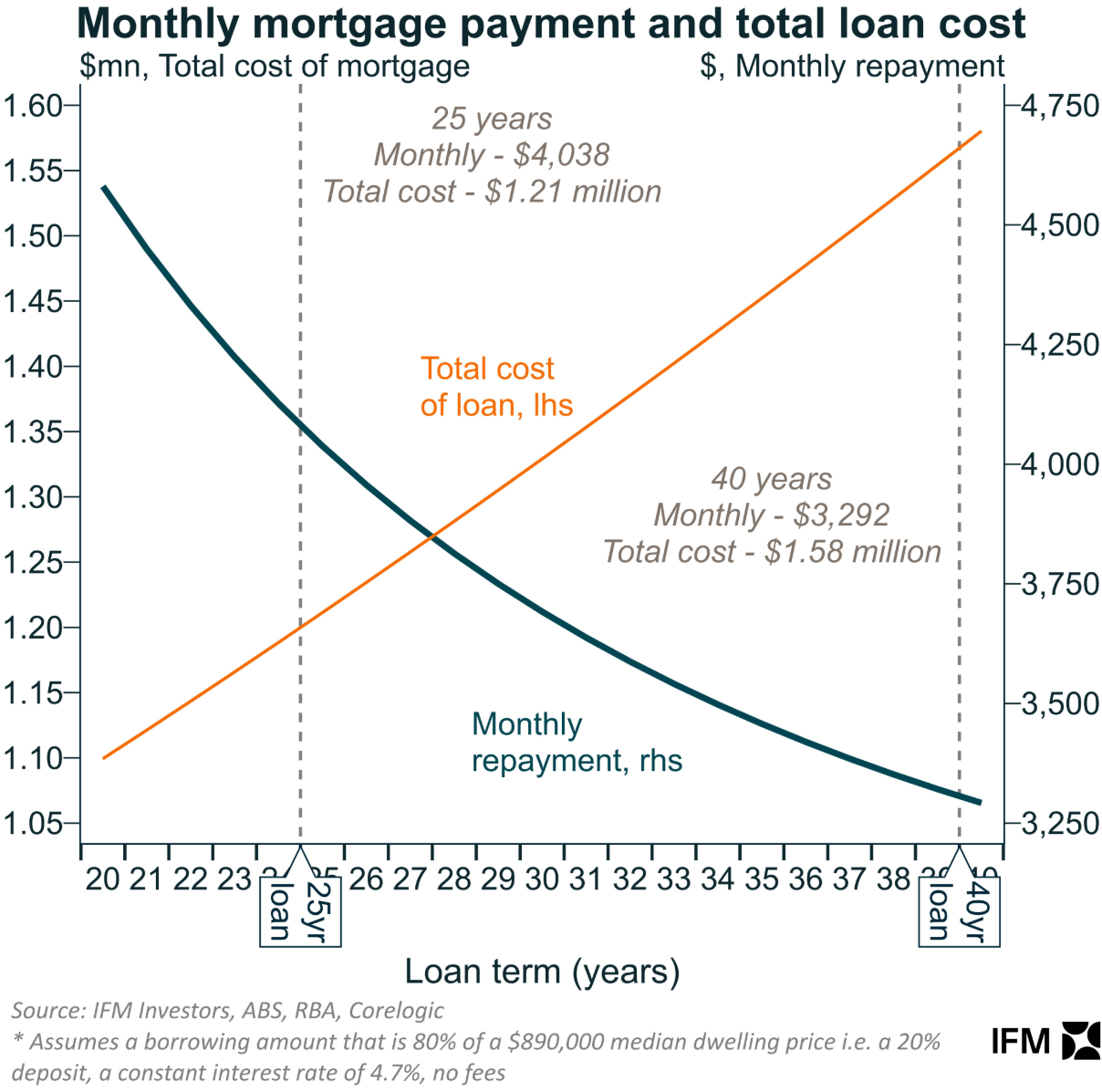

The following chart from Alex Joiner at IFM Investors shows how a lengthier 40-year mortgage term increases borrowing capacity.

Longer loan terms decrease monthly repayments, but total payback costs grow, and more Australians will carry mortgage debt into retirement.

Unbelievably, AMP has now launched “Australia’s first 10-year interest-only home loan with no reassessment”.

We’re excited to announce a new 10-year interest-only home loan offer with no mid-term reassessment, providing customers with more choice, long-term financial flexibility and greater control over cashflow.

Learn more: https://t.co/UV5IDmHI1r pic.twitter.com/m1cmJRmgmU

— AMP (@AMP_AU) May 4, 2025

The new loan is available to eligible borrowers, including retirees, pre-retirees, investors, and owner-occupiers.

AMP cites the following features and benefits:

- 10-year interest-only term: A decade of interest-only repayments, offering long-term cashflow support.

- No mid-term reassessment: Unlike typical products which require reassessment after five years, the loan provides greater certainty and stability for the full interest-only term.

- Flexible eligibility: Available to a wide range of borrowers, including retirees, pre-retirees, self-employed individuals, owner-occupiers, investors, and rent-vestors.

- Financial confidence: Enables longer-term strategic financial planning, whether it’s unlocking home equity in retirement or supporting investment goals in earlier life stages.

- Quality of life in retirement: Helps older Australians retain equity in their home, remain in their home, while unlocking cashflow to improve quality of life.

- Empowers younger buyers: Provides an alternative pathway into the property market, particularly for younger Australians through rent-vesting strategies.

- Simplified administration: Reduces paperwork and ongoing reassessment burdens, especially helpful for those with non-traditional income sources.

The reality is that this type of mortgage product will increase borrowing capacity, household debt, and ultimately home prices.

It will pour more mortgage fuel on the housing bonfire and is ultimately retrograde from a financial stability and affordability perspective.

Sure, interest-only loans are a wonderful analgesic for cash flow pains, but the pain is only deferred and never actually goes away.

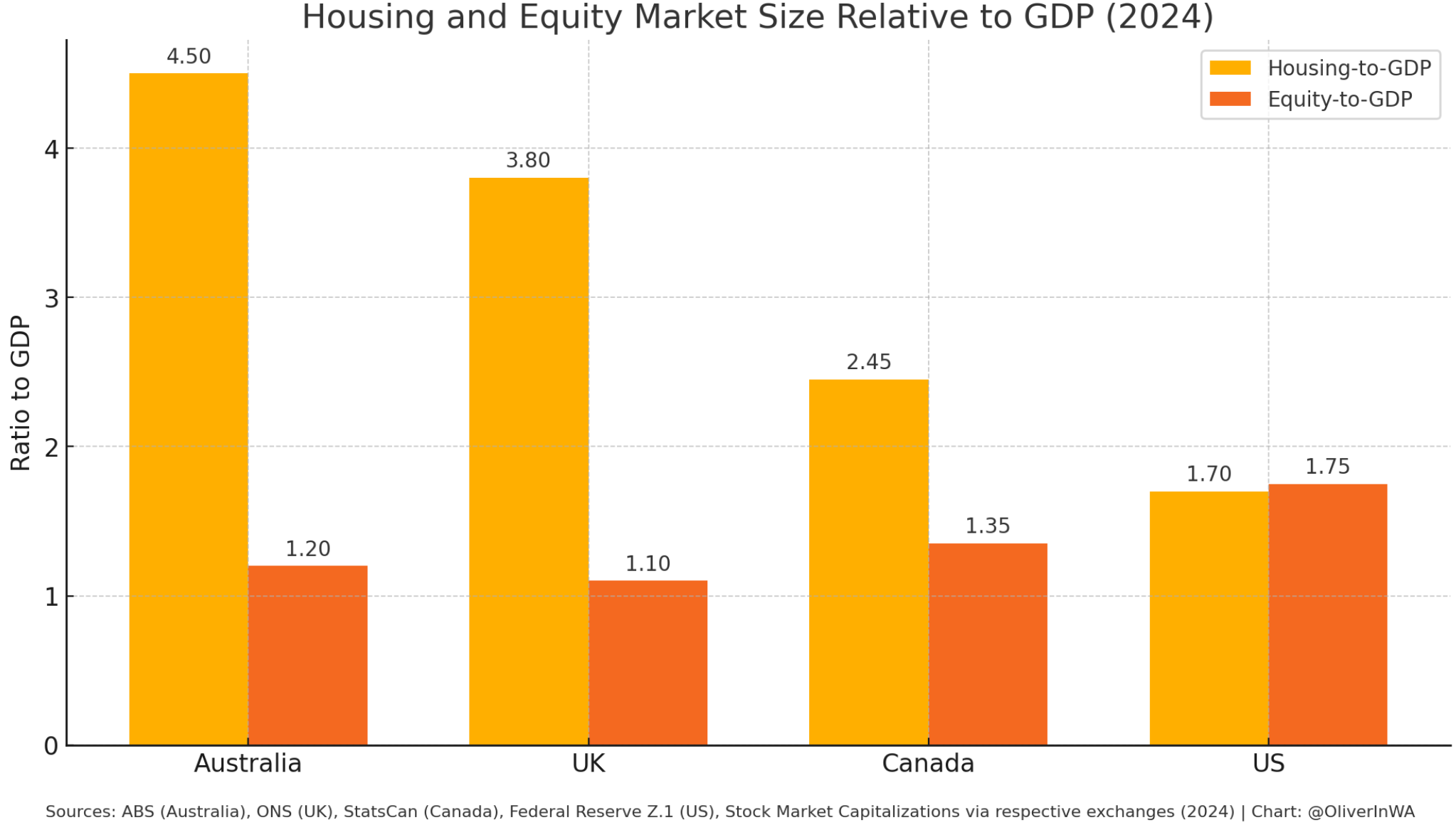

Australia already has one of the most expensive housing markets in the world relative to our economy and household incomes. Demand-side mortgage measures like these will merely drive more financial capital into housing, inflating home values further.

Extending mortgage terms and offering 10-year interest-only mortgages are additional attempts to boost housing demand and initiate a new price boom.

Allowing households to borrow more for their homes would achieve the same thing it usually does: increase debt levels and long-term housing costs.

This century has supplied abundant empirical evidence for how the story will conclude. House prices and debt will be pushed to new heights.

These new mortgage products also come amid the Albanese government’s promised state-sponsored subprime mortgage scheme, which will enable all first-time home buyers to purchase a home with only a 5% deposit, with the government (taxpayers) guaranteeing 15% of the borrowers’ loans.

Labor has also directed mortgage lenders to exclude student debt in their mortgage serviceability evaluations.

The inevitable outcome of these policies will be more borrowing, higher household debt, and higher home prices.

The stars are, therefore, aligning for a blow-off bubble in Australian home prices.