Global bond yield suppression has been a constantly favourable backdrop for equity investors since the 2008 Global Financial Crisis.

Every attempt to withdraw support has led to the financial markets convulsing until policy makers are forced to U-turn.

So what should we make of recent tumultuous events in Japan?

I have always exhorted clients to keep a close eye on Japan. Major financial events often happen first in Japan, for example the late-1990s tech bubble bursting first in Japan.

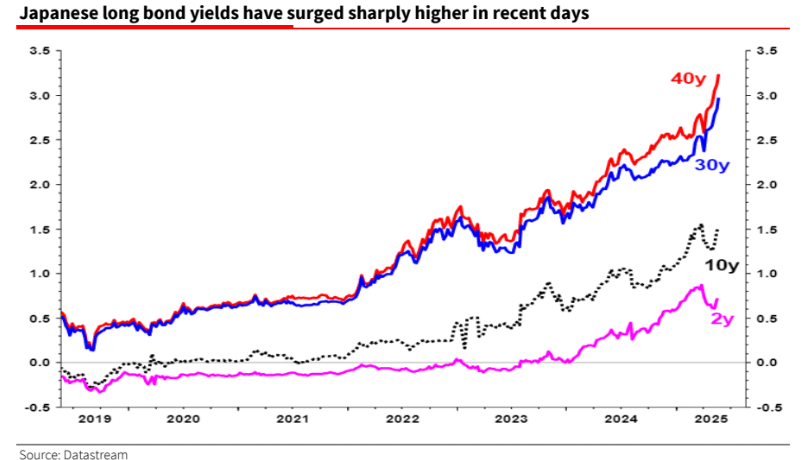

So what should we make of the recent explosive rise in Japanese long bond yields (see chart below)?I endorse the comment from “End Game Macro” on X (formally Twitter) who wrote, “The cracks in global bond markets just turned into fractures. Japan’s 20-year government bond (JGB) auction was the worst since 1987. Bid-to-cover ratios collapsed. Yields on the 30-year spiked to 3.12%, and the 40-year hit an all-time record. This isn’t a one-off technical failure it’s the first sovereign domino tipping over in a structure that’s held the global system together for decades.”

The author continues, “Japan’s bond market isn’t isolated. It’s the keystone of global yield suppression. For years, Japanese institutions propped up the global bond market through the yen-funded carry trade and massive foreign bond purchases especially U.S.Treasuries. That era is ending in real time. The BOJ is losing control of the long end of its curve. And with FX-hedged returns on Treasuries now deeply negative, capital is being pulled home….This is the regime shift. The sovereign bond repression model where rates are low, inflation is ignored, and balance sheets absorb unlimited debt is breaking. Japan’s failure is the signal. The U.S. response will define the consequences. The sequencing matters. Don’t get it backwards. Japan’s bond market may be the fuse, but the US is the [ticking fiscal] time-bomb.”

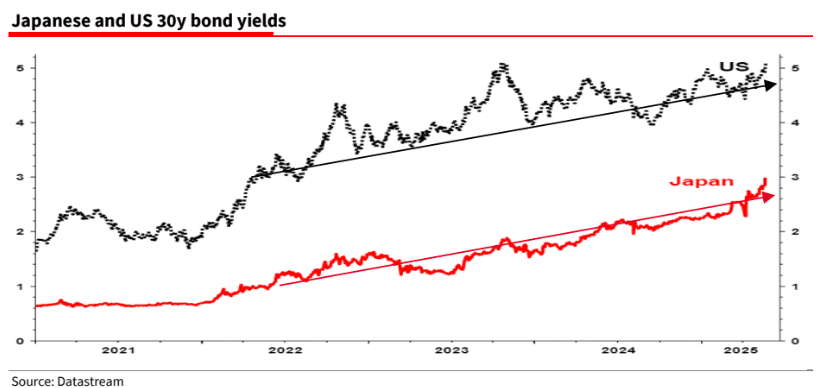

And therein lies the problem for global investors. Most commentators attribute the rise in US 30y yield to 5% to US domestic fiscal developments without putting it into a wider global context. Both the US treasury and equity markets are vulnerable, having been inflated by Japanese flows of funds (as has the dollar). And,if sharply higher JGB yields entice Japanese investors to return home, the unwinding of the carry trade could cause a loud sucking sound in US financial assets. Hence, I would rank trying to understandand follow the surging long end of the JGB market as then umber 1 most important thing for investors at the moment.

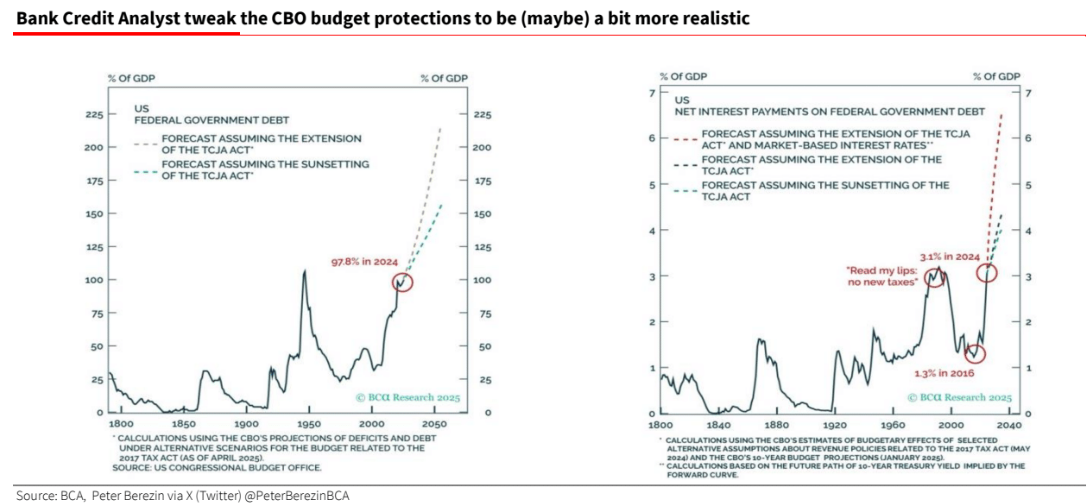

The US bond vigilantes are getting anxious and for good reason. Peter Berezinat the Bank Credit Analyst posted this great chart showing just how bad the US debt situation really is, especially if you use market interest rates. No wonder US30y yields are now above 5%.

This awful US fiscal situation (above) is the ticking time-bomb that End Game Macro alludes to. Bond vigilantes are rightly getting anxious and sharply rising 30y JGByields ain’t helping.

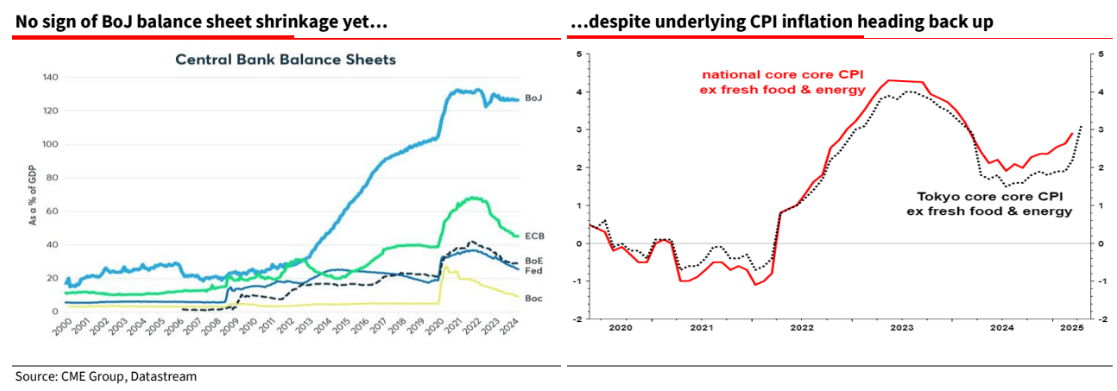

Let’s remind ourselves just how ‘off the scale’ the BoJ’s QE has been (left hand chart below). And the mounting signs that Japan has exited its deflationary quagmire (right hand chart) is putting more pressure on the BoJ to raise rates and shrink its bloated balance sheet.

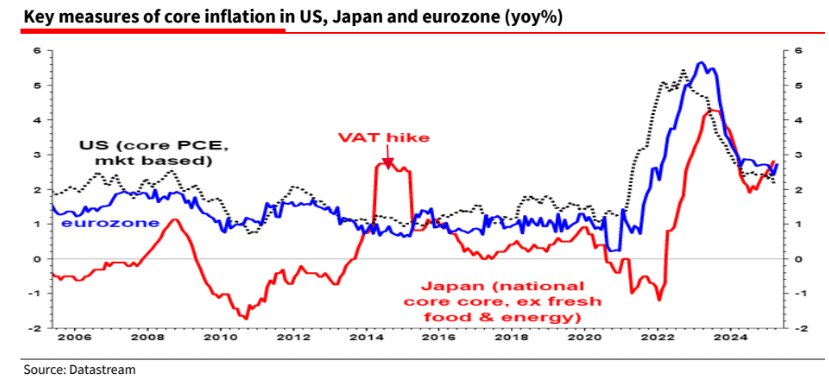

Japanese core CPI inflation (or core, core as they like to call it) is now higher than it is in the US or eurozone. No wonder there is upward pressure on their bond yields

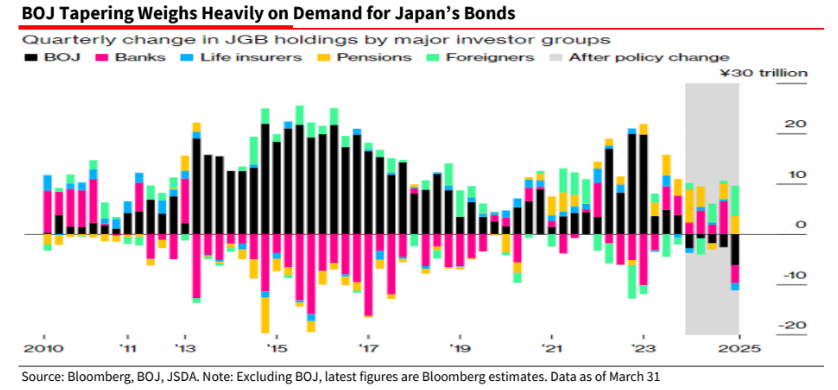

Bloomberg notes in an article that even the BoJ’s current moderate taper of QE has resulted in a hole in JGB demand. Given the size of the deficit, there is a lot to digest and so yields will rise.

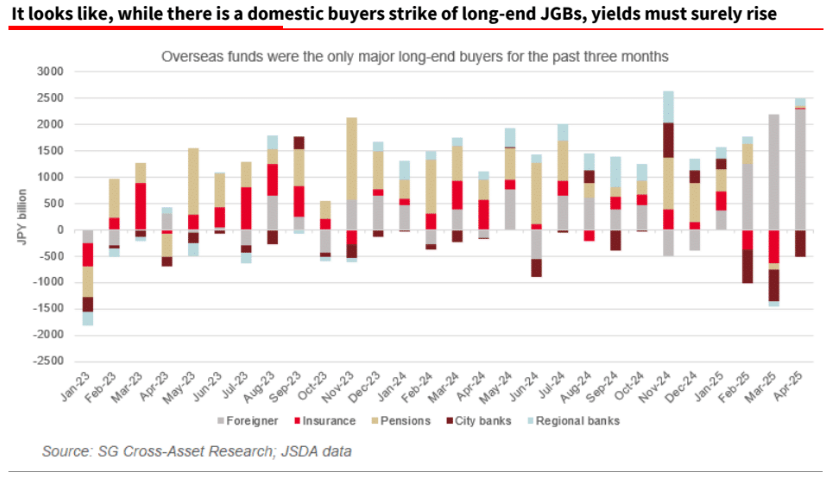

And our own Stephen Spratt notes that buying of long-end JGBs was entirely driven by foreign buyers in recent months. I think EndGame Macro has it right–if like us you believe BoJ QE has been pivotal to US bubble equity valuations, then the ongoing JGB rout is a game changer.