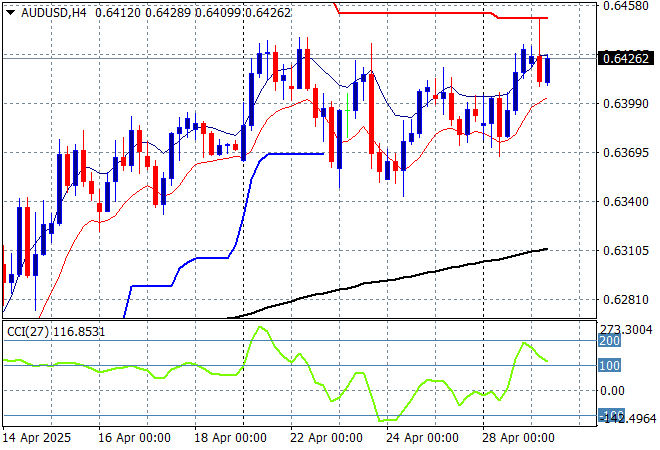

Risk markets are trying to digest quite a bit of macro news today with the Canadian election resulting in a Liberal victory, while a small reprieve in auto tariffs by the Trump regime looks possible amid the UK/EU announcing what could be a reversal in post Brexit trade barriers. The USD is back on the back foot against most undollars as the Australian dollar tries hard to lift further above the 64 cent level this afternoon.

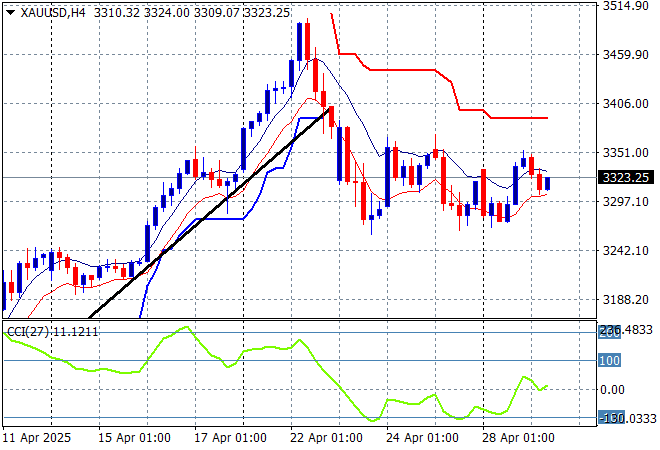

Oil markets are failing to stabilise with Brent crude now sliding down to the $64USD per barrel level while gold is trying to fight back with a slight rebound back above the $3300USD per ounce level:

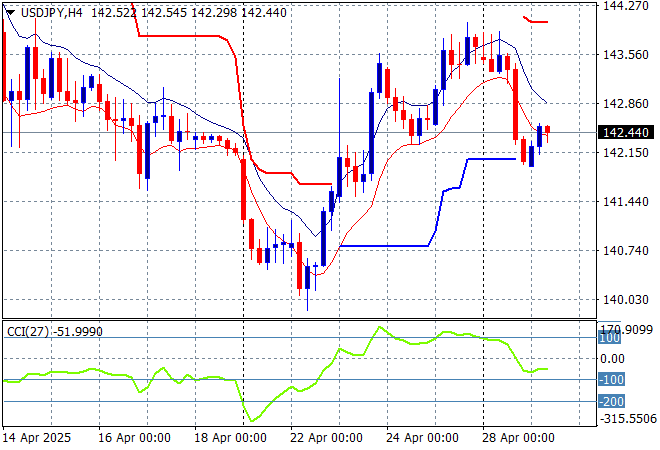

Mainland Chinese share markets are slightly lower going into afternoon trade with the Shanghai Composite retreating below the 3300 point level while the Hang Seng Index has pulled back slightly to remain above the 22000 point level. Japanese stock markets are having yet another holiday while trading in the USDPY pair has been muted as it tries to hold above the 142 level:

Australian stocks have managed a very solid session with the ASX200 up nearly 1% at 8070 points while the Australian dollar is holding just above the 64 handle as it thinks about another small breakout before this weekend’s election:

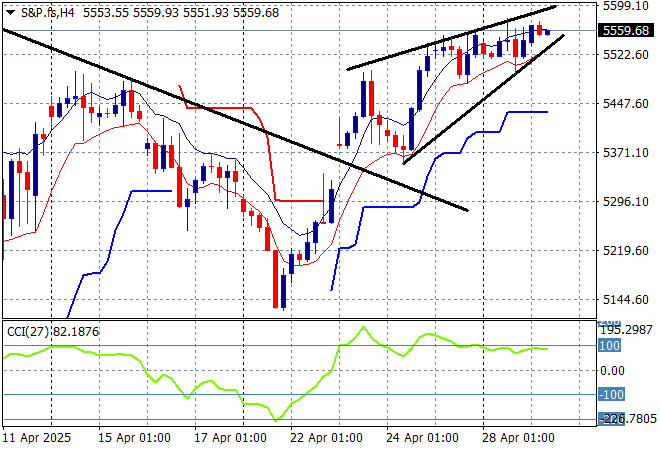

S&P and Eurostoxx futures are sliding back a little going into the London session although the auto tariff reprieve might help lift spirits with the S&P500 four hourly chart showing a bearish rising wedge pattern here at the 5500 point level:

The economic calendar is relatively quiet as we move into end of month and of course, US non farm payroll territory.