More positive news for RBA and inflation

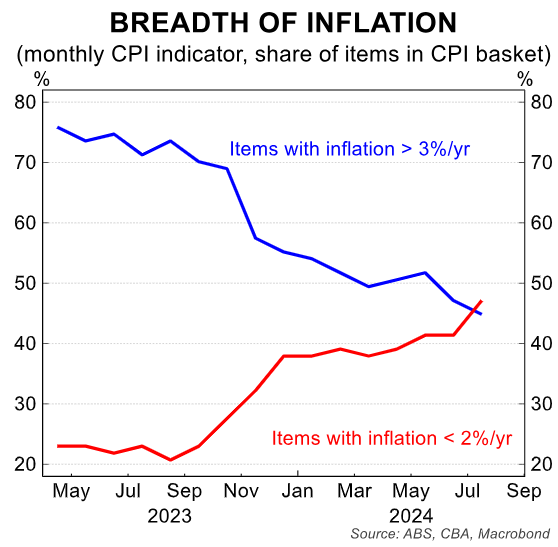

The July monthly inflation indicator from the ABS showed that the disinflationary impulse had broadened.

The number of items in the CPI basket with annual inflation below 2% rose above the number of items with prices growing faster than the RBA’s inflation target of 3%:

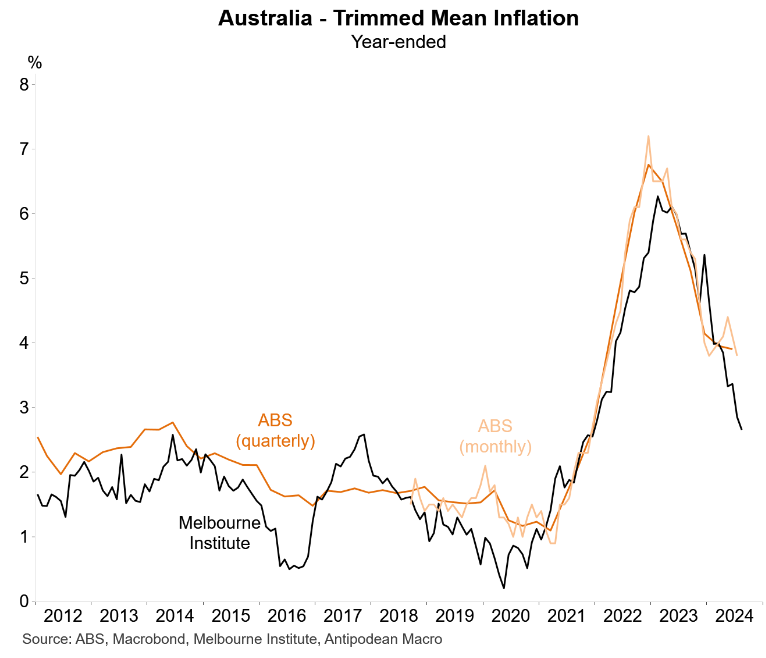

Last week, the Melbourne Institute inflation gauge recorded a sharp fall in trimmed mean inflation:

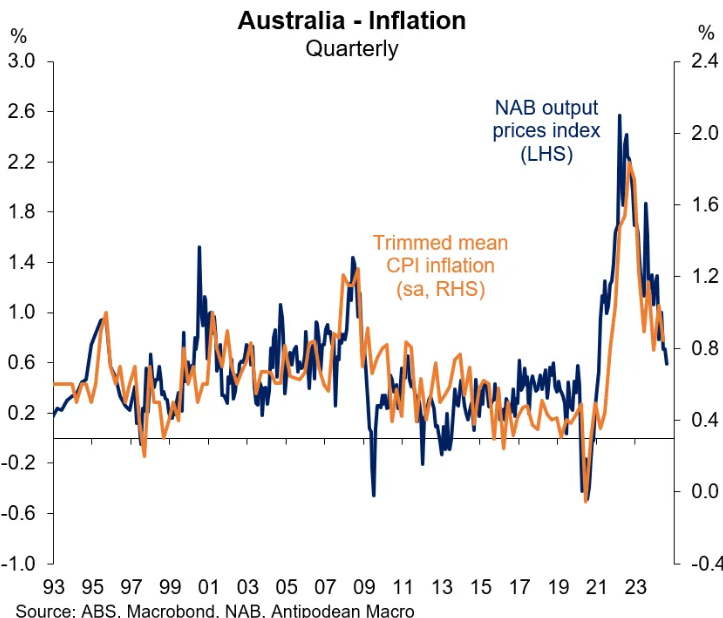

On Tuesday, the NAB business survey was released. As shown below by Justin Fabo at Antipodean Macro, output prices further declined in August, pointing to a further moderation in trimmed mean inflation:

Although the decline in CPI inflation has been slow and bumpy, progress is being made.

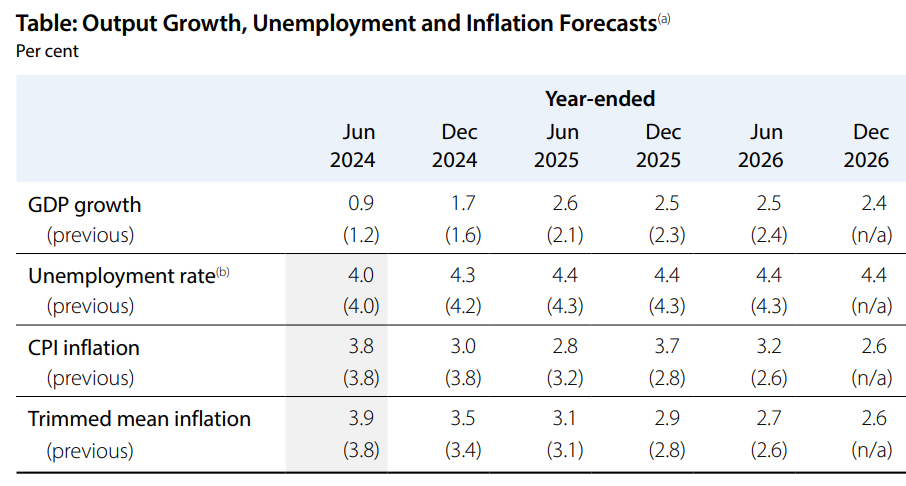

That said, I still believe that the RBA would need to see the official unemployment rate tick up toward 4.5% before it commences its next rate-cutting cycle.

The latest Statement of Monetary Policy projected that Australia’s unemployment rate would be 4.3% by year’s end, versus 4.2% currently:

The RBA would likely need to see the unemployment rate rise materially above its forecast to compel it to cut rates before the end of the year.