What other conclusion can we draw from this chart?

Going forward, relatively low sales volumes and new housing supply are likely to support prices and average loan sizes. Improving consumer sentiment following the Stage 3 tax cuts and the reduced possibly of an RBA rate hike should also support price growth and average loan sizes.

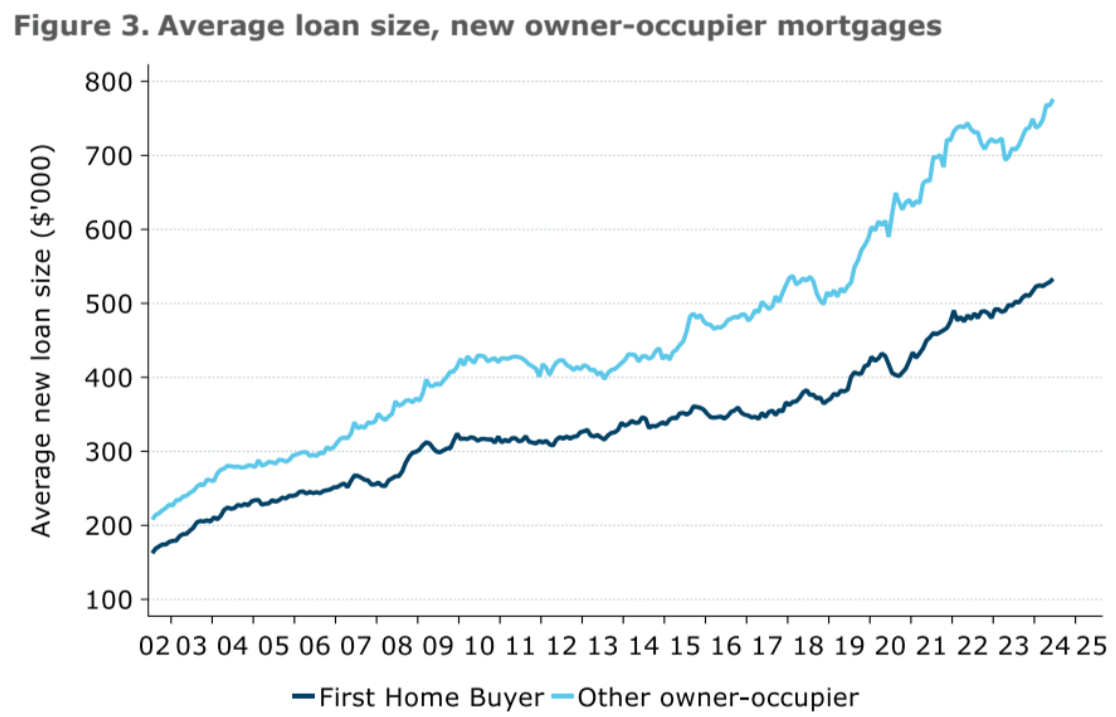

The post-2019 accelerated pace of rising mortgage sizes is the most amazing feature:

- loose immigration, falling rates, tight fiscal equals bigger mortgages.

- loose immigration, rising rates, loose fiscal equals bigger mortgages.

The two decent periods of correction have been in the circumstances of:

Advertisement

- post-GFC tight immigration, loose rates, and loose fiscal.

- COVID period, tight immigration, loose rates, and loose fiscal.

- (2018 is the Banking Royal Commission).

The only time Australians put a brake on their mortgage binge is when immigration falls.

And that is why population growth continues.

Advertisement