So says the parliamentary report:

The inquiry arose from concerns that some liquified natural gas (LNG) producers will not meet their domestic gas commitments under the WA Domestic Gas Policy by the time the gas projects reach end-of-field life. A concurrent concern was forecasting indicating that WA may experience shortfalls of gas almost every year until 2033.

WA faces increasing demand for gas and declining supply. Demand is expected to rise over the next decade. The Committee believes WA will need gas for decades to come, although exactly how much and over what timeframe is yet to be seen.

From 2030 onwards the forecasted supply deficit is concerning. By 2032 the domestic gas shortfall is forecast to exceed 350 TJ/day—a substantial amount which according to current forecasts will continue to increase year on year.

Since tabling its Interim Report in February, the Committee has seen evidence of a much-welcomed industry response. It appears that the State may now avoid shortfalls of gas in 2024 and 2025. Producers that were previously lagging in the delivery of domestic gas volumes have now improved the rates at which they are supplying the domestic market.

However, relying on sporadic appeals for more gas when shortfalls are imminent is not a viable strategy for the management of domestic gas supply. The terms of some existing domestic gas agreements are not robust enough to guarantee that producers will always meet their commitments to the domestic market in a timely manner.

The report makes recommendations to the State Government about how it can improve the operation of the Policy. These include enacting a new domestic gas security policy within a legislative framework and improving the terms of domestic gas agreements where necessary.

Well done WA. Smash the cartel.

Meanwhile, in the East:

Falling production at one of the country’s largest gas plants and a forecast slide in supply from fields off the south-eastern coast is making increasingly inevitable what had been dismissed as unlikely development only a few years ago: the need to import LNG.

The market operator has warned for months of looming shortfalls in gas – used in everything from manufacturing to heating homes – and fears of supply problems have spread beyond the major energy retailers. Other major companies examining the possibility of importing LNG now include Snowy Hydro, Woodside Energy, Shell and industrial users, including explosives manufacturer Orica and steel producer BlueScope.

“Everyone is looking but no one is committing … there are still no customers willing to lock in import-parity prices,” said MST Marquee energy analyst Saul Kavonic. “We may need to see a severe gas shortage event for someone to finally sign up for imports.”

…One major impediment to importing gas, however, is the price. At current spot LNG pricing, imports would cost $20 a gigajoule, over 30 per cent more than domestic prices.

…Frank Calabria, the chief executive of Origin Energy, said he believed that LNG imports would play “a major role” in maintaining gas supplies.

…Origin is regarded as a prime candidate to sign up for LNG imports, despite walking away this year from talks with aspiring South Australian LNG import terminal developer Venice Energy to use the company’s proposed facility in Port Adelaide.

Nobody is signing up because it is insane.

Why would we import gas, which will become the marginal price-setter, exposing the economy to the kinds of regular price shocks seen Europe, when we could just reserve a small volume of exports and pay local production costs?

Why would we let Origin import gas when it is a key player inside the gas export cartel? It will drip-feed the supply at whatever price it likes.

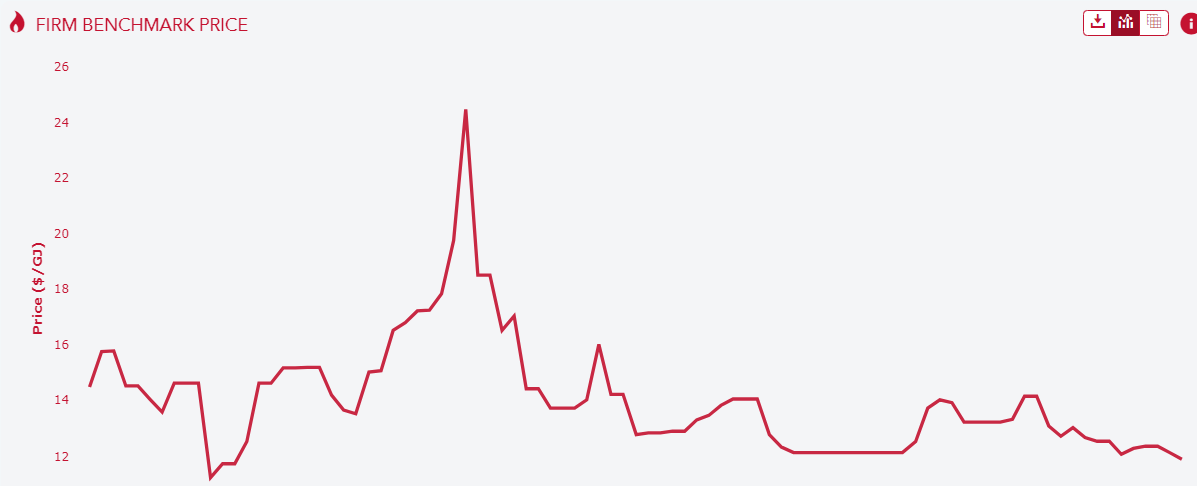

We can see that today, with the gas export cartel using Albo’s $12Gj price cap as a price floor:

Australian gas is a failed market. If it is not fixed, Australia itself will become a failed state.