Last week’s shock decision by the Reserve Bank of New Zealand to cut the official cash rate by 0.25% was an admission that the economy is deteriorating much faster than the central bank had expected.

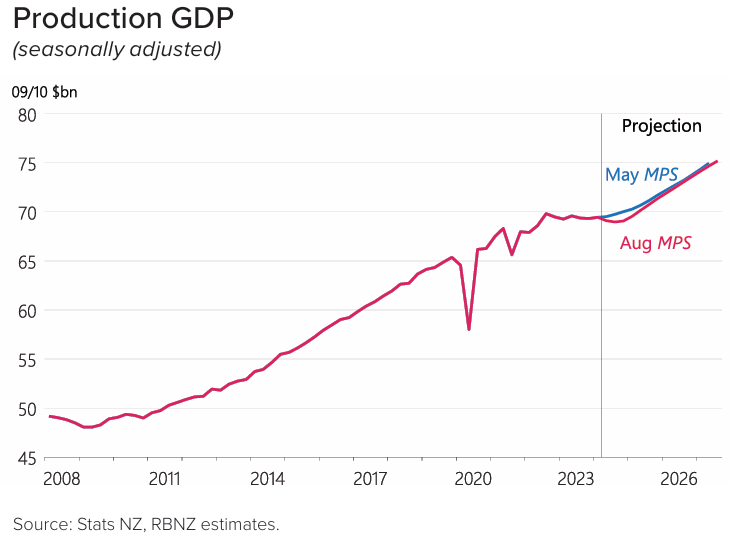

The Monetary Policy Statement (MPS) accompanying the decision noted that “the overall level of real GDP remains below its peak in the September 2022 quarter” and that “timely indicators of economic activity have weakened materially”.

As a result, “these indicators suggest that GDP contracted in the June 2024 quarter” and the Reserve Bank’s “projection for economic activity over 2024 is weaker than in the May Statement”:

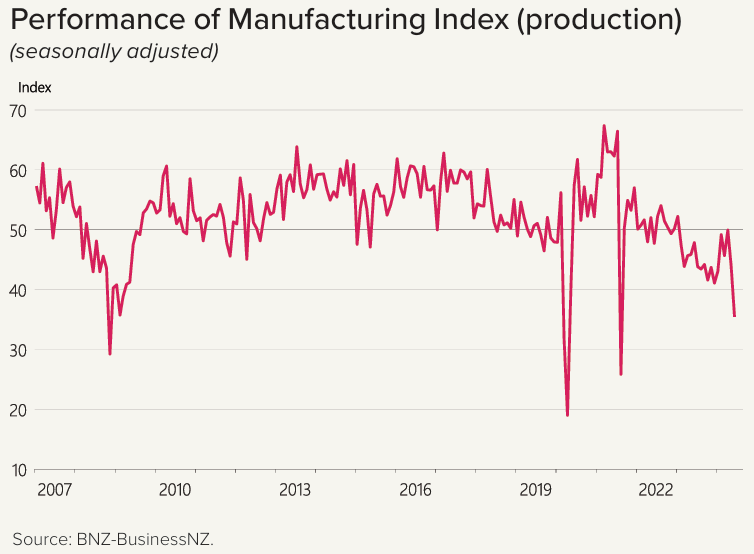

These “timely indicators” of weakness include the Performance of Manufacturing Index:

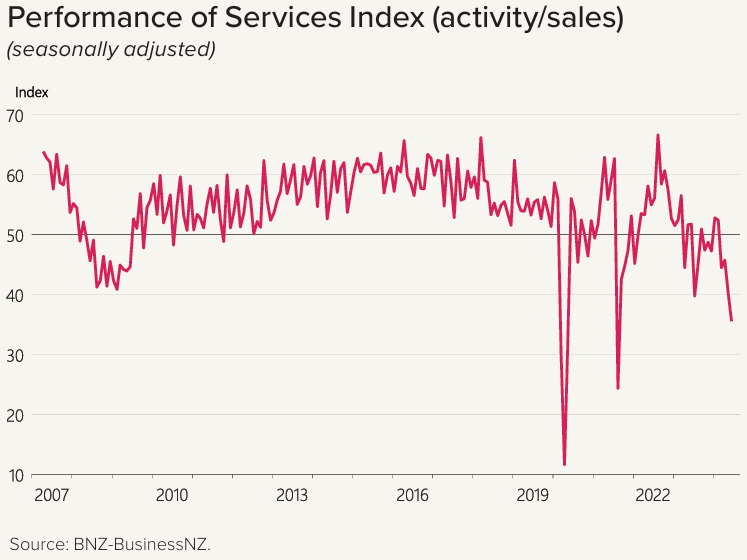

And the Performance of Services Index:

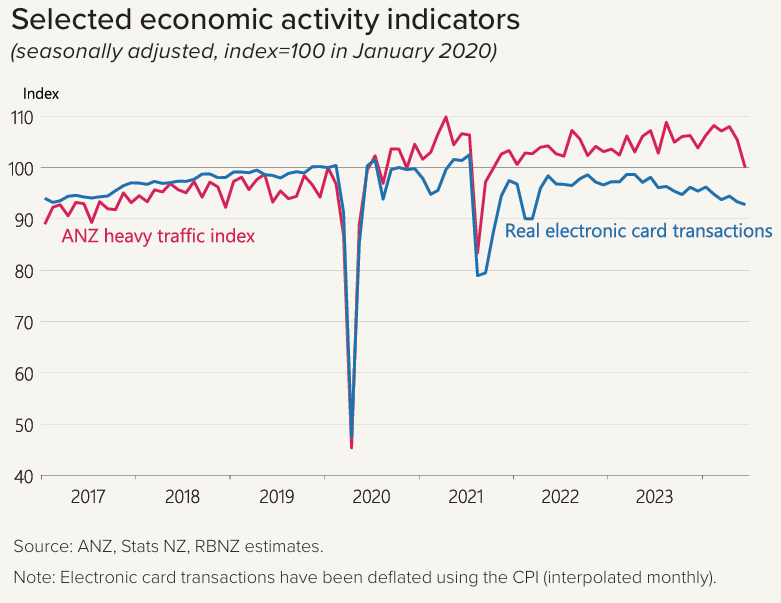

The Reserve Bank’s MPS also notes that consumer spending remains incredibly weak, as indicated by real electronic card transactions falling in May and June:

As such, the MPS noted that “our assumption for GDP growth over 2024 is materially weaker than at the time of the May Statement. We assume that GDP declined by 0.5% in the June 2024 quarter”.

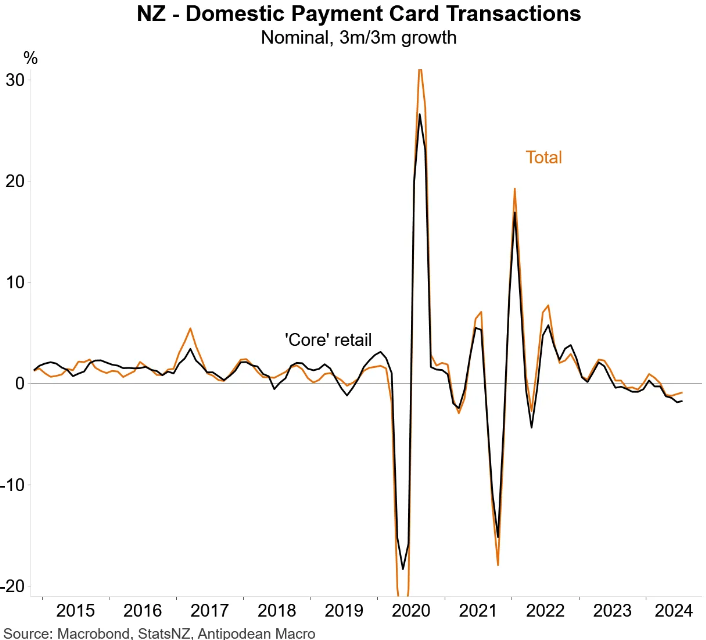

On Friday, Statistics New Zealand released card spending data for July, which showed that consumer spending weakened further.

The following chart from Justin Fabo at Antipodean Macro tells the tale, with retail spending in particular contracting:

The above spending data is in aggregate nominal terms. Therefore, it is not adjusted for inflation or population growth. If it were, it would show that consumer spending is stuck in a deep recession.

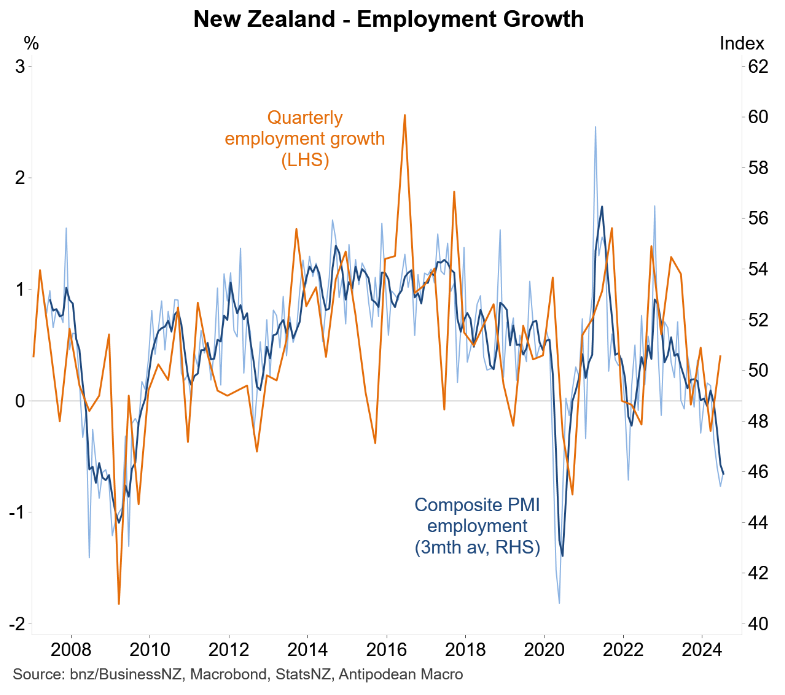

Leading indicators of New Zealand employment growth have also deteriorated:

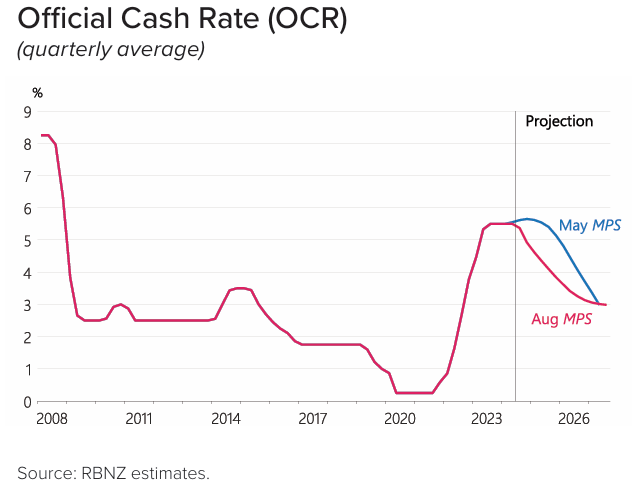

Given the ongoing weakness in New Zealand’s economy, the Reserve Bank will need to follow up with additional rate cuts in the coming monetary policy meetings.

The ‘good’ news is that the Reserve Bank’s official guidance is for the OCR to decline to around 3.0% by 2026, from 5.25% currently:

The OCR will need to fall to pull the economy out of recession.