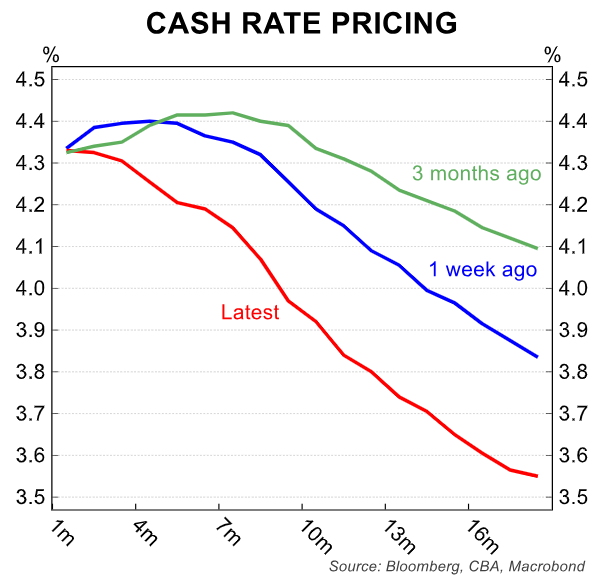

Last week’s Q2 CPI release from the Australian Bureau of Statistics (ABS) was obviously welcome news that will most likely see the Reserve Bank of Australia (RBA) keep interest rates on hold at Tuesday’s monetary policy meeting.

The all-important trimmed mean inflation came in below expectations at 0.8% over the quarter (versus 1.0% expected) to be 3.9% higher year-on-year.

It would have been greeted with a huge sigh of relief by the RBA, as it was in line with its May Statement of Monetary Policy (SOMP).

Annualised trimmed mean inflation was also 3.2%, just above the top end of the RBA’s inflation target of 3% to 3%.

Most economists and financial markets now tip that the RBA will commence a rate easing cycle towards the end of this year or early next year.

Indeed, following last week’s result, financial markets swung abruptly to tipping rate cuts after leaning towards rate hikes before the release.

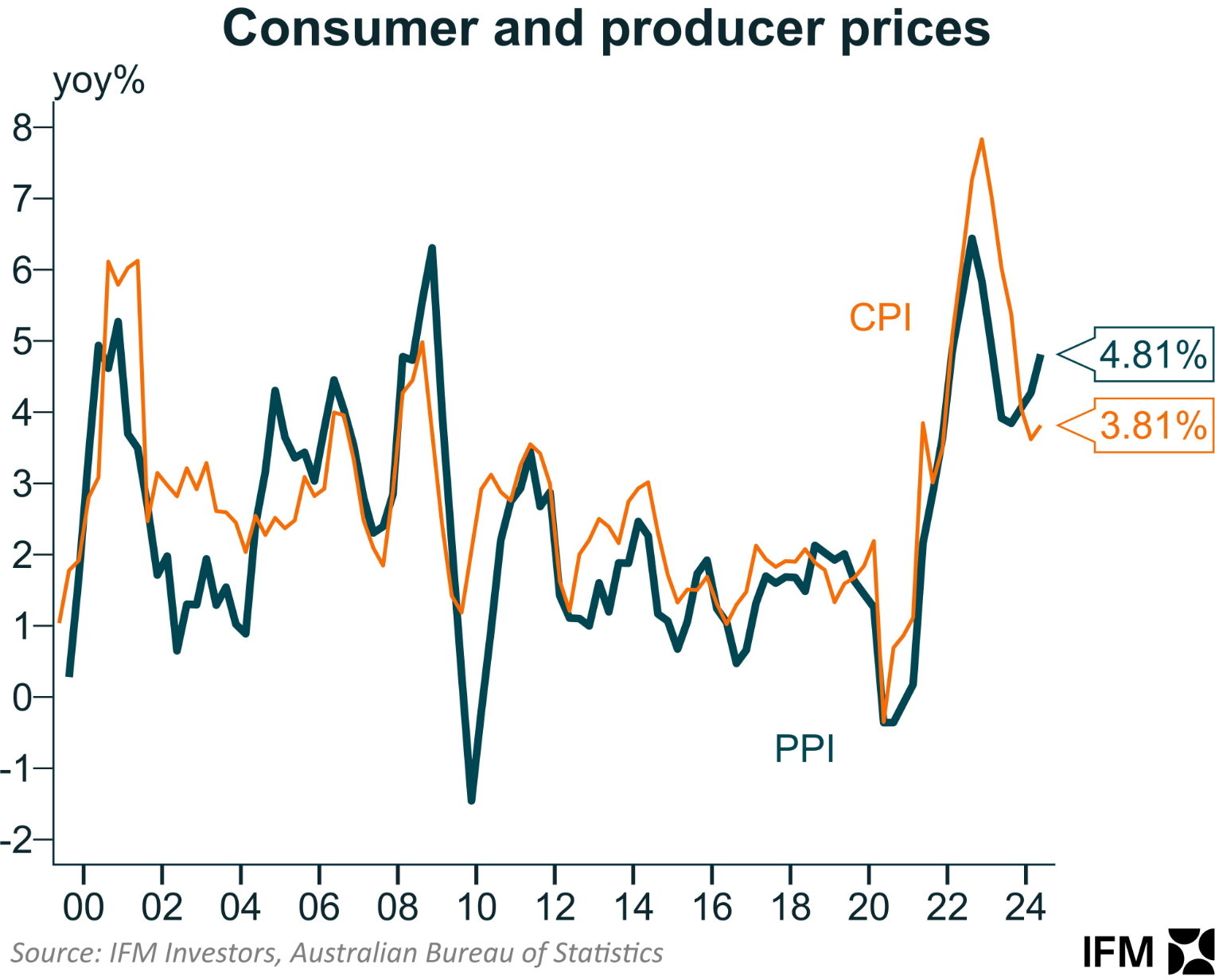

One area that warrants caution on the inflation front are producer prices, which firmed in Q2 according to Friday’s Producer Price Index (PPI) from the ABS.

The following chart from Alex joiner at IFM Investors shows that the annual change in the PPI rose to 4.81% in Q2 to be well above headline CPI inflation:

Joiner commented on Twitter (X) that we shouldn’t “be too aggressive pricing cuts just yet”, based on this data.

Separately, he noted that “will need the labour market to deteriorate and activity to weaken further… to see a cut”.

I agree. The RBA will need to see inflation fall further and unemployment rise more before it has the confidence to start cutting rates.

Nevertheless, I agree with the market’s current view that the next move in rates will be down. It’s just a matter of when.