The greatest energy criminal in Australia, Origin Energy, is back today:

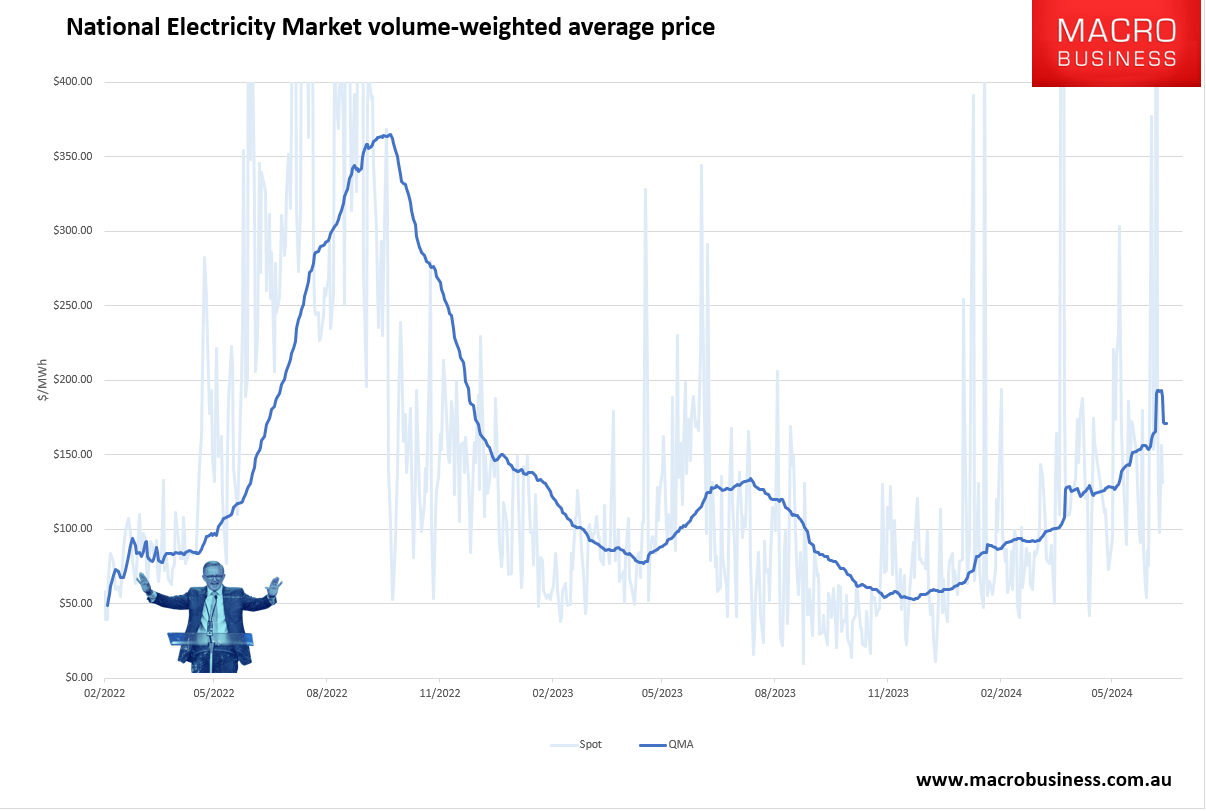

Origin Energy, the biggest Australian power and gas supplier, has soared to a bumper profit as higher electricity prices boosted its power plants and retailing business, but warnings of a softer year ahead triggered a sharp sell-off in the company’s shares.

The energy giant booked a bottom-line profit of $1.4 billion for the 12 months to June 30, up from $1.05 billion a year earlier. Underlying profit for the period surged nearly 60 per cent to $1.2 billion but still fell slightly short of analysts’ forecasts.

Higher earnings from Origin’s domestic power plants and retailing division were attributed to its ability to charge customers higher prices over the past year after energy regulators raised maximum price caps in mid-2023 to make up for a blowout in generation costs.

That is after Origin Energy engineered that spike in generation costs by exploiting gas prices following Russia’s invasion of Ukraine.

In turn, this was made possible by arguments against domestic reservation of gas popularised by a former Origin Energy executive working at the Grattan Institute, which is sponsored by, you guessed it, Origin Energy:

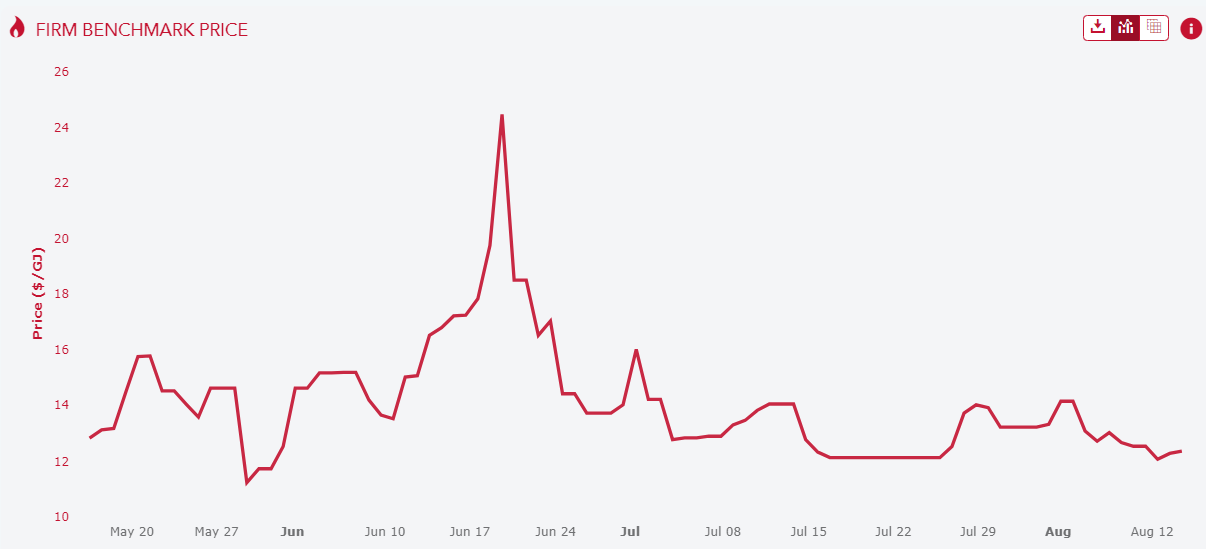

Today, Origin is still violating its social contract by keeping gas prices above the $12Gj price cap:

The simple truth of it is that Origin is a rogue firm that has done everything in its power to capture the political economy and turn it for its own ends.

- It has created an egregious vertical market structure that enables monopolistic pricing of both gas and electricity.

- It distorts public debate about energy markets and decarbonisation via sponsorship dollars.

- It violates the gas Code of Conduct on capped pricing.

- It rorts the NSW taxpayer for coal power subsidies.

- It pays next-to-no tax on its LNG exports.

- It operates more to the benefit of the Chinese economy than the Australian in partnership with Sinopec.

Origin Energy has torn up its social license to operate and should be nationalised, which would break the gas cartel, crash gas and electricity prices, accelerate the energy transition, end inflation, and restore industry.

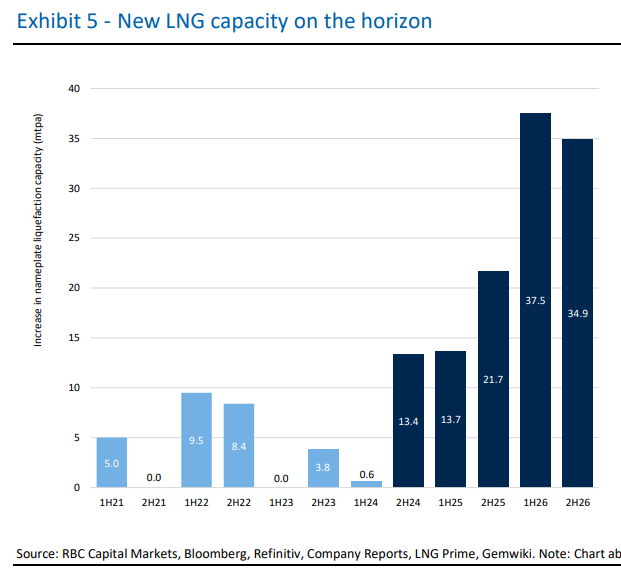

Meanwhile, we should all be cheering this on. RBC:

Following limited capacity additions and project start-ups in recent years, significant new LNG capacity is coming online over the coming years.

Altamira FLNG 1 (1.4mtpa) started up recently while debottlenecking at Freeport is set to add ~1.5mt of capacity soon.

The 13.3mtpa phase 1 of Plaquemines LNG is expected to be online in the coming months while Cheniere is set to bring the first of seven trains from Corpus Christi Stage 3 (10+ mtpa) online by year-end and another two by the end of next year.

Phase 1 of LNG Canada (14mtpa) will be starting up in mid-2025 while Golden Pass LNG’s (18mtpa) delayed startup is now planned for late 2025, with ramp-up likely through 2026.

Qatar expects to increase its liquefaction capacity by 33mtpa via the North Field East expansion by end of 2026.

In total, we calculate >120mtpa (165+ bcm) of capacity added (ex. Russia) across 2024-26 and adjusting for timing of startups and ramp-up, we see 24mt (33bcm) of incremental supply globally in 2025 and 73mt (100bcm) in 2026.

This is enough to crash the global price for a while, which will force local prices lower.