Ross Gittins argues that the Reserve Bank of Australia’s (RBA) “blunt” war on inflation has been borne primarily by households with mortgages, who have been sacrificed on behalf of the economy:

As research by Associate Professor Ben Phillips of the Australian National University has confirmed, the much-lamented cost-of-living crisis has been imposed on households with big mortgages far more than on any other households.

When you take account of the way rents actually fell during the lockdowns, renters haven’t been hard hit, while those who own their homes outright have been laughing. People on pensions or the dole have been protected by indexation.

So the reliance on interest rates to reduce demand is hugely unfair. But it’s also lacking in effectiveness. All of us have contributed to the excessive demand for goods and services, but only the minority of us with big mortgages have been pressed directly to pull back our spending.

This is why our management of the macroeconomy needs reform. We need another, much broader-based instrument that could be used as well as, or in place of, interest rates. Temporary changes in the rate of the goods and services tax are one possibility, but I’m attracted to the idea of temporary changes to the rate of compulsory superannuation contributions.

The two instruments – one interest rates, and the other budgetary – could be controlled by a new independent authority.

I have repeatedly made similar arguments, most recently last week in an interview with Tom Elliott at Radio 3AW:

The reality is that only around one-third of Australians carry owner-occupier mortgages.

As a result, the RBA’s monetary tightening has effectively smashed one-third of Australians in order to fight the inflation battle on behalf of all Australians.

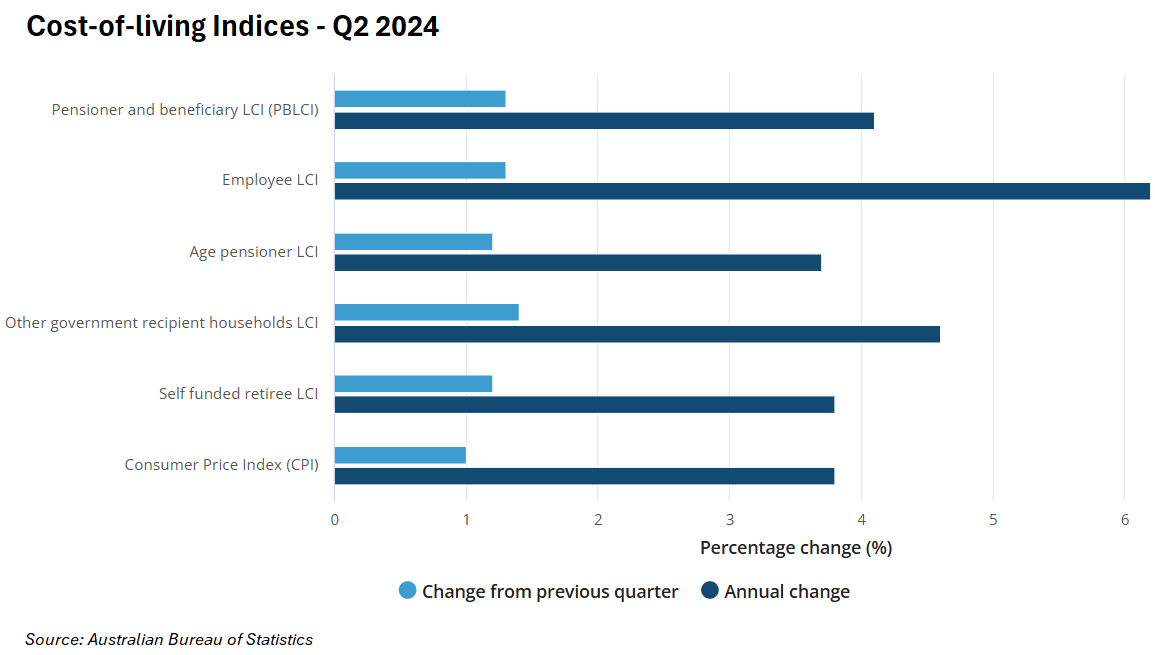

The impact of this blunt approach was illustrated by last week’s Cost-of-Living indices from the Australian Bureau of Statistics (ABS), which showed that employee households have been hardest hit.

Employee cost of living rose by 6.2% in the year to June 2024, well above the 3.8% increase in CPI inflation.

The primary reason why employee cost of living has risen so aggressively is because of higher mortgage interest rates, which comprise a larger share of their spending than for other household types.

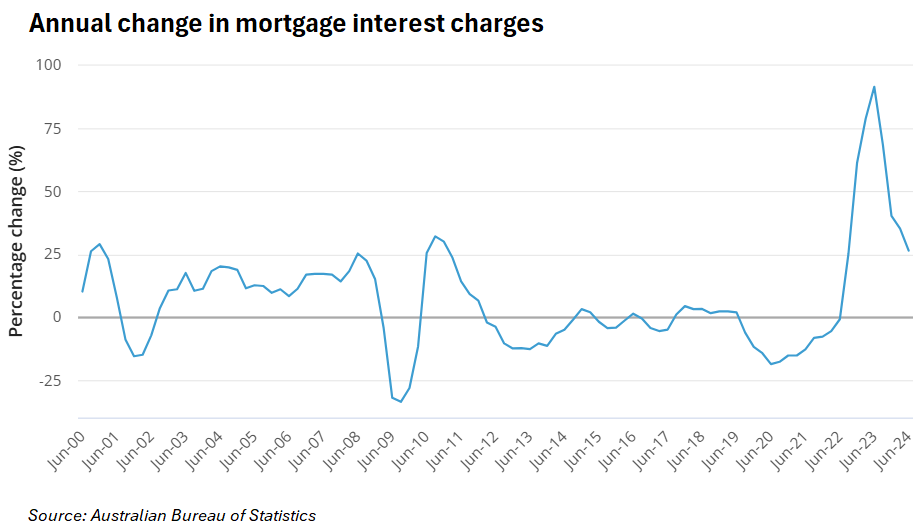

“Mortgage interest charges rose 2.6% in the June 2024 quarter, driven by the continued rollover of some expired fixed rate mortgages to higher variable rate mortgages”, noted Michelle Marquardt, ABS head of prices statistics.

“Mortgage interest charges rose 26.5% annually, continuing the moderation seen since the peak of 91.6% in the June 2023 quarter”.

Ross Gittins is right that we need broader tools to fight inflation. We also need our governments to assist the RBA in its inflation-fighting efforts via policy.

The federal and state governments should ensure that their spending is not expansionary when the RBA is trying to cool the economy via higher interest rates.

The federal government should also run a more moderate and sustainable immigration program that is compatible with the supply-side of the economy, namely business, infrastructure, and housing investment.

That said, I believe that adjusting the rate of the GST would be far more equitable and efficient than adjusting the rate of compulsory superannuation.

As I argued last week on Tom Elliott’s Radio 3AW segment (video above):

“Raising the superannuation guarantee would only impact those who are in the workforce”.

“But the people who are spending the most at the moment are actually the retirees who own their homes outright. They are spending at a very strong pace whereas everyone else is cutting back”.

“I think a better solution along those lines would be to raise the GST temporarily. That would bring down spending across the economy”.

Ross Gittins’ article is the right discussion to have.

We need to have more tools to fight inflation than interest rates. We also need our governments to work in tandem with the RBA, not against it.